Sequence of returns risks in India can silently damage your retirement corpus. Discover 9 hidden dangers, real examples, and proven strategies to protect your retirement income. sequence of returns risks in India, retirement planning India, retirement corpus risk, withdrawal strategy India, investment timing risk, financial planning India, retirement mistakes India.

Introduction: The Retirement Myth That Can Cost You Everything

Picture retirement dreams shaped by years of steady savings across India. Most folks trust that simply staying invested in things like mutual funds or property will pay off after sixty. Yet hidden beneath this hope sits something rarely noticed, capable of shifting results dramatically. Imagine two people doing exactly the same thing – same money put in, same average gains – but one runs dry while the other stays safe. Effort matches. Knowledge aligns. What separates them? When those returns show up matters more than anyone admits. It’s during spending – not saving – that sequence quietly takes control. Many investors believe that avoiding common errors is enough, but even those who understand retirement planning mistakes in India can still face unexpected risks due to poor timing. This hazard tied to timing goes by the name sequence of returns risk. Worst damage strikes right after retirement ends begins, when money moves are hardest to adjust. Little room to bounce back makes fixing mistakes nearly impossible then.

Understanding Sequence of Returns Risk in India

Sequence of returns risks refers to the impact that the order of market returns has on your retirement savings, particularly when you begin withdrawing money from your portfolio. Most old-school money tips talk about average growth, yet what really shapes outcomes in retirement is the order of wins and downturns. Early jumps in value followed by flat or low ones tend to stretch a pot further down the road. But when drops hit right at the start, pulling funds while balances shrink hits hard. That double pressure often drains savings fast, leaving little room to bounce back – even if stocks rally years after. Standard forecasts miss this twist entirely, averaging numbers without showing how timing tilts results. Many people just do not see it coming because their plans ignore when things happen, only counting totals. A person saving alone in India faces tougher odds when there is no steady pension to fall back on. What matters then isn’t just how much money grows, but whether it lasts long enough through ups and downs. Even powerful concepts like the power of compounding: your best friend in investing can fail when early losses combine with withdrawals during retirement.

Why Sequence Risk Is More Dangerous for Indian Investors

The impact of sequence risks is amplified in India due to several structural and behavioural factors that make retirement planning more vulnerable. What hits harder in India is how timing can twist retirement plans, thanks to deep-rooted habits and system gaps. When markets dip early in retirement, it stings more here – there’s rarely a safety net like pensions or state aid to fall back on. Savings carry the full load, so each medical bill or price jump eats deeper into what was set aside. People live longer now, stretching those savings thinner over years nobody fully planned for. Money parked mostly in stocks or property adds tension, especially when cash cannot be pulled quickly. Choices made today echo louder because backup options stay limited, leaving little room to adapt later. This becomes even more complex when portfolio outcomes vary widely across asset classes, especially when compared through real estate vs mutual fund returns in India. Starting off, feelings often steer money choices. Without expert help, mistakes grow more likely. Awareness gaps around pulling out savings make things worse. So it happens – sequence risk isn’t some distant idea here. It shows up real in Indian retirements. Money freedom gets shaky when timing works against you. This becomes clearer when comparing long-term outcomes through real estate returns in 2025: myth vs reality explained in detail, where asset performance varies significantly.

9 Hidden Sequence of Returns Risks in India

1. Retiring Just Before a Market Crash

Right when you stop working, your savings often hit their highest level – built up over many years. A steep drop in prices right then hits harder than usual since that’s exactly when you start taking funds out. Pulling cash from an account that’s shrinking turns paper losses into real ones, leaving less behind to grow later. That shrinking balance gets squeezed further by ongoing draws, making each loss deeper. The mix of spending and falling values pushes the total down faster, feeding on itself. When you are retired, losing money early on hits harder, since there is little chance to bounce back. A dip in markets during the first few years out of work might never get fixed, even if things improve later. Most plans pretend the stock market climbs smoothly, but that is rarely how it plays out in reality. Watching savings shrink makes some people sell at the worst times, which only deepens the loss. How long your money lasts could drop by many years, just because bad luck struck too soon.

