Learn how to decide your Ideal Savings Account Balance with smart savings rules, emergency fund planning, inflation protection, and practical money strategies for 2026. Ideal Savings Account Balance, how much money should be in savings account, emergency fund amount, ideal bank balance, savings account planning, savings strategy 2026, savings account limit, how much cash to keep in bank, smart saving habits, inflation and savings.

Update Note: Updated in May 2026 with smarter liquidity strategies, inflation-adjusted savings planning methods, emergency fund rules, and modern cash management techniques for Indian savers.

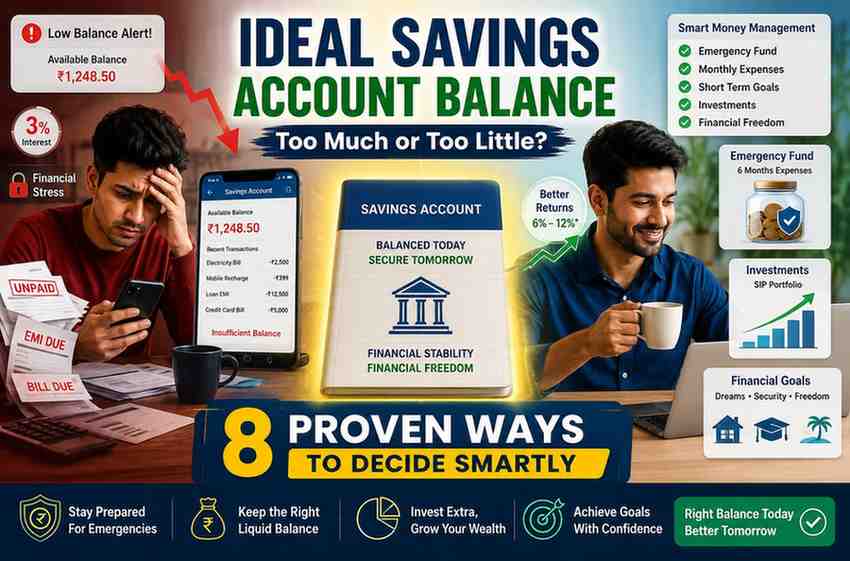

Introduction

Most folks now struggle to figure out how much cash ought to stay in their accounts. A full balance brings comfort to some, yet many choose to put nearly every dollar into investments instead. Between those choices sits something better. Security matters – just not at the cost of future growth. What you aim for is enough cushion to sleep well, but still move forward steadily. Picture 2026 – prices climb fast, paychecks feel smaller, hospitals surprise you with bills. Money moves mostly through phones now, jobs shift without warning. Stashing almost nothing leaves stress when storms hit. Piling up too much means slow loss of value, even if it feels safe. A middle path works best: enough cushion to breathe, yet funds stay active instead of sleeping forever. Finding that point isn’t magic – it’s choices shaped by routine costs, sudden needs, future goals. Here’s how regular people size their savings number using clear steps, actual cases, advice from planners who’ve tested ideas, tools built for today’s economy.

Why Your Savings Account Balance Matters More Than You Think

Most folks see a savings account just as storage for extra cash, yet its real job goes way beyond that these days. Think of it like the nerve hub where pay checks land, monthly dues get paid, loan instalments leave, digital transfers happen, coverage fees vanish, market moves start, memberships renew, and surprise costs show up. When funds dip too far down, one tiny unplanned hit might shake everything loose, pushing borrowing into motion. On the flip side, letting big amounts sleep there earns almost nothing while rising prices quietly eat away what those rupees can buy. You can also track official banking updates, repo rate changes, and financial system guidelines through the Reserve Bank of India (RBI) website. Having a clear plan for how much to save brings freedom in money choices, boosts readiness for surprises, yet keeps reliance on borrowing at bay when times get tough. Missing automatic payments slips away along with fees, cutting tension around daily finances. Some who manage money well now see their savings less like a vault, more like a flow controller for ready cash. Because of this shift, handling available funds with care matters more than ever by 2026.

People who want to improve their banking structure often combine emergency planning with better liquidity strategies through smart cash management approaches and long-term wealth planning habits.

What Is an Ideal Savings Account Balance?

