Unlock the power of the 8-4-3 Compounding Rule to accelerate wealth creation. Learn strategies, real examples, and mistakes to avoid for faster financial growth. 8-4-3 Compounding Rule, compounding strategy, wealth creation rule, power of compounding, long term investing strategy, financial growth formula, passive income growth, investment strategy India, compound interest strategy, wealth building tips.

Update Note (April 2026): The 8-4-3 Compounding Rule follows a 15-year timeline where the first 8 years focus on disciplined investing, the next 4 years on increasing contributions, and the final 3 years on exponential growth through compounding. It emphasizes consistency over quick returns and aligns investing with income growth. This approach shows how structured patience can significantly accelerate long-term financial outcomes.

Introduction

Money isn’t the finish line most think it is. Those who earn big pay checks often stay stuck, surprised by empty accounts. Wealth skips many of them entirely. What shifts things? A quiet habit done differently. Growth builds when returns feed future gains, slowly at first – then like rolling snow. That pattern separates those with lasting funds from everyone else watching numbers rise but never stick.

The 8-4-3 Compounding Rule is not just another theoretical concept. Most people grow money slowly, shaped by habits they form early. This method fits how lives actually unfold – earning more later, saving steadily. Step follows step, each part linking naturally to what comes next. Progress feels clear, since actions match daily reality. Momentum builds quietly, without sudden jumps or guesswork.

Most people get how compounding works when they hear about it. Yet once real money’s on the line, things fall apart fast. That stumble between knowing and doing – this breaks more plans than bad advice ever could. When you combine this rule with foundational concepts like the power of compounding, the difference in long-term results can be massive.