2. Fixed Withdrawal Without Market Adjustment

Some older adults take out the same sum each month or year once retired, no matter how stocks behave. Even though that feels steady, it overlooks something vital – how much markets swing up and down. Good years might handle such draws just fine. But when values drop, pulling equal amounts means giving up more shares while prices are low. That eats through savings quicker than expected. When markets bounce back, gains mean less if the account shrank too much earlier. Sticking to the same payout every year tends to drain savings faster than people expect. Pulling out cash in step with what’s happening in the economy helps stretch funds further, though staying alert matters. Most choose steady amounts simply because it feels simpler, missing how it wears down value slowly. That slow fade – often ignored – is a core part of why timing hurts portfolios.

3. High Equity Exposure at Retirement Stage

When you retire, holding too much stock might feel safe if markets rise. Still, drops right at the start can hurt more than expected. Money pulled each year multiplies damage when prices fall. Growth matters less now compared to guarding what is already saved. Some keep investing like they still work, ignoring how timing changes everything. A dip isn’t just a loss – it forces selling low, shrinking funds faster. Even small downturns weigh heavy once spending begins. Markets bounce back eventually, though accounts may never recover fully under withdrawal pressure. Later on, stocks might bounce back. Yet what happens early can stick because there is less money to work with. In India, prices swing hard without warning. Moving slowly into safer funds as retirement comes closer could soften the blow – though thinking ahead is key. Skipping that step usually means more pressure when income stops.

4. Ignoring Inflation During Market Decline

Even when markets stay flat, prices keep growing – this quiet shift chips away at what your money can buy. When stocks drop, that steady price climb feels heavier since costs go up but investment values shrink. Picture needing extra cash just to cover bills, only to pull from accounts already shrinking in size. Pulling out too much without thinking ahead might drain reserves faster than expected. Little changes each year add up until there’s less left than planned. In India, rising costs for health care and daily needs make financial risks harder to manage over time. Instead of just chasing investment gains, people often overlook how inflation eats into actual spending power. To plan well, thinking ahead about living costs matters – plus adding extra room when markets dip helps too. When this piece gets ignored, what seemed like a solid retirement plan might unravel under pressure.

5. Lack of Emergency or Liquidity Buffer

When markets dip, selling investments often means locking in losses – a risk many overlook. Instead of tapping into portfolios right away, having cash aside helps avoid bad timing. Most people assume they can pull money out when required, but that idea falls apart in tough times. Picture needing funds suddenly: car trouble, health bills, or home fixes – all easier handled if savings sit ready. Keeping everything in stocks might work on paper, yet real life does not follow schedules. Cash set aside for roughly twenty-four to thirty-six months of spending gives breathing room. That way, down markets do not decide withdrawal dates. Emergencies come unannounced; reacting should not mean cutting into growth assets. Surprises often creep in where you least expect them – like forgotten accounts gathering dust while dreams quietly unravel. Money tucked away and ignored might feel safe, yet it can quietly weaken long-term stability. Staying flexible with cash flow does more than protect – it reshapes how risk plays out when timing works against you.

6. Emotional Reactions to Market Volatility

When markets get shaky, feelings often take charge instead of logic. Instead of staying steady, many people pull out fast when prices drop, hoping to dodge pain. Yet stepping away at lows means they’re not around when things bounce back. What could be short-term dips turn into real damage over time, hitting future savings hard. Fear spreads easily, especially if someone does not grasp how cycles work. Learning helps. So does sticking to a plan, even when noise gets loud. Wrong money choices go beyond just investments – take India’s frequent credit card dispute errors, born from confusion about how finance rules work. Staying steady with a clear strategy helps dull emotional triggers, yet demands active attention plus self-reflection. Starting over after missteps means seeing patterns before they repeat.