A healthy savings cushion means having enough cash ready for bills, surprises, big purchases, or sudden needs – without touching invested funds or borrowing. Not every person fits one number; paychecks, life demands, debts, household size, and plans shift what makes sense. A public servant might sleep fine with less set aside than someone earning project by project. Picture a solo renter versus parents juggling tuition, loan payments, health costs, and coverage – that changes the game fast. Too little leaves you shaky. Way too much could mean missed chances elsewhere. Comfort matters. Flexibility too. Money should feel steady, not stuck. A bit left over can grow if put to use. Think of it like this: the right amount saved sits where safety meets opportunity. Not too tight. Not too loose. Just enough so life feels calm, yet progress keeps moving. Understanding deposit protection rules through the Deposit Insurance and Credit Guarantee Corporation (DICGC) can also help savers feel more confident about banking safety.

8 Proven Ways to Set Your Ideal Savings Account Balance

1. Follow the Emergency Fund Rule Carefully

Start by setting up an emergency fund before anything else when figuring out how much to keep in savings. Most advisors suggest having cash ready to cover basic costs for three to six months straight. When job loss hits, health issues come up, pay gets delayed, work slows down, or sudden family needs arise, that money cushions the fall. In cases where earnings are steady – like receiving a public sector pay check or pension – a smaller buffer covering just three months might do. Still, those who work freelance, run their own business, lead start-ups, or earn via commissions usually require half a year to a full year of backup funds due to unpredictable pay. Rent, food, medication, power charges, insurance costs, loan payments, travel needs, plus necessary household spending must be included in that safety net. Often, folks overlook this step – until trouble hits, leaving them stuck borrowing at steep rates. When savings hold steady through storms, big-picture goals stay untouched, safe from early taps. Confidence grows when money is ready before chaos knocks.

A strong emergency strategy becomes even more effective when combined with practical emergency fund planning in India for uncertain situations.

2. Separate Daily Spending Money from Emergency Savings

Most folks mess up their budget when every dollar sits in just one place. When everyday cash blurs with backup funds, spotting how much goes where gets messy fast. Try splitting things instead – give each pile a job. Some covers rent, food, apps you pay monthly, gas, digital transfers. That way nothing drifts aimlessly. Leave some set aside – only for real crises. Try splitting money into parts: one for trips, another for yearly coverage updates, school costs, or quick targets. Doing it this way keeps habits tight, stops impulse drains. Temptation fades when crisis cash stays off-limits for small wants. Sharp savers lean on this method – it clears mental clutter, sharpens choices when things get shaky.

3. Consider Your Job Stability Before Deciding the Amount

What you do for work shapes how much cash you might want nearby. Pay checks that arrive like clockwork tend to ease money worries, so steady jobs sometimes allow smaller cushions. Yet when pay varies – like for freelancers or shop owners – a bigger stash helps handle quiet months. Surprise dips in earnings hit harder without enough set aside, especially if layoffs sweep through a field. Feeling secure matters too, and those facing unpredictable flows often sleep better with extra saved up. Unexpected downturns test budgets fast, making reserves crucial for some more than others. Most people overlook job stability when mapping out their money. A smarter number in your bank ties directly to how pay actually comes in, not what some tip online says it should be.

4. Account for Family Responsibilities and Lifestyle Needs

One moment everything feels manageable, next it shifts entirely when life adds more weight. Living solo without ties often means fewer bills each month – a lean safety net might cover it. But throw kids into the mix, aging parents, a house payment, tuition, doctor visits, or a partner who relies on your income – suddenly that small cushion vanishes under pressure. When health surprises hit, money gaps turn stressful fast if cash isn’t ready. What you’re used to spending shapes the game too – bigger outgoings ask for deeper backup, quietly but firmly. How much you set aside grows not just from duty, but rhythm of daily choices. When you’re helping relatives or juggling several money commitments, keeping more cash on hand just makes sense. Savings plans work better when they match actual life, not what influencers pretend is normal.

5. Avoid Keeping Excessive Idle Cash

Some think stuffing a savings account equals smart money moves, yet sitting on big balances might erode worth slowly. Inflation marches ahead faster than most bank interest, so buying strength fades each year. Picture prices rising 6 percent annually while your balance grows just 3 – even with gains, loss hides underneath. That extra stash, once bills and crises are covered, tends to do better in options like bonds, FDs, SIP plans, debt funds, or retirement picks based on how much uncertainty feels bearable. Calm comes from knowing cash sits there, true, still years of progress could shrink without notice. People trying to create balance between liquidity and returns often combine savings with low-risk debt fund strategies for better cash efficiency.

6. Use a Salary-Based Savings Formula

Picture this: figure out what you spend each month on must-haves – things like housing, food, power bills, travel costs, coverage plans, loan repayments. Take that sum and stretch it across how many months of backup you aim to hold. Say ₹50,000 leaves your account every month, aiming for half a year’s cover lands at ₹3 lakh saved up. Toss in near-future cash goals next – trips, yearly policy dues, new devices, tuition, health visits scheduled ahead. That total? Your target balance taking shape. Aiming for balance, this method sets clear money goals rather than guessing each month. Because it adjusts to real needs, too much or too little saved becomes less likely.

