Discover 9 shocking facts about unclaimed bank deposits in India and learn how the RBI UDGAM portal helps families search and recover forgotten bank money. unclaimed bank deposits in India, RBI UDGAM portal, dormant bank account India, RBI unclaimed deposits rules, how to claim unclaimed bank money India, DEA fund RBI, forgotten bank accounts India.

Introduction

Some Indians hold several bank accounts across life – pay check ones, savings, fixed deposits, shared accounts set up for different money reasons. As years pass, a number sit unused or get overlooked when jobs shift, people move, retire, or just lose track. When such accounts remain untouched for years, the balances can eventually turn into unclaimed bank deposits in India.

Few grasp how big this really is. Data from the Reserve Bank of India shows countless crores sitting idle in bank accounts across the country. Money left behind by regular people – some lost track, others never knew it was there. Because the scale matters, authorities stepped in. A single online system now exists to help find what’s been overlooked: the UDGAM Portal.

Sometimes a person might lose track of old bank deposits. This website helps them look through several banks at once to find what could be missing. When relatives face tough situations like inheriting money, unclear records, or inactive accounts, it becomes useful. Money long gone unnoticed sometimes shows up because of this tool.

Finding out why money gets left behind at banks matters to anyone who holds an account. Rules exist to manage these forgotten funds, though few pay attention until it affects them. One way or another, each person might face a moment when tracing lost cash becomes necessary. Knowing what steps follow helps clear confusion later on. Procedures differ slightly across regions but share common ground overall. People regain access by following specific paths set by financial authorities. This article explains nine important facts about unclaimed deposits in India, along with practical guidance on how to prevent your money from becoming unclaimed.

What Are Unclaimed Bank Deposits in India?

Money left untouched in bank accounts might sit idle for years when owners stop using them. Such funds show up across different types of holdings – savings, current, fixed, or recurring deposits. Often, no activity happens because the person does not log in, withdraw, or even check balances. Over time, these dormant sums become what banks call unclaimed property.

After someone stops using their bank account for a long while, it gets marked dormant. Should that go on for several years without any word from the person, the money inside becomes what is called unclaimed. These amounts never vanish nor are seized by authorities or the bank itself. They move into a protected pool overseen as per rules set by the central bank.

This system keeps funds accessible so owners or their heirs can retrieve them later. Still, tracking down these balances gets tricky when paperwork is missing. Often, relatives aren’t even aware an account exists.

How Bank Deposits Become Unclaimed

A sleepy kind of silence settles when money sits untouched for too long. No movement, just stillness where activity once was. Then comes a label – dormant – applied quietly by the institution holding it. Years pass without contact or notice from the owner. Eventually, that sum shifts into a separate reserve overseen by the central bank.

Folks often land here after things unfold a certain way. A chain of everyday events tends to push them toward this result.

Common causes include:

- Forgotten salary accounts after job changes

- Fixed deposits that matured years ago

- Migration to another city or country

- Death of the account holder without nominee details

- Customers maintaining multiple bank relationships

These situations are surprisingly common in India, particularly among individuals who opened several accounts during their working years.

Real Life Example: Forgotten Salary Account

That year in Mumbai, Rohit started at a private firm during 2012. On joining, his boss set up a paycheck account through one specific bank. Three years later, job change came along, so he left for work somewhere else in another city entirely. A fresh pay account followed under the new workplace arrangement. Meanwhile, the old banking details slipped his mind without notice.

A single account sat untouched for ten years, holding just a bit of money while gains built up through a tied fixed deposit. Updates never reached Rohit – his phone number on file was out of date. Much later, during paperwork checks for buying a house, he came across the forgotten record. It turned out the bank labeled it dormant long ago.

Folks run into these scenarios all the time, which piles up a big chunk of forgotten money sitting idle in Indian banks.

RBI Regulations Governing Unclaimed Deposits

Starting year two, every bank must spot customer accounts showing no activity. When found, they send letters or messages trying to reach the owner before things sit too long. Records stay updated by law, holding numbers safe if nobody claims them. Silence from account holders triggers steps meant to protect what is left behind.