7. No Defined Withdrawal Strategy

Most people put effort into saving for later years. Yet hardly anyone thinks ahead about taking money out wisely. Pulling funds without thought can clash with how markets move or what the future needs. Acting without direction might mean grabbing too much when things look good or staying stuck when times get tough. That kind of pattern opens the door to early losses piling up. Smart moves depend on watching prices shift, costs rise, and where investments sit. Staying steady relies on having steps to follow, so rash choices fade away. Out here in India, where putting aside cash usually means just piling it up, that missing step matters more than most notice. Thinking about change? It starts by treating money not like a stockpile but something alive, moving through years when work stops.

8. Overdependence on One Asset Class

Putting money in different places matters a lot when investing, but plenty of people who stopped working still tie up most savings in just one type, like houses or bank deposits. When that happens, losses hit harder if that area struggles – something older adults can’t always afford. Imagine home prices dropping or tenants vanishing; suddenly, monthly funds shrink fast for anyone counting on rent. The same goes for savings accounts when banks pay almost nothing in interest. Money sits there, growing slower than needed. Most folks think owning lots of different things protects their money. Yet spreading cash around without a plan rarely works well. Picture this: retirement changes how investments should behave. Just piling up stocks, bonds, or real estate does little if they don’t fit together. A shaky mix might crumble when early withdrawals hit during bad years. Balance matters more than quantity ever could. This is why investors often rely on diversification tools like gold as a safe haven during uncertain periods.

9. Delayed Financial Adjustments

Slipping past notice, slow shifts in money situations spark big trouble if ignored. When markets dip or life throws changes, sticking rigidly to old habits invites unnecessary loss. Take someone pulling large sums out while investments shrink – this drains savings faster than expected. Not shifting asset mixes or revising budgets opens the door to greater danger over time. Staying alert matters, watching numbers closely counts, adapting when needed makes the difference – even though many retirement blueprints skip these steps entirely. When things stall, even tiny holdups might ripple out over years. Spotting that shifts are needed, then moving without wait, keeps timing dangers under control.

Real-World Examples

Months into retirement, a person who left work in 2008 watched their investments shrink fast when the financial crash hit. Though they held many different stocks, losing money while also pulling funds out eroded savings deeply. Even once stock values climbed again later on, getting back what was lost stayed out of reach.

