Learn the truth about personal loan foreclosure charges in India, hidden fees, GST, lock-in periods, RBI rules, and smart ways to maximize savings before closing a loan early. personal loan foreclosure charges, foreclosure fee on personal loan, personal loan prepayment charges, loan closure charges, personal loan foreclosure rules, personal loan early repayment charges, loan prepayment penalty.

Introduction to Personal Loan Foreclosure Charges in India

Getting money fast might be why people take personal loans – sudden expenses, school bills, big life events, fixing up a house. When someone starts earning more, paying off the loan ahead of time begins to sound smart, cutting down what they owe later. Yet ending a loan early does not guarantee clear wins. Charges pop up: lenders tag on exit penalties, extra fees, tax layers, paperwork costs. What looked like progress sometimes slips away once numbers arrive in a closure notice. Surprise waits often at the end, right after asking for that final balance report. Lenders are required to disclose loan-related charges and terms transparently under regulatory guidelines issued by the Reserve Bank of India (RBI). Foresight into fees tied to closing a personal loan ahead of schedule matters greatly when planning repayment in India. Weighing what it costs against what you gain might reveal if settling early fits how things stand for you.

What Is Personal Loan Foreclosure?

Paying off a personal loan early is what loan foreclosure means. When someone settles the full principal along with any interest built up, taxes due, and extra fees, the bank shuts the account for good. Unlike partial payments that just lower part of the balance but keep the loan active, this wipes it out completely. Some people go this route after getting a bonus, money from an investment maturing, profits from their work, or another large sum arriving at once. Cutting down on long-term interest and being free of debt sooner often drives the decision. Borrowing trouble might come even when avoiding mortgage default seems smart, since banks often add extra fees without warning. Each cost needs close inspection before signing anything.

