Discover the hidden charges in personal loans that could inflate your borrowing costs. Learn about processing fees, prepayment penalties, and more to make smarter financial decisions. Save money by uncovering these sneaky costs today! #hidden charges in personal loans, #personal loan hidden costs, #hidden fees in personal loans to avoid, #what are hidden charges in personal loans, #personal loan fees explained, #how to spot hidden fees in personal loans, #common hidden charges in personal loans, #avoiding surprise fees in personal loans

Introduction: Uncovering the True Cost of Personal Loans

Many people rely on personal loans for everything from crises to weddings, schooling, or dream holidays. Although they provide fast access to money, the low interest rates they promote may not be true. Personal loans with hidden fees have the potential to subtly increase your borrowing costs and transform an otherwise inexpensive loan into a financial hardship. Even the most astute borrowers may be taken aback by these deceptive costs, which are frequently concealed in fine print. In this comprehensive guide, we’ll reveal 7 shocking hidden charges in personal loans you must avoid and provide actionable tips to borrow wisely. You may safeguard your financial future and save thousands of dollars by being aware of these expenses.

Why Hidden Charges in Personal Loans Matter

The interest rate or monthly EMI is frequently the main focus when you apply for a personal loan. However, hidden charges in personal loans—like processing fees, prepayment penalties, and insurance premiums—can significantly increase the total cost. A Consumer Financial Protection Bureau survey found that many borrowers fail to pay these fees, which results in unanticipated debt. Knowing these expenses up front gives you the ability to evaluate lenders wisely and stay out of debt.

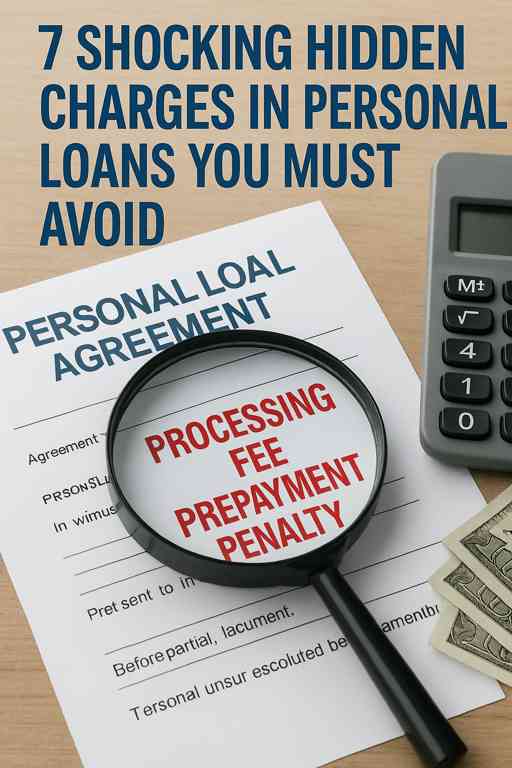

1. Processing Fees: The Silent Deduction

One of the most common hidden charges in personal loans is the processing fee, typically ranging from 1% to 3% of the loan amount. Prior to disbursement, this charge is subtracted from the approved loan. For instance, you will only receive $9,800 if you borrow $10,000 with a 2% processing fee, but you will still be responsible for repaying the entire $10,000 plus interest.

How to Avoid: Always request the processing charge up front and account for it when calculating your loan. Look around for better offers because some lenders might remove this cost during promotional periods. Loan offers can be compared with the use of websites such as Bankrate.

2. Prepayment and Foreclosure Penalties: The Cost of Early Repayment

Although it may seem wise to pay off your loan early in order to save interest costs, many lenders charge prepayment or foreclosure penalties, which can range from 2% to 5% of the remaining debt. Early repayment is less cost-effective because Non-Banking Financial Companies (NBFCs) frequently charge higher fees than banks.

How to Avoid: Seek out lenders that have minimal or no prepayment penalties. Verify the loan agreement’s terms before signing. To balance the advantages of early repayment against penalties, use resources such as the loan comparison calculator on NerdWallet.

3. EMI Bounce and Late Payment Fees: The Penalty for Missed Payments

There are significant EMI bounce costs ($15–$30 per instance) and late payment penalties ($20–$50) associated with missing an EMI or not having enough money for an auto-debit. These hidden charges in personal loans not only increase costs but can also harm your credit score, affecting future borrowing.

How to Avoid: To prevent misses, set up automated payments or reminders. Keep money set aside in your bank account to cover auto-debits. Visit the official website of your lender, such as the fee disclosure page of LendingClub, to review their fee schedule.