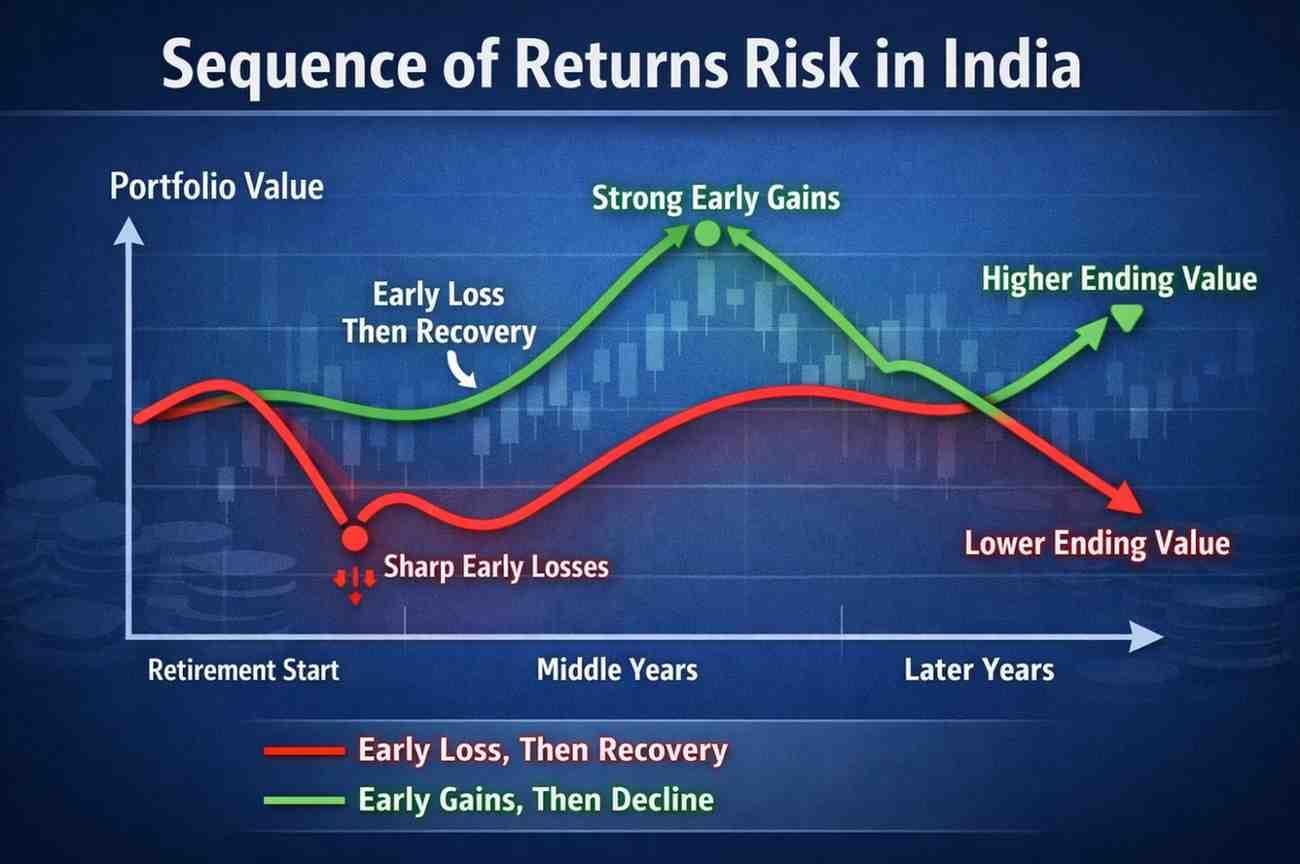

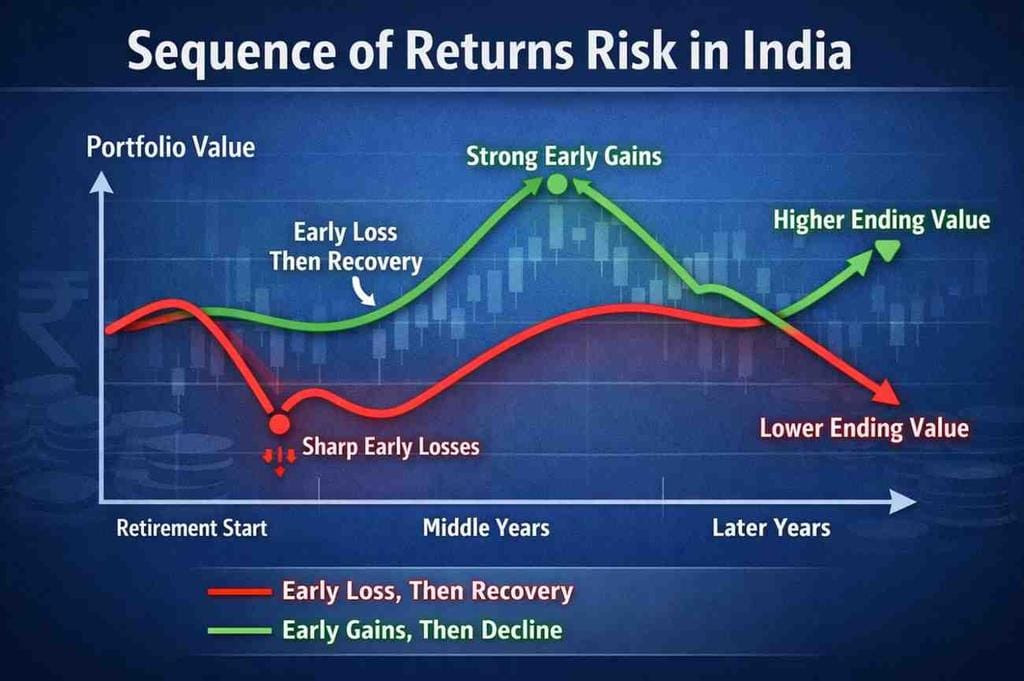

A different case shows two people holding the same mix of investments, both earning similar overall results. One hits rough patches right after retiring, losing money when it matters most. The other sees growth at first, letting their funds grow before any downturns arrive. Early setbacks drain accounts faster, especially when cash is pulled out during drops. Gains at the start create a cushion that helps later on. What happens first can shape everything – even if long-term numbers look equal.