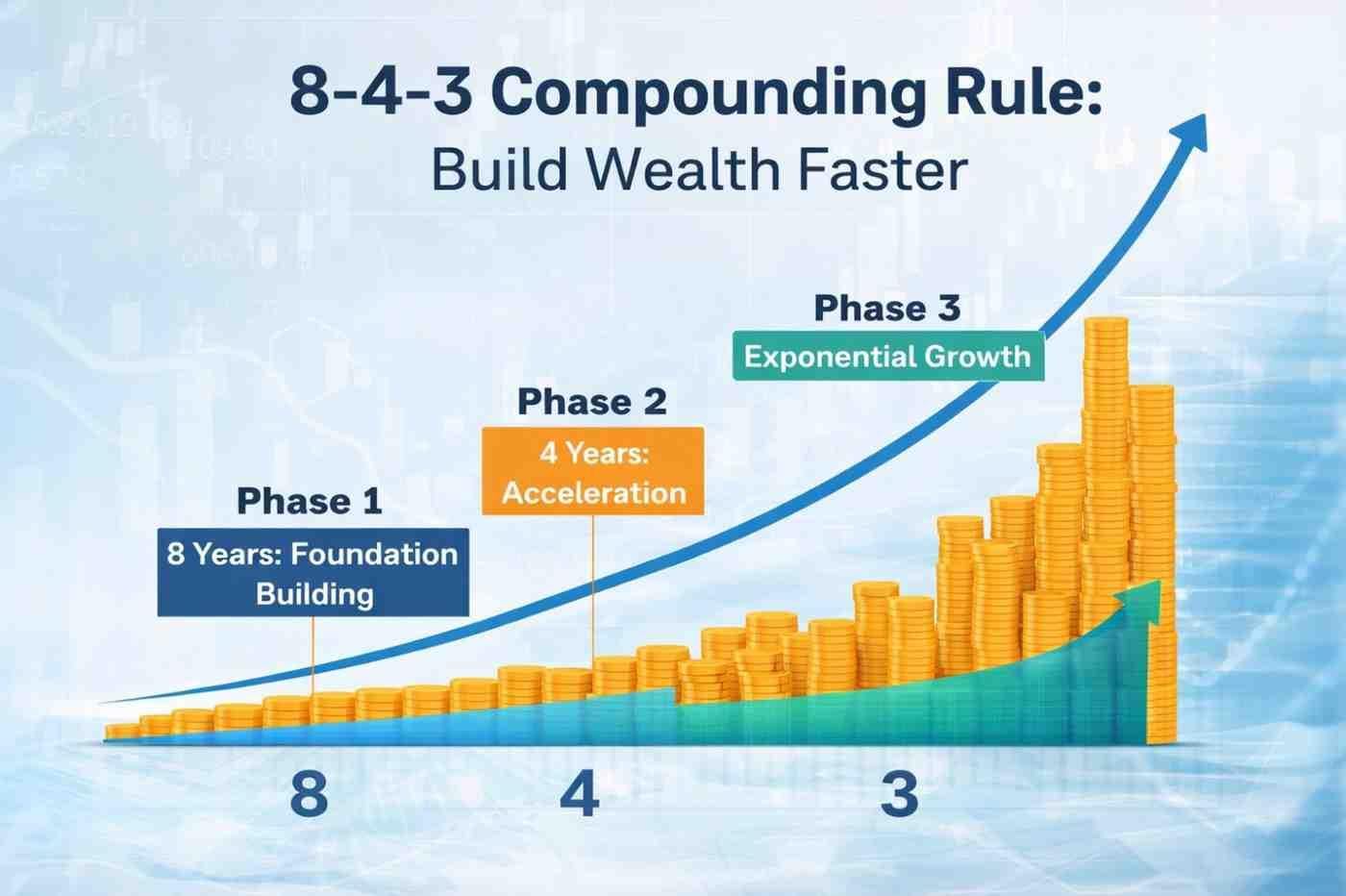

What is the 8-4-3 Compounding Rule?

The 8-4-3 Compounding Rule divides your wealth-building journey into three structured phases that align with how money actually grows over time. Eight years make up the opening stretch, where steady investing matters more than hunting big gains. Through these times, setting down solid money roots becomes key – showing up regularly with investments, no matter what markets do. That stretch shapes how you act, turning persistence into routine.

Four years ahead move fast. Income tends to climb during this stretch. A stronger financial spot opens room to put more into investments. What happens now builds directly on earlier groundwork – it gains momentum here. Contributions rise sharply rather than staying flat. Growth speeds up simply by adding more. The effect stacks quietly but deepens over time.

Three years out, gains from past choices multiply faster than before. Then come moments when earlier moves fuel new spikes in value automatically. Suddenly, results surge ahead even if actions stay steady. Growth leaps higher while inputs remain flat. Most methods bank on fuzzy timeframes. Not this one. It builds around how pay actually comes in – steady, predictable, tied to actual weeks people work. When combined with disciplined financial planning like investment plan by age, it becomes even more practical and effective.

Why This Rule Works Better Than Traditional Investing

Most folks begin earning less, then see income rise slowly as years pass. Sticking with investments over decades matters – that part advisors get right. Yet routines alone do not match real-life money habits. Life brings shifting demands: early struggles differ from mid-career costs or later stability. A fixed strategy ignores such changes. Enter the 8-4-3 idea – built for how wallets grow, not just time ticking by.

Most people find this method fits their life better since it grows along with their paycheck and peace of mind. Early on, staying regular matters more than results, easing stress so they stick with it. When earnings go up, investing follows naturally, using extra room in the budget without strain.

Most people skip planning, yet picking dates shapes how money moves. Hitting targets step by step trims the noise cluttering choices. Without checkpoints, decisions wobble – spreading too thin or grabbing quick wins often backfires. Structure keeps effort focused where it counts. When paired with practical habits like smart personal finance habits, the results become more predictable and sustainable over time.