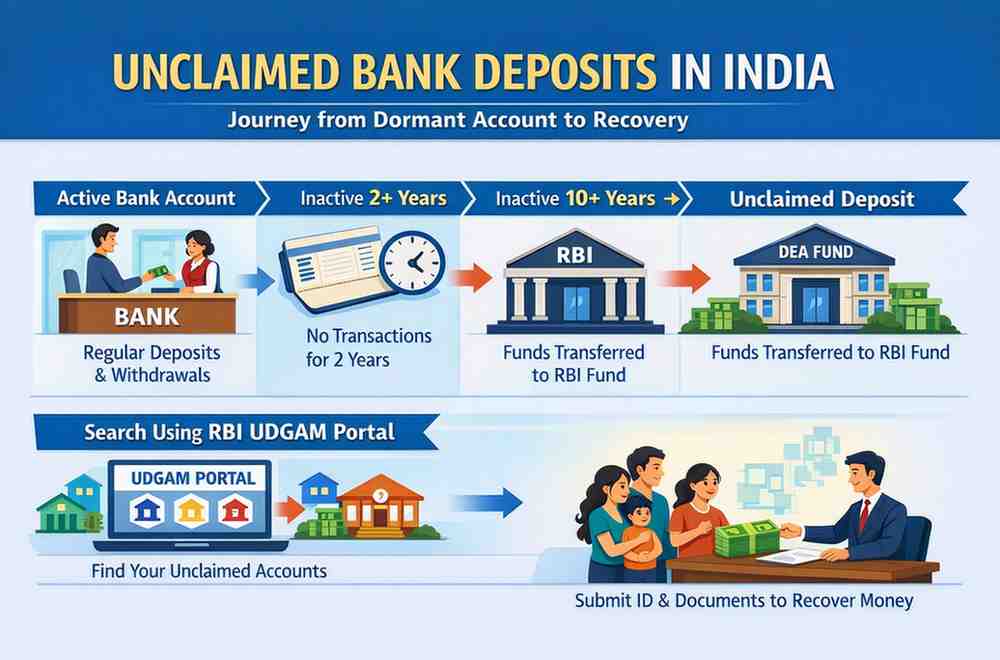

A gap of two years with no activity usually turns a bank account into what’s called dormant. When that silence stretches to a full decade, the money inside must move – it flows into the DEA Fund, held by the RBI. Silence, once long enough, triggers transfer.

Just because cash moves into the DEA Fund doesn’t strip the owner’s rights. Should someone pass away, family members may still walk into a branch, years later, and take back what was left behind.

9 Shocking Facts About Unclaimed Bank Deposits in India

1. Thousands of Crores Remain Unclaimed

It might catch you off guard, but stacks of cash sit untouched in Indian banks. According to RBI records, those dormant accounts add up – way past several lakh crore rupees. What rests there? Money waiting, forgotten by owners.

Money sitting in these accounts came from regular people who put it away long ago, then forgot where it was. Years pass before some households find out about the cash – often when going through paperwork following a loved one’s passing.

2. Dormant Accounts Are the Main Source

Sleeping too long makes bank accounts start fading away. After folks walk away, activity gets frozen – safety comes first. These forgotten spots? They slowly shift into a quiet zone called dormant.

It hits most people when they finally go to pull funds out, having left things untouched for years – then learning the account needs waking up first. Situations involving inheritance disputes can also reveal forgotten accounts, especially when families try to understand the difference between nominee vs legal heir in India while settling financial assets.

3. Money Is Not Confiscated

Most people believe banks keep forgotten money forever. Actually, that idea does not match what really happens. Government holds those funds – they are never lost.

Ownership stays with the depositor, even once cash moves into the RBI’s fund meant for awareness. Should someone come forward with proper proof, it falls to the bank to handle their request. Only then does release happen, under clear verification steps.

4. Families Often Discover Accounts After Death

When someone passes away, forgotten bank accounts often surface unexpectedly. Relatives might have no idea about every money link the person once held.

Without shared records or named beneficiaries, tracking down old accounts can turn into a real puzzle. Picture this: a simple chat today might save months of confusion later on. Clear notes plus open talks help keep things sorted when life gets complicated.

Real Life Example: Family Finds Hidden Fixed Deposit

That year, when Mr. Sharma died, his relatives started going through his money files. Not long after, they uncovered multiple accounts along with some insurance plans, thinking nothing else was left. Then again, during sorting, his daughter stumbled upon a dated slip – a fixed deposit – from a far-off branch. Only then did doubt creep in.

A few years back, the deposit reached its maturity date yet stayed unused. Once the family got in touch with the bank, it turned out the money had moved to the RBI account because nobody claimed it. With checks done and papers proving rightful inheritance handed over, the payout finally went back to them.

A single oversight might leave money untouched for decades. How quietly wealth slips through the cracks surprises most people.

5. The UDGAM Portal Makes Searching Easier

Now there’s a way to find forgotten bank money. Starting today, people can look up old deposits without visiting each bank separately. One stop brings together records from many banks at once. With just a name, someone might discover what was lost long ago. Finding what belongs to you becomes simpler this way. Details like account numbers aren’t needed right away. Information flows more smoothly now than before. A single place does what took many steps earlier.