A sudden health issue hit an older adult who had no cash set aside, right when prices were falling. With few options, money had to come out of investments just as values dropped. That move shrank the account balance while weakening future growth. Poor preparation made timing work harder against them.

How to Protect Yourself from Sequence Risk

Starting later does not mean finishing weaker when it comes to handling timing danger in withdrawals. A cushion of ready cash helps absorb shocks if markets dip early. Shifting money between time-based buckets keeps choices flexible as years pass. Slowing down stock involvement close to retirement may soften potential blows. Instead of fixed draws, altering amounts depending on yearly results supports balance over time. Spreading funds across different types avoids heavy reliance on one place. Learning what studies from around the world show adds depth to personal decisions. The point shifts from chasing growth to making resources stretch reliably. Global financial literature explains that early negative returns can significantly reduce retirement sustainability, a concept widely known as sequence risk in investing.

Conclusion

Early loss hits hardest when you retire just as markets slide. Picture taking money out while investments shrink – savings dwindle faster than expected. What matters isn’t just average growth over time, but when gains or losses occur. A rough start can bend the path of your funds far more than later downturns. Long stretches of gain mean little if the first few years drain the pot. Withdrawals during slumps force selling low, which deepens the hole. This pressure builds quietly, often unnoticed until recovery feels impossible. Planning around income needs alone misses half the picture. How cash flows out, what assets back it, and where risk hides matter just as much. Smart strategy prepares not only for earning, but enduring. Understanding official investment guidelines from SEBI can further strengthen long-term retirement planning decisions. Those who see the danger ahead tend to stay in control of their finances when they stop working. Staying alive doesn’t mean much if savings vanish before time runs out.

FAQs

Q1: What is sequence of returns risk in simple terms?

The way that the timing of market gains and losses impacts your retirement funds is known as sequence of returns risk. Early losses can drastically lower your portfolio when withdrawals start, even if average returns are comparable.

Due to the short recovery period, early negative returns are more detrimental than later ones, making this risk crucial throughout retirement.

Q2: Why is sequence risk more important after retirement?

Because they are not taking money out, investors can weather market downturns during accumulation years. Regular withdrawals and losses, however, cause the portfolio to decline more quickly after retirement. As a result, withdrawals and falling asset values have a compounding detrimental effect on long-term sustainability.

Q3: Can diversification eliminate sequence risk?

Sequence risk cannot be totally eliminated by diversification, although its effects can be lessened. Investors can prevent significant losses in a single segment by distributing their investments over a variety of asset types. To properly manage this risk, however, a sound withdrawal strategy and liquidity planning are equally crucial.

Q4: How much cash buffer is ideal for retirees in India?

In general, financial experts advise keeping at least two to three years’ worth of expenses in low-risk or liquid investments. During market downturns, this helps prevent forced withdrawals. Having a buffer greatly increases financial stability, albeit the precise amount may vary based on lifestyle, spending, and risk tolerance.

Q5: Is sequence risk relevant for young investors?

Young investors should be mindful of sequence risk even though it predominantly impacts pensioners. Early comprehension of this idea facilitates better planning and the avoidance of errors in later life. As retirement draws near, it also promotes prudent asset allocation and diligent investing.

Q6: What is the best way to manage withdrawals in retirement?

Fixed withdrawals are thought to be less successful than a flexible withdrawal approach that changes according to market performance. During recessions, this strategy aids in capital preservation. This improves long-term sustainability when combined with a diversified portfolio and bucket approach.

Disclaimer

This article offers general insights meant to inform and educate, never to replace tailored financial, investment, or legal guidance. Markets carry uncertainty; history gives no promises about what comes next. Each person faces unique circumstances, comfort levels with risk, and personal aims. Talking with a qualified money adviser, tax specialist, or investing professional makes sense prior to acting. Responsibility for choices lies with the reader – neither writer nor publisher accepts liability for outcomes.