Learn 9 powerful National Pension System timing secrets to boost returns, maximize tax savings, and avoid costly retirement mistakes easily. National Pension System, NPS timing strategy, NPS tax benefits, retirement planning India, NPS investment tips, NPS returns strategy, pension planning India, tax saving NPS.

Update Note: This article has been updated in April 2026 to reflect the latest National Pension System rules, tax benefits, and investment strategies. All information has been aligned with current regulations, contribution limits, and retirement guidelines. The timing strategies and examples have been refined to match present market conditions and investor behavior.

Introduction: The Hidden Timing Mistake That Costs You Lakhs

It’s common to think putting money into the National Pension System means a solid retirement fund is certain – truth is, it’s not that straightforward. What sets apart regular savers from sharper ones isn’t simply how much they put in, yet when they choose to invest at various points in life. Often, people wait too long to start, contribute only when filing taxes near year-end, or ignore updating plans despite earning more. Tiny choices like these pile up quietly, shaping outcomes years later. Missing out early on, say by three or four years, might cost you hundreds of thousands down the road because growth slips away. Later on, markets respond differently depending on when you put money in, particularly with stocks in play. Sticking to a routine pays off under the National Pension System – much more so than rushing in at deadlines. Those who learn the right moments for boosting payments, changing fund mixes, or using tax rules well usually end up with far bigger savings down the road. Skipping attention to these moments doesn’t only mean lost chances – it quietly chips away at what you’ll have later. For that reason alone, getting timing right inside this system isn’t something extra. It’s required.

What is National Pension System (Quick Understanding)

Starting later does not mean you can’t begin. A government-supported plan called the National Pension System helps people prepare for retirement by putting money into long-term investments. Oversight comes from an agency known as the Pension Fund Regulatory and Development Authority. Instead of fixed interest, what you gain depends on how well chosen assets perform. Growth happens through exposure to stocks, company debt, and state-backed instruments. One part pushes risk higher, another keeps things steady. Over years, results reflect actual market movement, not promises. Sticking with regular contributions becomes easier when structure guides choices. Commitment builds slowly, shaped by consistency rather than sudden shifts. What forms is less about luck, more about showing up repeatedly. What stands out most is the extra tax perk available outside the usual Section 80C cap, turning it into a solid option for managing taxes. Because you can pick how your money is spread across assets – manually or by going with an age-based automatic plan – it fits different comfort levels. Money stays put until retirement, so sudden decisions to pull funds vanish, nudging behaviour toward consistency. As years pass, staying invested lets gains build on gains, riding shifts in market trends without needing constant adjustments. When aligned with broader strategies like the power of compounding, the National Pension System becomes even more effective. It provides a planned route to long-term wealth growth rather than only a retirement product.