11 Eye-Opening Insights of the 8-4-3 Compounding Rule

Insight 1: The First 8 Years Decide Everything

Most people overlook the beginning, though it matters more than anything else when growing wealth step by step. Not aiming for big gains at first lets you focus instead on steady habits that stick. Little amounts put in regularly become powerful only when kept going without break. Starting slow teaches how to stay calm when prices jump or drop suddenly. Jumping out too soon ruins progress, especially when someone wants fast wins. Patience gets stretched most during the opening eight years, yet sticking around often pays off down the line. What happens then shapes how you see losses, choices, and long-term moves with money. When aligned with structured approaches like investment plan by age, it becomes even more effective.

Insight 2: Consistency Beats Intelligence

Success with compounding does not demand a finance degree. Staying on track matters more than knowing every detail. Smart investors sometimes lose out by tweaking too much, shifting plans too often. Following through without pause lets you ride the waves of upswings while skipping nothing big. Modest gains add up when repeated year after year. Most wins come not from knowing charts, but from staying calm when things shake. Those who follow their strategy usually do better than people jumping at every headline. This is why understanding behavioural mistakes, such as those highlighted in silent financial mistakes to fix now, is crucial.

Insight 3: The 4-Year Acceleration Phase is Critical

Staying put often beats jumping in and out. Many think spotting the perfect moment to buy boosts gains, yet that idea rarely works out. Growth builds slowly when money keeps earning on itself year after year. Jumping around between trades breaks that flow, chipping away at progress. What matters most is showing up consistently, not guessing what comes next week. When markets fall, holding steady helps your money bounce back. Through ups and downs, those who wait tend to gain more over time. Jumping in and out usually means leaving growth behind. This principle is reinforced by strategies like benefits of staying invested during market dips.

Insight 4: Compounding Needs Time, Not Timing

Staying invested often beats jumping in and out. Many think spotting the perfect moment to buy will bring bigger gains. Truth is, growth stacks up when money sits undisturbed for years. Jumping around breaks that build up – costs add up without notice. What really counts isn’t guessing peaks and dips – it’s how long you remain. When markets drop, holding steady means your investments can bounce back later. Over years, those who wait usually gain more because they ride through ups and downs, while quick movers skip the slow build up of returns. This principle is reinforced by strategies like benefits of staying invested during market dips.

Insight 5: The Final 3 Years Create Exponential Growth

The last phase of the 8-4-3 Compounding Rule is where the real transformation happens, and this is the stage most people underestimate. Three years before the finish line, growth shifts – no longer steady, but rapid. That speed comes from past gains now fuelling future results. Not just fresh deposits each month, but old savings doing most of the lifting. The bulk of progress rides on what was already earned. Now imagine your money has been running a long race. Each step forward grows bigger without needing extra effort. Most people walk away right when progress speeds up. They leave because waiting feels pointless, though results are about to surge. It’s like stepping off the track one minute before crossing the end point.

Patience matters most when you let things unfold naturally. Not pushing harder can work better than trying too much, especially if distractions are kept away. Sticking around without reacting builds strength over time, slowly shifting odds in your favor. People who skip the urge to fix what isn’t broken tend to gain more than they expect, like quiet growth sneaking up on them.

Insight 6: Small Delays Create Huge Losses

Starting late might be the riskiest move you make with money. People often wait, thinking better pay or stability should come first. Yet every month lost chips away at growth, since time shapes how powerfully savings build. Missing early years means missing what those years could have grown into. Later start dates chip away at what you could have built, simply because beginning sooner lets money stretch further. Each year missed means one less round where gains build on top of gains. Those first few moments matter most – their absence weakens everything after. Skipping even a short span steals chances that never return.

Late beginnings usually demand bigger payments later – something that can feel heavy on the wallet. Heavy loads like these tend to limit choices instead of expanding them. A slow start with little money beats rushing in with a pile much later. Easing into saving early makes growing money feel lighter down the road.

Insight 7: Avoid Over-Diversification

Most people think spreading money around keeps things safe. Yet having too many different spots might actually pull down what you earn. Spreading thin means each piece plays a smaller role. Big wins get lost when everything gets split so far apart. Most people think owning extra choices cuts down danger. Yet spreading efforts too thin brings confusion instead of control. When attention splits across countless picks, clear thinking often fades away.