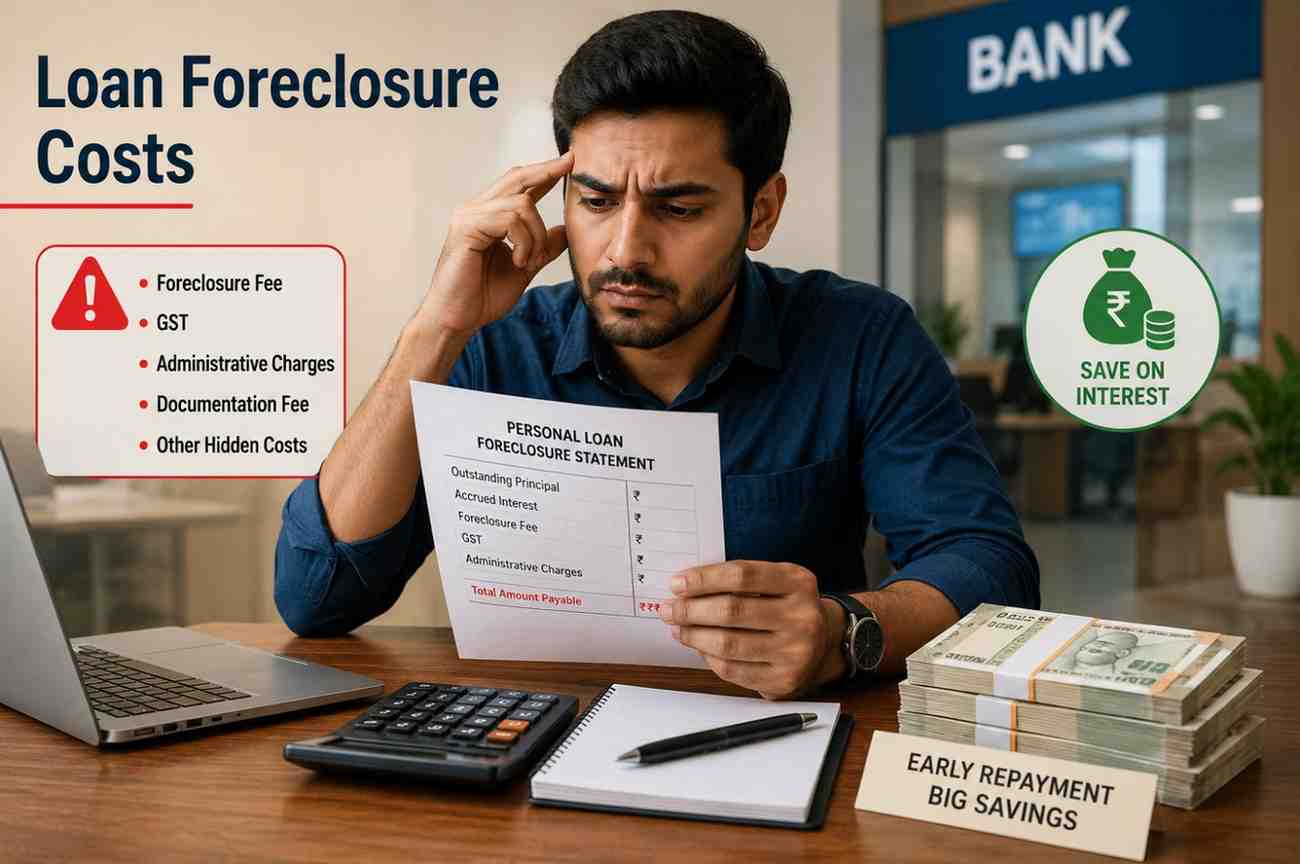

1. Foreclosure Fee Is Often the Largest Hidden Expense

Borrowers often face one big cost when paying off a personal loan ahead of schedule – that’s the foreclosure fee. Since lenders won’t collect the interest they counted on later, they apply this charge instead. A chunk of what you still owe becomes the base for the calculation. Some banks take between 2% and 5%, pulled straight from your unpaid sum. How much gets added depends entirely on who gave out the loan. Twenty thousand rupees might seem sudden when you owe five lakhs and face a four percent exit charge. Yet folks often fixate on interest drops, forgetting such fees exist at all. So what feels like progress could shrink once numbers settle. Picture weighing that penalty against payments you’d skip down the road instead. Clearer choices come from balance, never guesses.

2. Lock-In Period Restrictions Can Limit Your Flexibility

Some people think paying off a personal loan early is always an option once funds are free. Yet most banks and financing firms set a waiting window before allowing full repayment. Usually that span lasts half a year to one full year starting from when cash hits the account. A sudden windfall – like a hefty bonus or lump sum – won’t change much if it arrives too soon. Lenders often reject closure attempts made while still inside this restricted stretch. Borrowers usually fixate on monthly payments instead of fine print details hiding in lending contracts. Those rules about early repayment tend to get ignored until later. It pays to check exit options before signing anything. Lower charges upfront might come with strings attached down the line. Flexibility matters just as much as cost over time when picking a loan.

3. GST on Foreclosure Charges Can Increase the Final Bill

Borrowers often figure out the foreclosure cost right, yet overlook the extra tax tagged onto it. Because lenders see this charge as a kind of service, GST tends to kick in. That pushes the total payment higher than most plan for. Say someone faces a ₹15,000 fee – what they actually pay climbs once the government levy joins in. That extra fee might look tiny compared to the full loan, yet it chips away at what you save by paying early. So get the total payoff number straight from the lender instead of guessing with separate fees. A clear foreclosure breakdown removes guesswork. When math is precise, choices rest on facts, not fragments.

4. Administrative Charges Can Reduce Overall Savings

Lenders sometimes add extra charges when wrapping up a loan – fees tied to paperwork, checks, settling balances, or shutting accounts. Not every closing includes them, yet they pile up alongside bigger expenses like foreclosure penalties. Often tiny next to those main costs, they still shift how much you pay overall. People miss these bits, eyes stuck on lump sums involving borrowed amounts and interest rates. Similar surprises occur throughout the borrowing process, which is why many people underestimate the impact of hidden charges in personal loans. Borrowers need to know every fee involved when thinking about foreclosure. Getting a full list of charges from the lender helps avoid confusion. This breakdown makes it easier to see real savings clearly.

5. Interest Continues Until the Loan Is Officially Closed

Some people think paying off what they owe finishes everything. Yet banks still add daily charges right up to the day money arrives. The number seen online might already be outdated by then. Even after sending funds, interest grows until the system marks it closed. What shows today won’t match tomorrow’s total. Payments need extra time to clear completely. Only once processed does the balance truly stop rising. Linger just a couple days, the total owed might creep higher. When borrowers send money without checking the latest foreclosure figure, they sometimes miss a leftover sum. That tiny gap? It holds up closing, adds hassle. Right before paying, pin down the exact number due – it sidesteps those snags. Know how interest builds; it clears paths through confusion, stops shocks at the finish line.