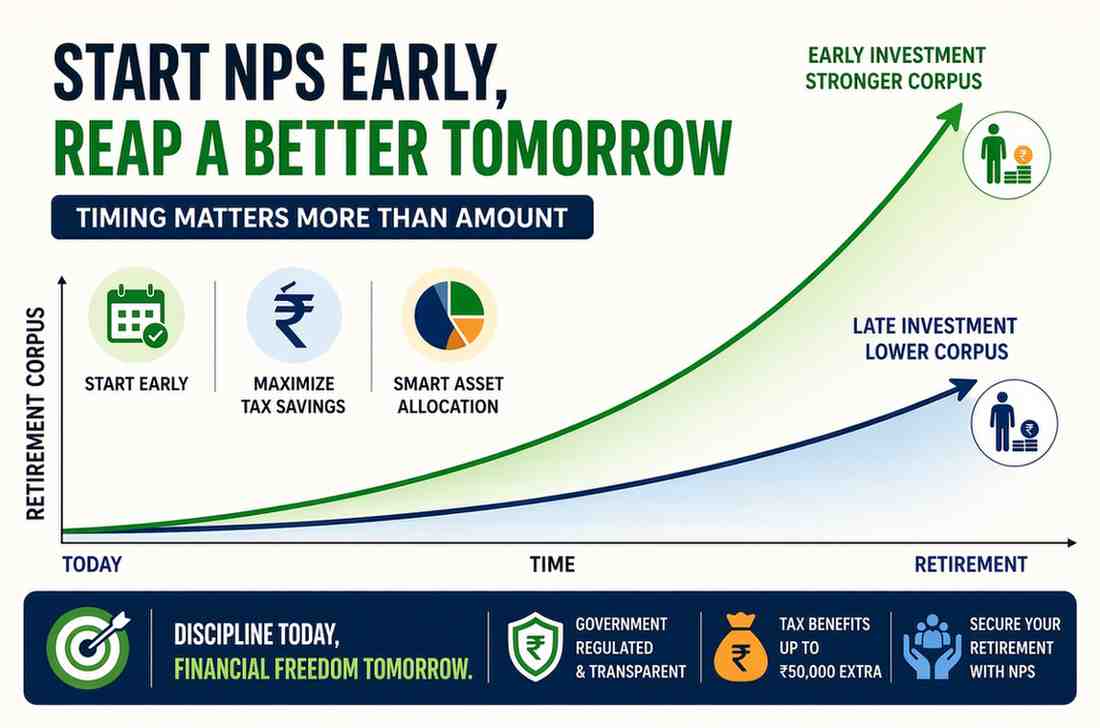

Why Timing Matters More Than You Think

It matters when you put money into the National Pension System because timing shapes growth potential. Some think long-term plans like NPS make entry points irrelevant – yet that idea often backfires quietly. By adding funds steadily throughout the year rather than rushing near March, you smooth out purchase prices naturally. Buying during highs along with dips keeps each contribution’s value from swinging too hard. Later gains grow faster when cash enters early, simply because it sits there building more layers over time. When you put money in shapes whether stocks or bonds make sense right then, changing what you might earn – or lose. People tweaking plans as years pass tend to land in a stronger spot, especially if markets dip. Rough patches open space for smart moves, like adding funds when prices drop. A disciplined approach similar to sip vs lump sum which is better highlights how consistency beats sporadic investing. Whether you are actively building wealth or just saving money ultimately depends on the timing.

9 Powerful National Pension System Timing Secrets

1. Start Early — But Don’t Wait for Perfect Time

Picture this: planting a seed today means watching it become a tree years later. Begin putting money into the National Pension System while young, so each dollar has more seasons to multiply. Kick off in your twenties, tiny amounts add up – thanks to decades of quiet growth behind the scenes. Hesitating until conditions feel just right? That mindset steals time you cannot get back. Stretch out the journey, and suddenly smaller sums each month do the heavy lifting. Putting off investing means saving larger amounts down the road – something that might not work when life gets complicated. Those who begin sooner usually hold more stocks, an approach that often grows wealth steadily across years. That head start builds momentum few can match, regardless of how much extra they add later. Getting started early shapes habits too, turning regular choices into steady progress without needing willpower each time. Time slips under the radar for many savers, yet quietly plays a massive role in building lasting value. Aligning early investments with strategies like investment plan by age ensures that your approach evolves as your financial situation changes.

2. Monthly Contribution Beats Last-Minute Investment

Month after month, putting money into the National Pension System works better than dropping it all in one go near year-end. Because markets move up and down, steady deposits mean buying more shares cheap, less when costly – smoothing out price swings over time. Jumping in late, say around March, leaves gaps where gains could have built. Timing matters, yet waiting raises the odds of choosing a peak instead of an average. Over months, small steps add up quieter, steadier, without chasing highs. Every month putting money aside builds a steady way to invest, fitting well with big future plans. Because it happens regularly, the stress of dropping in huge amounts suddenly fades away. Little by little, showing up the same way each time strengthens how your investments grow and hold value. People using this step-by-step approach often do better than those jumping in randomly. Spreading moves across months means dealing with taxes feels lighter, never piling up near deadlines.