Starting small beats spreading too thin every time. Owning less can mean winning more when choices are sharp. Growth thrives where focus does – scattered picks lose steam fast. Picking smart builds steady ground for gains to grow on their own. Balance isn’t luck – it shows up when structure stays clear. What matters sits between timing and choice, never just quantity.

Insight 8: Income Growth Fuels Compounding

Wealth builds faster when rising earnings fuel it. Though regular investing matters, putting in more money as time passes makes a big difference. When pay goes up, so should what you set aside. Most folks stick to the same investment size despite making more money. Yet spending shifts upward too, soaking up extra cash that could grow. So gains miss out on multiplying fully over time. Wealth piles up slower than it might otherwise.

Every time pay goes up, putting more into investments kicks off a strong chain reaction. Bigger deposits mean gains grow faster, feeding the snowball of compound interest. Money builds on itself when rising income meets steady saving. Growing earnings matters just as much as growing portfolios over years. Wealth rises best when effort flows both ways.

Insight 9: Risk Management is Non-Negotiable

Stability shapes how well compounding grows, so handling risk matters when thinking ahead over years. Big gains might come from bolder moves, yet sudden drops can break the steady climb needed for growth to build. One big setback might wipe out progress built over many years, leaving you back at square one. That’s the reason staying cautious matters just as much as aiming high. Growth that lasts beats quick wins every time, which smart investors know well.

Starting off knowing how much risk feels right shapes where you put your money. Because balance across different assets matters, mixing types can soften potential losses. When you check in on holdings now and then, adjustments keep things on track. Keeping funds safe means growth isn’t derailed by sudden drops. Over months or years, steady progress builds without needing big swings.

Insight 10: Automation Builds Discipline

Sticking with a plan for years can be tough when putting money to work. Feelings pop up, headlines shout, prices jump around – suddenly habits shift. When moves are set ahead of time, choices fade into the background, letting deposits flow like clockwork.

Starting with scheduled deposits, investing happens without guessing when markets rise or fall. Even when prices drop, money moves steadily into funds because the system runs on its own. Skipping buys during rough patches? That slip gets cut since transfers happen whether news feels good or bad.

Little by little, steady habits build up what matters most. Hitting each week means riding through highs and lows, smoothing out the bumps in results. When things run on their own, decisions fade into background noise – actions stick without effort. Sticking around long enough changes outcomes, even when nothing feels different day to day.

Insight 11: Mindset Determines Success

Most of what happens along your path to growing wealth hinges on how you think. Excitement at the beginning doesn’t guarantee staying power when returns stay flat. It takes months before slow gains turn into something noticeable. Waiting quietly while numbers inch forward isn’t thrilling for people chasing fast wins. Anyone focused only on rapid rewards usually walks away too soon. The deepest gains arrive later – after others have already left.

Most people lose track when prices jump around. Staying calm comes easier if you see past next week’s numbers. When things get shaky, steady habits keep moving. Big wins often follow rough patches nobody enjoys at the time. Start strong by building habits that stick. Stay calm when markets shake instead of reacting fast. Rely on your plan every time doubt creeps in. See results grow slowly once thoughts match future aims. Money builds without force if patience stays present. Let consistency do the heavy lifting, not effort.

Real-Life Examples of the 8-4-3 Rule

Picture someone setting aside eight thousand rupees every month starting at twenty five. For nearly a decade, the habit matters more than market moves – just steady deposits into their account. At thirty three, they shift gears, pushing up contributions to twenty thousand each month. Over four years, that extra flow swells what’s already there. The last stretch brings quiet power: money earned now builds upon earlier gains. Growth begins feeding itself without new effort. Three years later, results emerge not from activity but momentum.

Picture two people beginning at separate times. Early on, one puts aside modest sums without delay. The other waits years, then adds bigger chunks all at once. Even though that second person moves greater totals, their balance trails behind – time slipped away. Growth needs space to breathe, after all. What matters most shows itself slowly: begin sooner, keep going.