6. Part-Prepayment Rules Can Influence the Value of Foreclosure

Lenders sometimes let people pay off chunks early instead of waiting until the full payoff. Yet hidden rules can catch you unaware even when such options exist. Only after several monthly payments might one lender grant access to early settlement features. A different provider could cap how many times each fiscal year allows such moves or set floor limits on transaction size. When these factors come into play, the pace of principal reduction might shift – changing total interest paid over time. Making early payments smartly could trim costs even if the account stays open longer than expected. Someone who is still evaluating different repayment approaches may discover that a few practical personal loan repayment tips can reduce interest costs while preserving financial flexibility. Knowing these guidelines enables borrowers to select the best course of action for debt reduction.

7. Balance Transfer Costs Are Frequently Underestimated

Borrowers sometimes move a personal loan to a different lender through what is called a balance transfer. This switch usually promises a smaller interest amount over time. Yet things rarely go exactly as planned when you look closer. One bank might add closing penalties just for leaving early. Another could ask for payment on paperwork, checks, even file handling before approving anything. Once every added expense piles up, any savings start fading fast. Most people look at the headline rate first – yet what matters more is how much cash they actually keep. Shifting debt around isn’t always needed if the bank you’re already with will talk numbers. Borrowers who are considering alternatives before foreclosure often explore ways to reduce personal loan interest rate rather than paying a substantial closure fee. Before choosing to transfer a loan, a thorough cost analysis is necessary.

8. Loan Closure Documents Are More Important Than Most Borrowers Realize

Payment cleared doesn’t mean everything’s done. Getting paperwork from the lender shows the debt is truly finished. A No-Dues Certificate might arrive first, then a letter stating the loan closed. Sometimes an updated account summary comes too. Proof like this helps if someone later claims money is still owed. Credit reports may need correcting – these papers back up your case. Years go by before some realize their paid-off loan shows as open, thanks to slow or wrong updates from the lender. Fixing this gets tough when paperwork is missing. Saving both printed and electronic versions of payoff letters just makes sense over time. Proof like that confirms the debt is gone, which shields someone down the road. What matters most? Having something real to show it ended.

9. Credit Report Updates Can Affect Future Borrowing

Surprisingly few realize closing a loan doesn’t mean bureaus see it right away. Lenders might send updates, yet delays happen before changes show up. After foreclosure, checking the status makes sense – just to be sure. A listing that still looks open? That one can quietly block new borrowing chances. Later on, checking your credit report ensures changes show up right. For anyone thinking about loans ahead, getting this done matters more than it might seem at first glance. Anyone unsure about the process can check credit score in India for free and review account information directly from their credit report. Frequent monitoring aids in spotting mistakes before they develop into more serious issues.

10. Opportunity Cost Is the Most Ignored Foreclosure Charge

Lenders might not see all expenses tied to foreclosure right away. The largest unseen hit often comes from pulling personal cash to cover closing costs. That money could’ve earned returns somewhere else instead. Walking away from reserves means less cushion when surprises strike. Picture draining savings just to clear debt – then facing hospital bills or unemployment with empty accounts. Tough spot. When returns on certain investments beat the actual loan cost, paying off debt fast might backfire. Instead of rushing to clear balances, weighing real-world impacts matters just as much as numbers. Clearing debt feels good – yet stability counts more than speed. What looks like progress could slow growth elsewhere.

When Does Foreclosure Make Sense?

Most times, people look at paying off loans early if rates are steep and many years still left on the schedule. Suddenly having extra money – like from a bonus, payout, sale profits, or an inheritance – tends to spark that thought. When payments eat up too much each month, getting ahead of debt might open room for other plans. Savings down the line on interest could outweigh what it takes to close the loan now. Wiping out debt can lift a heavy weight off your mind. Still, taking this step makes most sense if you still have backup funds once payments stop. It feels like a clearer path when the money saved on interest clearly overshadows what you must pay. Crunching numbers carefully shows if walking away really adds up.

When Should You Avoid Foreclosure?

Closing a loan early might not make sense near the end of its term since nearly all interest is already covered. Instead of rushing into it, think twice if you’d need to drain reserves meant for emergencies. Sometimes fees, taxes, and paperwork costs eat up much of what you hoped to save. Those facing irregular pay checks often stay better off keeping cash handy. Paying everything at once could leave them stretched too thin. Understanding the broader disadvantages of personal loans can help borrowers evaluate whether reducing debt immediately should be the priority or whether a more balanced approach is appropriate. Instead of generating new financial concerns, every foreclosure decision should promote long-term financial stability.