7. Adjust Savings According to Your Age and Life Stage

Later years bring shifting money demands as duties shift. Twenties mean shaping saving habits, setting aside cash for surprises, beginning small investments. Marriage kicks in during third decade, buying homes begins, kids’ future costs take shape – so more ready cash matters. Middle aged adults face rising health uncertainties, preparing life after work gains weight, protecting what’s been built grows central. Priorities transform quietly, shaped by stage of life, not sudden choices. Later years mean less room for error with money, since setbacks take longer to fix when you are older. That changes how much needs sitting in savings – a number that shifts slowly, not one that stays the same forever. Long-term financial planning becomes more effective when aligned with investment strategies based on age and goals for different life stages.

8. Build a Multi-Layer Financial System

Most careful savers spread cash around instead of stacking it all together. They set up different buckets, each doing its own job – some ready for spending, others locked away just in case. Day-to-day buys come out of one pile; bills get paid from there too. When surprises hit, another section stands guard without touching the rest. Long-range plans live apart entirely, growing slowly over time. Down the line, saving for what’s ahead – say a trip, new tech, or tuition – gets easier with a dedicated pot of funds. Later on, putting money aside for distant milestones builds lasting value over time. With cash sorted into separate buckets, choices feel clearer when surprise costs pop up. Instead of guessing, you see exactly what can be spent and what should grow. When life feels shaky, knowing where things stand makes sticking to a plan far more doable.

Signs Your Savings Account Balance Is Too Low

When pay runs out early each month, trouble might already be brewing behind the scenes. Failure of automatic payments happens often when funds are stretched too thin. Borrowing cash just to cover minor setbacks hints at deeper imbalance in ready money. Relying on plastic for groceries or rent signals risk building up quietly. Surprise costs spark worry more easily if there is no backup stash nearby. Repairs, doctor visits, sudden travel, or work pauses become chaos without breathing room. Each stumble feels heavier when every dollar has already been counted twice. Worries about cash can grow when the numbers in your account stay low. When income comes in but stress stays high, something might be off with how much you’re setting aside.

Signs You May Be Keeping Too Much Money in Savings

When savings run too low, trouble might follow, yet piles of unused cash aren’t safe either. Left sitting for ages in a bank, that money could slowly shrink in real value thanks to rising prices. Fear of investment sometimes keeps folks from growing their future pot, even when they mean well. Sitting on big sums might mean passing up smarter moves like regular plans, pension tools, debt funds, or steady earners. Earning next to nothing while bringing in plenty each month? That’s another clue things are off track. Comfort comes from stashing cash, yet big balances might limit what grows later. Aim shifts when peace of mind trades places with smart moves across accounts. Balance shapes better outcomes than totals ever could.

Common Mistakes People Make

- Treating Savings as Investment: Savings accounts offer liquidity and security, but they are not intended for long-term wealth growth because the rates are typically lower than inflation.

- Ignoring Inflation: Many consumers focus solely on the nominal account balance, disregarding how inflation quietly diminishes real purchasing power year after year.

- Having No Emergency Reserve: Even minor financial setbacks might push people into costly debt or credit dependence if they do not have emergency funds.

- Mixing Investment and Expense Money: Using one account for everything leads to confusion, poor spending control, and ineffective financial tracking.

- Blindly Copying Others: Instead of following generic online advice, evaluate your responsibilities, lifestyle, and income pattern when choosing your appropriate savings account balance.

The long-term impact of inflation becomes easier to understand through real examples of shrinking purchasing power in changing economic conditions.

Real-Life Examples

Example 1: Salaried Professional- Every month Rohit brings home about eighty thousand rupees working at a private firm. His first move used to be stuffing nearly every penny into a savings account, thinking fat balances equalled peace of mind. But once he sat down to track what he truly spent each month, things shifted quietly. It turned out, hoarding beyond half a year’s worth of backup cash wasn’t adding real security. These days, he sets aside just enough for emergencies – nothing more. The leftover income flows steadily into SIPs along with safer debt tools instead. Because of better money habits, he felt more secure while also building value over time. When health troubles hit at home, costs were covered easily – plans stayed on track, no borrowing needed.