3. Increase Contribution at the Right Income Stage

When pay goes up, putting more into the National Pension System keeps things balanced with what you aim to achieve financially. Often people stick to the same amount despite earning much more now. That choice slows down how fast savings can grow for later years. Boosting deposits after a raise or extra income speeds up gains while still living comfortably. It opens doors to bigger tax advantages allowed by NPS rules too. Slowly raising what you put aside helps match rising costs and shifts in money demands later on. When people stick to the same amount, they usually end up short when it’s time to stop working. Building a plan that grows as your pay check does tends to bring stronger stability years ahead. That method works best if steady saving is already part of how you manage funds. The point isn’t sudden big deposits into accounts. It’s growing them thoughtfully, bit by bit, across months or years.

4. Choose Equity Allocation Timing Carefully

Picking how much stock goes into your pension plan shapes what you get back over time. Young people often handle more stock risk since they wait out rough markets better. Getting nearer retirement means stepping back from stocks helps keep savings safe. Shifting at the right moments lets gains grow early, then stay steady later. Staying heavy on stocks near retirement might cost big when markets drop. Later years might reward bold moves, yet playing it safe at the start could hold back gains. Instead of sticking rigidly, shifting investments gradually fits changing life stages better. As time passes, matching exposure to personal comfort with risk becomes more natural. Moving money between stock and bond options at the right moment shapes outcomes strongly. How soon or late adjustments happen directly influences total savings built.

5. Avoid Market Timing — But Use Market Awareness

Success in the National Pension System does not depend on guessing where markets will go next. Market awareness, though, might just sharpen how you plan ahead. When values dip, boosting your payments means grabbing more units without paying much. Timing every shift precisely? Not required – better results come from steady moves when things sag. Selling fast when prices tumble turns paper drops into real harm. Holding firm through swings keeps you in line for rebounds later down the road. Recovery favors those who do not bolt at the first sign of trouble. Staying invested for years means waiting calmly instead of reacting every time markets twitch. Noticing what happens in finance lets people choose wisely – yet still avoid guessing games. When prices swing wildly, those who keep going usually end up ahead. Growth over decades matters more than quick wins when building wealth slowly. Doing the same things steadily beats trying to outsmart tomorrow’s numbers.

6. Use Tax Timing to Your Advantage

Most people overlook timing when using the pension system for tax perks. Yet savings grow stronger when deposits happen early, not rushed in March. Think ahead – putting money in step by step opens full access to write-offs like 80CCD(1) and extra breaks up to 50K. Moving cash gradually means shares get bought at different levels, lifting overall gain chances. Heavy lump sums strain budgets; smaller chunks ease pressure without sacrificing benefit size. Most people overlook how timing affects their taxes and investments at once. Yet shifting when you act can boost what stays in your pocket while growing wealth steadily. Those thinking months ahead often claim full deductions but still keep cash ready if needed. Instead of waiting until deadlines loom, fitting tax steps into investing choices makes sense mid-year too. When moves align just right, money works harder without extra risk.

7. Switch Active vs Auto Choice at the Right Time

Picking either active or automatic investing in the National Pension System comes down to how hands-on you want to be and what you know about markets. When you go active, you pick where your money goes – helpful when you grasp how prices shift over time. The system shifts funds by itself with auto mode, cutting exposure to risk gradually as retirement nears. Timing matters when moving from one method to another so savings stay on track. Those just starting out might gain more by steering investments themselves while aiming high for long-term gains. When retirement gets closer, picking autos might offer steadier footing. Getting the moment right keeps risk and gain in line. Some people skip this step then face too much danger or leave gains behind. Shifting as life changes tends to work better over time. Knowing the shift point often leads to stronger results down the road.