One place holds all the records, making it easier to see what’s been lost. Searching here means no need to reach out to each bank on your own. A single check replaces many separate requests. This way, finding old accounts becomes simpler than before.

6. Multiple Banks Participate in the Database

Finding lost money just got easier because banks – both government-run and privately owned – are now sharing information with UDGAM. Instead of visiting each bank separately, people can look up forgotten funds in many places at once through a single access point.

A match shows up in the search results? Go to the bank’s local office instead of waiting. Bring every document needed to finish claiming it – no shortcuts allowed.

7. Claiming Deposits Requires Documentation

Start by showing who you are – banks need that first. Then comes the part where you prove it actually belongs to you. Papers like a passport or ID card usually do the job for identity. Proof of where you live might mean a utility bill or rental agreement. Old bank books sometimes help, especially if they show activity. Deposit slips work too when signed and stamped. Each piece adds up to make the case stronger. Not every branch asks for the same things though. Some want more, others less. It depends on how old the account is. Rules change based on location as well. Nothing moves forward without clear links between person and funds.

When someone who held an account dies, those entitled by law might have to provide papers like proof of passing, a court-backed inheritance slip, or evidence naming them as beneficiary – banks wait for these before handing out money.

8. Dormant Accounts Can Attract Fraud Risks

Inactive accounts sometimes become targets for misuse or suspicious activity. In rare cases, criminals attempt to exploit dormant banking relationships for illegal transactions.

Financial authorities therefore monitor such accounts carefully, particularly in cases linked to money mule accounts in India where dormant accounts may be used for fraudulent transfers.

9. Forgotten Accounts Often Surface During Disputes

A few people stumble on forgotten accounts when checking bank issues. Take someone going through payment history after a problem – they might notice an outdated profile is still active.

Consumers should also understand how credit card chargeback disputes work when investigating suspicious transactions or billing errors in financial accounts.

How to Prevent Bank Deposits From Becoming Unclaimed

Besides keeping track of money, staying in touch helps stop accounts from going dormant. What often matters most? Regular attention – paired with updates when life changes happen.

Simple preventive measures include:

- reviewing bank accounts regularly

- updating contact details with banks

- registering nominees for accounts

- maintaining a consolidated list of financial assets

- informing family members about bank relationships

Funds stay claimed longer when these steps are followed. Over time, fewer go missing.

Conclusion

Money left behind in Indian banks is a real problem that could easily be avoided. When people forget about their accounts, fail to keep proper records, or skip naming someone to inherit funds, loved ones may never find what was saved. Starting today, finding lost money just got simpler thanks to a new tool from India’s central bank. Hidden away? That cash might still be waiting – this system helps track it down. When accounts sit untouched, they fade from view; knowing the rules keeps your funds within reach. Family needs may arise later, so holding on to paperwork makes all the difference. Access stays possible only if you stay aware and keep records close.

FAQs

Q1: What are unclaimed bank deposits in India?

Unclaimed bank deposits are funds lying in bank accounts or deposits that remain inactive and untouched for many years. When there are no transactions for a long period, banks classify such balances as unclaimed deposits. Even after funds are transferred to the RBI’s Depositor Education and Awareness Fund, the depositor or legal heirs retain the right to claim the money.

Q2: When does a bank account become dormant?

After two years without any customer-initiated transactions, a bank account often goes dormant. In these situations, banks may limit services like internet banking and ATM withdrawals. By completing KYC verification and starting a transaction through the bank branch, customers can reactivate inactive accounts.

Q3: Can unclaimed deposits still be recovered?

Yes, even after being moved to the RBI’s special fund, unclaimed deposits are still recoverable. Clients or legal heirs must go to the relevant bank and provide proof of identity and ownership. Banks process the claim and give the money to the legitimate owner after verification.

Q4: What is the RBI UDGAM portal?

A centralized online platform called the UDGAM portal was created to assist customers in looking for unclaimed deposits at various Indian banks. To find out if any bank account or deposit is still unclaimed, users can enter the depositor’s basic information.

Q5: Why is nominee registration important?

Bank deposits can be easily transferred to a chosen person in the event of the account holder’s death thanks to nominee registration. When attempting to claim monies from the bank, legal heirs may encounter delays or legal procedures in the absence of nominee data.

Disclaimer

This article is intended for informational and financial awareness purposes only. Banking rules, RBI regulations, and claim procedures may change over time. Readers should verify the latest guidelines from their respective banks or official RBI sources before making financial decisions.