Example 2: Freelancer with Unstable Income- Some months pay well. Then again, others barely cover rent. Ananya designs graphics on her own terms – that means money comes unevenly. Still, she keeps ten months’ worth tucked away in accounts she can reach fast or bonds that mature soon. When work dried up last winter, those funds kept life steady. No panic. Just quiet breathing through the dip. One way she stays on track is by putting tax cash, backup funds, and daily expenses into separate places. Because everything has its spot, uncertainty doesn’t shake her calm – knowing what’s where makes all the difference.

Example 3: Young Investor Starting Financial Planning- Out of nowhere, Aman began working full time and dove straight into risky investments while skipping basic saving habits. Then – laptop died, doctor bills piled up, all within weeks – and his account came up short when it mattered most. So instead of waiting, he turned to plastic just to cover costs. That moment changed things; slowly but surely, he tucked away enough cash to handle four months’ worth of living costs before touching stocks again. These days, his finances move like layers: some ready to grab, some set to grow. Less worry shows on his face now, simply because he knows what to do if something goes sideways.

Psychological Benefits of Maintaining the Right Savings Balance

Peace of mind shows up when money feels less like a threat. Knowing there’s backup cash means surprises do not spiral into stress. Choices at work become clearer once fear of collapse fades away. When pressure lifts, judgment tends to steady itself. Decisions arrive slower, more thoughtfully, if hunger for quick fixes disappears. Having plenty of accessible cash means you do not rely so heavily on credit cards or costly borrowing – that shift alone eases tension in noticeable ways. When money is ready for surprises, emotions tend to stay steadier, thoughts clearer. Most overlook how deeply this sense of readiness affects mood – until an urgent bill hits without warning. Truth be told, feeling sure about your finances can weigh just as heavy as growing them.

How Inflation Changes Savings Strategy

Money feels different now that prices keep climbing. Safety once made banks the go-to spot for extra dollars. These days, sitting on cash chips away what it can buy. Bills add up faster – food, medicine, school, travel, power – yet bank returns barely rise. What seemed wise a few years back doesn’t stretch nearly as far today. These days, just putting aside cash does not do the job. What matters more is how you mix ready access with steady gains. Some folks pair quick-access funds with regular investment plans, fixed-income options, pension tools, along with varied assets – to keep future buying strength intact. Rising prices have led many to rethink where their money sits, shifting from passive stashes to sharper choices across different pockets of value.

Conclusion

Here’s a thought: your best savings number isn’t some sky-high figure gathering dust. What matters most? A setup that keeps you safe, ready for surprises, open to change, yet still building value over time. Running too lean risks panic when life shifts – car trouble, medical bills, job gaps. On the flip side, letting large sums sit untouched often means losing ground slowly, thanks to rising prices. Think differently – not just stashing funds but routing extra amounts into steady opportunities that compound without constant effort. Money moves in 2026 aren’t just about income – smart handling matters just as much. When savings are mapped out ahead of time, tough moments feel less shaky. Clarity shows up when things get unclear. Decisions come easier because pressure fades. Calm replaces fear when choices need to be made.

FAQs

Q1: How much money should I have in my savings account?

Most financial gurus advocate saving three to six months’ worth of critical costs, depending on your salary and obligations. The actual amount depends on lifestyle, family size, and financial commitments.

Q2: Is having too much money in savings accounts bad?

True, when money sits too long, its value slips since bank rates usually trail rising prices. Instead of letting it pile up, stash past immediate reserves could shift toward thoughtful growth paths.

Q3: Should emergency cash remain entirely in savings accounts?

Emergency funds should be kept easily available, although some people split them between savings accounts and low-risk liquid assets for greater efficiency and somewhat higher returns.

Q4: Does age affect Ideal Savings Account Balance planning?

Yes, savings requirements typically rise as people become older due to increased responsibilities, healthcare bills, and retirement preparation.

Q5: Can I invest all of my spare money instead of keeping it in savings?

Investments are crucial, but withdrawing all liquidity might cause major complications during an emergency. A balanced approach to saves and investing is usually safer.

Q6: Why do financially stable people keep emergency savings?

Even financially secure people confront uncertainties such as medical problems, market crashes, and temporary income disruptions. Emergency liquidity safeguards investments against forced withdrawals during bad times.

Disclaimer

This article serves education and information alone, never standing in for expert money, investing, tax, or law counsel. How much you need to save shifts with pay level, duties, daily choices, targets, and comfort with uncertainty. Each person must look closely at their finances prior to choosing accounts or where to put funds. Turn to a certified finance helper or bank specialist when needing custom help on saving, growing wealth, taxes, or preparing for surprises.