8. Plan Exit Timing Strategically

Leaving the National Pension System matters just like building it up. When work ends, take some savings out at once, though what stays needs to buy a steady payout later. How timing plays out shapes both cash in hand and future flow. Markets high when pulling money means more value locked in. The moment picked for securing regular payments shifts how much arrives each month afterward. Bad timing might mean smaller gains and less stable finances. Because preparation helps, choices around pulling out money or putting it back in become clearer. Without a clear plan, many investors overlook key moments that matter. When the exit is thought through, shifting from saving to earning feels natural. Timing matters just as much as thinking things through here.

9. Align NPS with Overall Financial Strategy

Think of the National Pension System as one thread in a larger fabric, not something set apart. Instead it fits better when woven together with tools like mutual funds, EPF, or steady income assets. From that mix comes balance – room to grow, stay stable, and still reach into your money when life shifts. Put all focus only on NPS and movement gets tight, options shrink. Spread across different lanes, risk softens even as results gain ground. Structuring your investments through models like 3 bucket portfolio in India provides clarity and balance. Money set aside today can cover near-future expenses, while still feeding into bigger targets down the road. When NPS fits smoothly within your full plan, pieces link without friction. A connected system like this builds stronger protection over time, growing value steadily behind the scenes. Stability takes root when every part moves in step, not just for now but years ahead.

Tax Benefits of National Pension System

One way Indians save on taxes? The National Pension System gives a broad setup for that. Put money in under Section 80CCD(1), it counts toward the ₹1.5 lakh cap set by Section 80C. Beyond that limit, here’s something extra: Section 80CCD(1B) lets you deduct another ₹50,000 – rare among most savings paths. When employers chip in, Section 80CCD(2) kicks in, adding more room to lower taxable income depending on how pay is split. Most people find NPS appealing because it lowers what they owe in taxes. When arranged well, every deduction counts – without locking away more money than needed. Using each part of the plan wisely cuts down how much income gets taxed. Less tax means more stays in your pocket, changing how far each invested rupee goes. Government guidelines and updates can be accessed through Income Tax official portal and Pension Fund Regulatory and Development Authority (PFRDA). You can make better financial decisions if you are aware of these provisions. When applied properly, NPS can be utilized as a strategy to reduce taxes and increase wealth.

Common Costly Mistakes to Avoid

Investing in the National Pension System often goes off track because people rush into it just before tax season ends. Instead of planning ahead, they treat it like a quick fix for taxes. This shift in timing messes up their long-term goals. A rigid mix of assets stays unchanged even when life changes around them. Over time, that rigidity chips away at potential gains. When salaries go up, contributions stay flat – leaving money on the table. Growth slows down without regular boosts to savings. Markets dip, nerves jolt, some freeze and pull out completely. That pause means sitting idle when rebound chances rise. Most people do not realize how withdrawal rules affect their choices when leaving the NPS. Because they see it apart from everything else, many fail to connect it with their overall money strategy. Timing shifts in where funds go or when deposits happen – often brushed off – carry weight later on. Small slips today? They grow heavier over years. When those errors fade away, performance quietly improves.

NPS vs Other Investment Options

One big plus of the National Pension System? Returns tied to the market, so gains might grow more over years. Fixed deposits can’t do that. Instead of steady interest, think shifting value based on performance. Tax perks stand out too – few investments match those cuts. Not every plan lets you save quite like this one. Yet getting money out early isn’t allowed; wait till retirement, no exceptions. Mutual funds let people pull cash faster, though they cost more over time. Lower fees in NPS help keep expenses down. Flexibility takes a hit, sure. Still, long-term planning gets a quiet boost here. Long-term retirement fits better with this plan compared to quick money targets. Alongside other assets, it creates a steadier path toward building value. Fixed deposits bring steady footing. Mutual funds on the other hand open room for gains over time. Spotting how they differ guides smarter choices across options. Used inside a varied collection of holdings, its strength shows more clearly than when standing alone.