RBI Rules on Personal Loan Foreclosure

No one-size-fits-all rule exists for foreclosure fees on personal loans in India. Each bank or non-banking financial company sets its own rates – so long as they tell customers clearly what applies. Look closely at documents like the approval letter, contract, and fee list before agreeing to anything. Rules emphasize clear communication instead of forcing everyone to charge the same amount. When something feels off about how a fee was handled, start by talking directly to the lending institution. If the issue remains unresolved, borrowers can escalate the complaint through the RBI Integrated Ombudsman Scheme. The RBI’s grievance redressal procedure may then be used to escalate unresolved complaints. The greatest method to prevent disagreements later on is frequently to be aware of lender policies before taking for a loan.

How to Calculate Whether Foreclosure Is Worth It

Figuring out how much you save through foreclosure? Begin with guessing the total interest due if payments went on till the end. After that, take away costs like legal fees, taxes, paperwork charges – anything extra tied to closing early. What stays after those cuts – that number is close to what you actually keep saved. When savings stay strong, plus a solid cushion sits untouched, avoiding foreclosure might make sense. Crunching real figures often leads to smarter choices than chasing the idea of zero debt fast.

Real-Life Examples

Example 1: Rajesh, a software engineer in Bengaluru, had three years left on his personal loan debt of about ₹4.5 lakh. He chose to assess foreclosure after getting a sizable yearly bonus. According to the lender’s declaration, there were around ₹22,000 in foreclosure charges and taxes. Even though the fees were high at first, they saved more than ₹75,000 in interest over time. He made the decision to foreclose on the debt after carefully examining the two figures. Early payback would still result in significant long-term savings, according to the computation.

Example 2: A personal loan from an NBFC was already with Neha when a bank offered her one at a reduced rate. Right away, shifting balances seemed like the move. Yet once she added up exit penalties, paperwork costs, and extra charges, the gain looked thin. Even so, because six months shy of five years were left on the original term, some money was still saved overall. What stands out is how full expenses matter more than just chasing a better rate.

Example 3: Right after closing his personal loan early, Amit felt relief. Yet months passed before a hospital visit changed everything. Cash ran short fast when no savings were left to pull from. He reached for a new loan, costlier than the last one. That earlier win now seemed less clear. Freedom from debt looked good – until it didn’t. Money tucked away quietly often matters most when life spikes unexpectedly. Even smart moves can backfire without backup plans breathing nearby.

Conclusion

Foreclosure on a personal loan can be a useful tactic for lowering future interest costs and paying off debt sooner. But the outstanding principle amount should never be the only consideration. The real financial advantage may be greatly impacted by opportunity expenses, GST, administrative fees, credit-report implications, and foreclosure fines. Borrowers are more likely to make wise financial decisions if they carefully weigh savings against expenses. Those facing disputes regarding loan charges or service-related issues can also seek guidance through the National Consumer Helpline. Get a thorough foreclosure statement, go over all relevant fees, and make sure you have enough emergency reserves before moving forward. While a poorly planned foreclosure may result in preventable financial hardship, a well-planned one might improve financial wellness.

FAQs

Q1: What are the foreclosure fees for personal loans in India?

Lenders slap extra costs on borrowers who clear personal loans ahead of schedule. Not every bank or NBFC does it the same way – some charge more, others less. Paying off debt fast might seem smart until these fees eat into what you thought you’d save.

Q2: How much do lenders often charge for foreclosure?

Lenders often take a slice from two to five percent of what you still owe, yet numbers shift depending on who’s lending. Before asking to close out your loan, check what fee sticks. That detail matters every time.

Q3: Is GST applicable on foreclosure charges?

Yes, as foreclosure fees are considered service-related expenses, GST is typically applicable. This raises the total settlement sum above the actual foreclosure cost.

Q4: Can I foreclose on a personal loan as soon as it’s disbursed?

Not all the time. Foreclosure requests are prohibited during lock-in periods imposed by many lenders. Lender policy determines the precise time frame.

Q5: Does going through foreclosure raise my credit score?

Closing loans responsibly can improve your credit profile as a whole. Foreclosure by itself does not, however, ensure a higher credit score because credit scores are influenced by a variety of circumstances.

Q6: What paperwork should I get following a foreclosure?

A final account statement, loan closure letter, and no-dues certificate should be obtained by borrowers. These records attest to the loan’s full settlement.

Q7: Is foreclosure always preferable to making ongoing EMIs?

No. Interest savings, foreclosure expenses, liquidity needs, investment opportunities, and long-term financial objectives all influence the response. Every circumstance needs to be assessed separately.

Disclaimer

This article serves education and information needs. Yet it does not stand as guidance on money, law, taxes, or investments. While one bank might close a personal loan early under certain rules, another could apply different ones. Because lenders set their own ways, checking details straight from your provider matters. Rules shift slowly, sometimes without warning. What fits one person’s situation might not suit someone else’s at all.