Common Mistakes That Destroy Compounding

When markets dip, some people halt investing without realizing it freezes their losses. Instead of riding out drops, they miss gains when things bounce back. Shifting tactics after small wins or dips messes up steady growth too. Sticking with a plan quietly builds more than jumping around ever does. Most people chasing big gains end up in shaky deals – losses pile up fast that way. When waiting feels too long, decisions get rushed; money pulls out before time has passed. Discipline slips when pay rises but deposits stay flat, growth stalls without notice. Compounding works best if poor habits are simply left behind.

External Validation of Compounding

Most studies on money growth point to compounding as a steady force, backed by real-world results across markets. Staying invested year after year tends to pay off more than trying to time moves in and out. Over decades, accounts left untouched often grow far beyond what active traders gain through constant shifts. What matters most isn’t speed – it’s how long gains keep multiplying.

You can verify these principles through detailed resources like Investopedia’s guide on compound interest. These sources reinforce the idea that time, consistency, and discipline are the key drivers of compounding success.

Who Should Use the 8-4-3 Compounding Rule?

Most people aiming to grow money over time might find the 8-4-3 Compounding Rule fits their goals. Steady paychecks make it a strong match – those earning regular wages often see good results. New investors gain clarity since the method lays out steps without clutter. Clarity comes first here, helping avoid guesswork when starting out. Sticking to this rule works well for people wanting control over their money, since it fits how they plan ahead plus encourages steady choices. Those ready to keep going without reacting to quick market noise often get solid results. Over time, even pros tweak their approach using this method – consistency tends to grow when habits line up.

Conclusion

The 8-4-3 Compounding Rule is not about complex strategies or quick wins. Most people overlook the quiet role of routine, yet showing up matters more than any single decision. Following a steady path means money moves in step with life, not against it. Sticking with it – day after day – that is where things fall apart for many. Patience becomes rare, so those who keep going stand out without trying. Tiny actions, repeated, swell quietly, shaping what lasts far beyond quick wins.

FAQs

Q1: In a nutshell, what is the 8-4-3 Compounding Rule?

Eight years kick off the plan – steady deposits build the base. Then four stretch further, pushing more cash in each month. Finally three ride rising momentum alone. Fifteen years unfold this way. Growth leans on patience, not luck. Time feeds results, step by step.

Q2: Is the 8-4-3 Compounding Rule suitable for beginners?

True, newcomers find this method works well since it brings order to how they invest. Sticking with a plan keeps them on track instead of jumping at quick profits or switching tactics too often.

Q3: In order to adhere to the 8-4-3 Compounding Rule, how much should I invest?

Whatever you earn, there’s no set number that fits everyone. Begin by putting aside something small – something manageable right now. Over months, shift higher little by little without pressure. Progress grows when steps stay steady but quiet.

Q4: If I quit investing during the 8-4-3 cycle, what would happen?

Stopping investments can drastically lower long-term profits and interfere with the compounding process. Maintaining consistency is essential, and even little pauses might affect the ultimate financial result.

Q5: Is it possible to apply the 8-4-3 Compounding Rule to SIPs or mutual funds?

True, mutual funds and SIPs follow this rule closely since consistent investment feeds steady expansion. Their structure fits naturally with patient wealth building through time.

Q6: Why does compounding take so long to produce results?

At first, gains move at a crawl since the starting amount is tiny. Over time, each return builds on top of larger totals. Growth stays quiet then suddenly surges forward. What seemed small becomes powerful without warning. Patience hides the shift until it arrives

Disclaimer

This piece aims to inform, nothing more – never meant as guidance on money matters. Decisions about where to put funds depend on personal targets, how much uncertainty one accepts. Conditions out there shift; what happened before offers no promise of repeats. Talking with someone who knows finance helps when choices loom. Cases shown here simply show possibilities, not promises.