Advanced Strategy Most People Miss

Now here’s something few people pay attention to – changing how much you put into your pension and where it goes, depending on how markets move and where you are in life. Sticking to the same plan all the time tends to hold back growth. When prices drop, putting in more money means buying at better rates. As retirement gets closer, shifting slowly away from stocks shields what you’ve built up. Timing investments alongside tax decisions just makes everything work smoother. Mixing NPS into broader financial plans builds something sturdier, able to shift when needed. Those who tweak their moves often outperform folks sticking rigidly to one path. Watching how markets rise and fall helps shape smarter choices at the right moments. Staying alert and consistent matters here – results grow over years, not days. Changes do not need to be constant; timing and thought make the difference.

Real-Life Examples

Example 1: A young investor, just twenty-five, begins putting five thousand rupees each month into the National Pension System. As pay goes up, so does the amount saved – slowly but steadily growing over years. Wealth grows faster later on, thanks to money made from earlier gains piling up. Sticking to the plan while raising savings at smart moments leads to a solid fund for later life. Starting early, paired with steady choices, quietly builds strength that lasts decades.

Example 2: Thirty five years old when he began, the man put ten thousand rupees every month into NPS, trying to catch up. Though his payments were large, what he gathers at retirement still falls short of another person’s who started sooner. Years skipped mean compound interest had less room to build. Waiting to join the National Pension System ends up shrinking future savings by lakhs. What slips away quietly is hard to regain later.

Example 3: Most years, a single payment comes through – March is chosen just to cut taxes. Yet skipping the rest of the months means missing low prices when markets drop. Buying all at once keeps each share more expensive in the long run. Spreading buys out slowly usually brings down that average price. Returns shrink, not because money was lacking – but due to mistimed moves.

Example 4: Close to retirement, one investor holds on to heavy stock investments through NPS without shifting strategy. When markets drop right before they stop working, their savings shrink fast. Had moves happened sooner, damage might have been smaller. Right moment matters most when reshaping where money sits.

Conclusion

Timing shapes the value of what you build inside the National Pension System more than effort alone ever could. From the moment someone begins until they step away, each phase bends the outcome differently. A misstep in scheduling might drain potential years later, whereas clear thinking boosts results quietly. Staying steady matters far beyond knowing which button to press or form to fill out first. Success shows up most often where habits meet attention, not noise or speed. Most gains in NPS come when contributions, fund splits, and tax moves work together without friction. Think of NPS as one piece in a larger money plan, not some magic fix on its own. Done right, it quietly builds strength over years, shaping what retirement looks like. Small shifts in start time matter more than long hours pushing numbers later.

FAQs

Q1: Is the National Pension System appropriate for every investor?

True, this fits well with lasting retirement goals, particularly if steady contributions and tax perks matter. Still, anyone needing quick access to money might find it less fitting.

Q2: Can I alter my NPS investment strategy?

Changing how you split up investments? That’s doable. Shift from active picks to automatic settings whenever life changes direction. Your plan bends instead of breaking when priorities shift down the road.

Q3: What would happen if I stopped making contributions to NPS?

Your account is still active, but depending on the donation guidelines, you might be subject to limitations or fines. To optimize benefits, it is best to continue making monthly contributions.

Q4: How much money should I put into NPS?

Your income, financial objectives, and retirement requirements will determine the amount. Better results are guaranteed by a methodical approach that gradually increases contributions.

Q5: Is NPS superior to mutual funds?

One works toward later years plus cuts taxes. The other moves with your needs, opens when you want it. Mix them right, get steady ground. Five

Disclaimer

This article aims to inform, not guide your money choices. When weighing investments, personal targets matter more than general tips. Instruments tied to market shifts – NPS included – can rise or fall without warning. Past performance gives no promise of future results. Rules around tax benefits might shift tomorrow, next year, whenever. Check what applies today, not yesterday. Guidance shaped by license and training often brings clarity others can’t.