4. Insurance Premiums: The Hidden Add-On

Some lenders increase the principle amount of personal loans by including loan protection or personal accident insurance. Your EMI rises as interest is subsequently applied to the inflated principal. Insurance can be helpful, but it’s frequently portrayed as required, which may not be the case.

How to Avoid: Compare quotes for independent insurance and find out if insurance is required. Check for bundled premiums in the loan agreement. Investopedia and other resources provide guidance on assessing loan terms.

5. Goods and Services Tax (GST): The Overlooked Extra

An 18% GST is applied to all personal loan expenses, including processing, prepayment, and late payment fees, raising the overall cost. For example, GST makes a $200 processing fee $236. This tax is rarely highlighted by lenders, making it one of the sneakiest hidden charges in personal loans.

How to Avoid: When calculating the cost of a loan, include GST. To determine the entire cost, including taxes, use online EMI calculators such as the one on Credit Karma.

6. Statement and Documentation Charges: Small but Cumulative

Some lenders charge $5 to $20 each request for loan account statements, duplicate papers, or amortisation schedules. These hidden charges in personal loans can add up if you frequently need paperwork or make changes to your loan terms.

How to Avoid: Choose lenders that provide free online statement access. Prior to signing, review the lender’s documentation fee policy. Clear fee structures are frequently offered by platforms such as SoFi.

7. Interest Rate Manipulation: The Fine Print Trap

Some lenders advertise low interest rates, but instead of lowering balance rates, they impose flat rates, which raises the total amount of interest paid. Others may include hidden charges in personal loans by adjusting rates based on credit scores or loan tenure without clear disclosure.

How to Avoid: Always make sure the rate is decreasing or flat. To determine actual interest costs, use comparison tools on websites such as Forbes Advisor.

How to Spot Hidden Charges in Personal Loans

To avoid being blindsided by hidden charges in personal loans, follow these steps:

- Request a Full Fee Breakdown: Prior to signing, request a comprehensive summary of all charges. This is what reputable lenders will offer.

- Read the fine print: Look for phrases like “processing fee,” “prepayment penalty,” or “insurance premium” in the loan agreement.

- Compare Multiple Lenders: To compare terms and costs from several lenders, use websites such as LendingTree.

- Check Your Credit Score: Interest rates and fees can be decreased with a higher score. Get your score through Experian.

- Ask Questions: Make it clear if insurance is optional or if fees are negotiable. Never be afraid to bargain.

The Financial Impact of Hidden Charges

Ignoring hidden charges in personal loans can have serious consequences. You could pay an additional $560 (including 18% GST) on top of interest for a $10,000 loan that has two missed EMI fees ($30 each), a 3% prepayment penalty, and a 2% processing fee. This might add up to thousands of dollars in extra expenses during a five-year loan. You can steer clear of these pitfalls and save a lot of money by being knowledgeable.

Conclusion: Borrow Smart, Save Big

Hidden charges in personal loans can turn a helpful financial tool into a costly mistake. These hidden expenses, which include GST and processing fees, can raise your loan amount by hundreds or thousands. By understanding the 7 shocking hidden charges in personal loans—prepayment penalties, EMI bounce costs, GST, insurance premiums, processing fees, documentation fees, and interest rate tricks—you may make well-informed borrowing choices. Always compare lenders, study the tiny print, and request a detailed charge breakdown. By using these techniques, you’ll be able to borrow more wisely, stay out of financial surprises, and keep more of your money.

FAQs

Q1: What are the most common hidden charges in personal loans?

Processing fees (1-3%), prepayment penalties (2-5%), EMI bounce fees ($15-30), late payment penalties ($20-50), insurance premiums, GST (18%), and documentation fees are examples of common hidden costs.

Q2: How can I avoid hidden charges in personal loans?

Read the loan agreement carefully, compare lenders, ask for a complete price breakdown, and find out if fees like insurance are optional. Make use of comparative sites such as Bankrate.

Q3: Are there any unstated fees associated with personal loans?

Although they vary in transparency, most personal loans carry some costs. While some lenders may hide costs in fine language, reputable lenders reveal them up front. Always seek clarification.

Q4: Can my credit score be impacted by concealed charges?

Yes, your credit score can be lowered by missing EMIs or paying bounce costs. To avoid fines, make your payments on time and keep money in your bank account.

Q5: Are there any personal loans that don’t have any additional fees?

Clear loans with low fees are provided by certain lenders. Search for “no-fee” or “low-fee” loans on websites such as LendingClub or SoFi.

Disclaimer

This article is not financial advice; rather, it is merely informational. A competent financial advisor should always be consulted before taking out a loan. Verify specifics with your provider as loan conditions and fees may depending on the lender. Any monetary losses resulting from choices made in response to this article are not the author’s responsibility.

Also Read: