Navigate your home loan decision guide with confidence! Explore 7 key factors, pros, cons, and expert tips to decide if a home loan is right for you in 2025. Make informed financial choices now! #home loan decision guide, #should I take a home loan, #things to consider before taking a home loan, #is a home loan worth it, #pros and cons of home loan, #what to know before getting a home loan, #factors to consider for a home loan, #home loan in 2025

Introduction: Unlock Your Path to Homeownership with a Home Loan Decision Guide

A crucial decision that could impact your financial destiny for decades is whether or not to take out a home loan. Making the best decision in 2025 will demand preparation and clarity due to rising real estate prices and changing interest rates. Your go-to resource for confidently navigating this difficult decision is this home loan decision guide. This guide presents seven important aspects to consider when weighing your alternatives, whether you’re a first-time buyer or reevaluating your options. These criteria balance the benefits of homeownership against the obligations of a loan. This home loan decision guide will provide you the knowledge you need to make an informed decision that fits your budget.

1. Discover the Wealth-Building Power of a Home Loan

A home loan decision guide starts with understanding the financial upside. Your monthly Equated Monthly Installment (EMI) is converted into equity in a physical asset with a home loan, as opposed to renting, where payments have no lasting value. Urban real estate frequently increases in value over time, making it an alluring long-term investment. For instance, traditionally, real estate in expanding cities has surpassed inflation, increasing homeowners’ wealth.

A home loan decision guide also identifies important tax advantages. Under Section 80C of the Income Tax Act, you can deduct up to ₹1.5 lakh per year from principle repayments, and under Section 24(b), you can deduct up to ₹2 lakh from interest payments. By reducing your taxable income, these deductions increase the affordability of a house loan.

Key Takeaway: This house loan choice guide demonstrates how, although you must weigh these advantages against long-term expenses, a home loan can increase wealth through asset ownership and tax savings.

2. Embrace the Long-Term Commitment

A home loan decision guide emphasizes that a home loan is a 15- to 30-year commitment requiring steadfast financial discipline. By lowering your credit score, missing EMIs can restrict your ability to borrow money in the future. Regular EMI payments are essential for a solid credit record, according to CIBIL. A home loan decision guide suggests that in order to manage this long-term commitment, you should make sure you have a steady income and an emergency fund that can cover six to twelve months’ spending.

Particularly in unpredictable economic times, fixed monthly EMIs might also limit money for other objectives, such as investments or vacation. To prevent going over your financial limit, this house loan choice guide advises evaluating your budget.

Key Takeaway: A home loan decision guide prepares you for a decades-long commitment, ensuring your income and savings can handle EMIs.

3. Evaluate Your Financial Readiness

Your financial health is the foundation of a sound home loan decision guide. Your debt-to-income ratio, income stability, and credit score are all factors that lenders consider. Reliability is shown by a credit score above 750 (out of 900), which leads to better lending rates. Savings are also required for a down payment (10–20% of the property’s worth) and a contingency fund for unforeseen expenses.

Your budget may be strained by a home loan if you’re also paying other EMIs. Make sure your EMIs don’t surpass 40% of your salary by using a home loan EMI calculator. This home loan decision guide advises delaying making a commitment until your finances are stable.

Key Takeaway: A home loan decision guide stresses a strong credit score, stable income, and ample savings for a stress-free loan experience.

4. Choose the Right Property Location

A critical aspect of this home loan decision guide is the property’s location. A house in a growing neighbourhood with strong schools, hospitals, and internet access has a better chance of appreciating in value. There is frequently high demand for and resale value for properties close to tech hubs or metro lines. On the other hand, purchasing at a period of market stagnation or overhype may trap your money.

Use websites such as Housing.com or 99acres to investigate regional trends. Prioritising areas with growth potential is advised by this home loan decision guide in order to optimise your investment.

Key Takeaway: For long-term financial rewards, choosing a property in a high-potential neighbourhood is advised by a home loan decision guide.

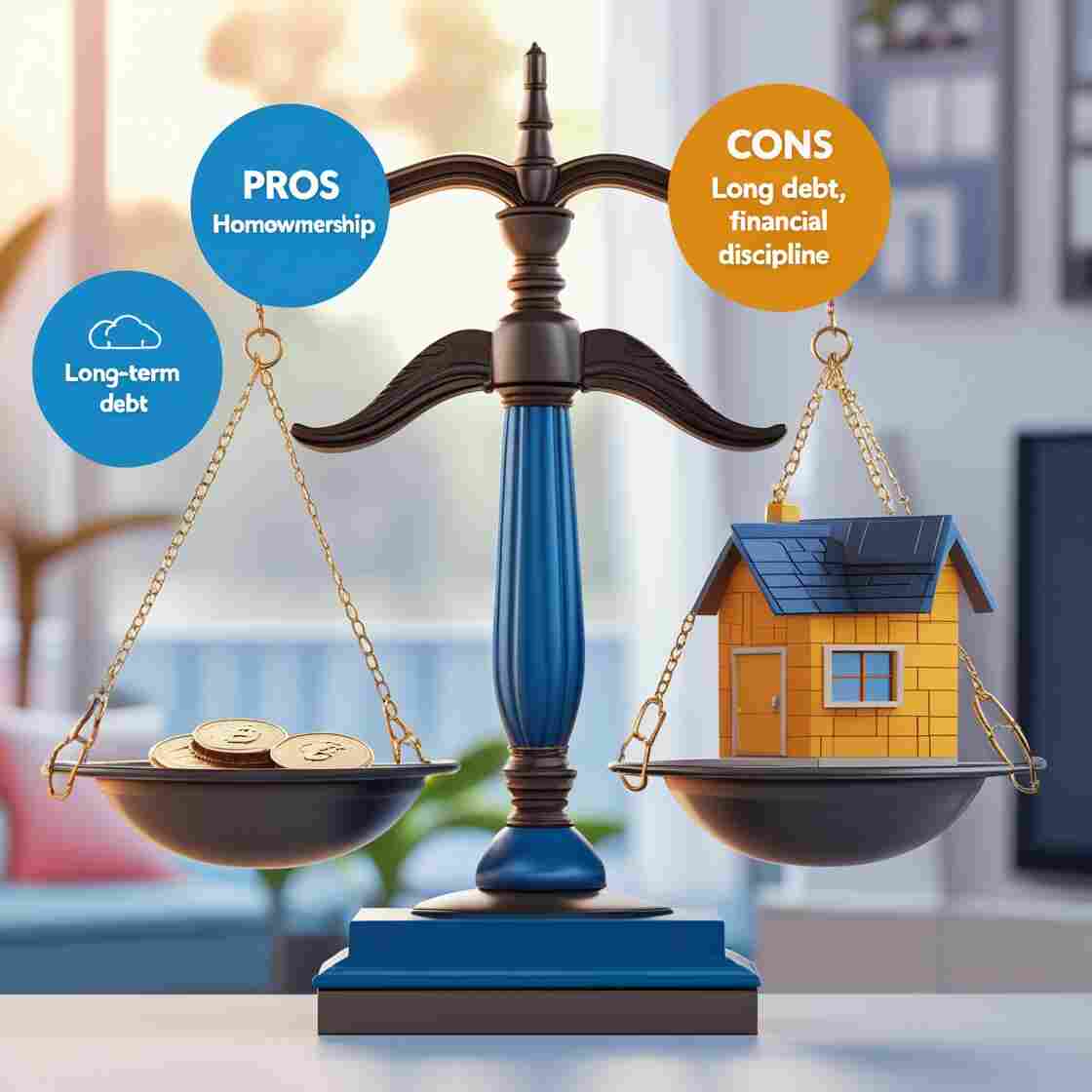

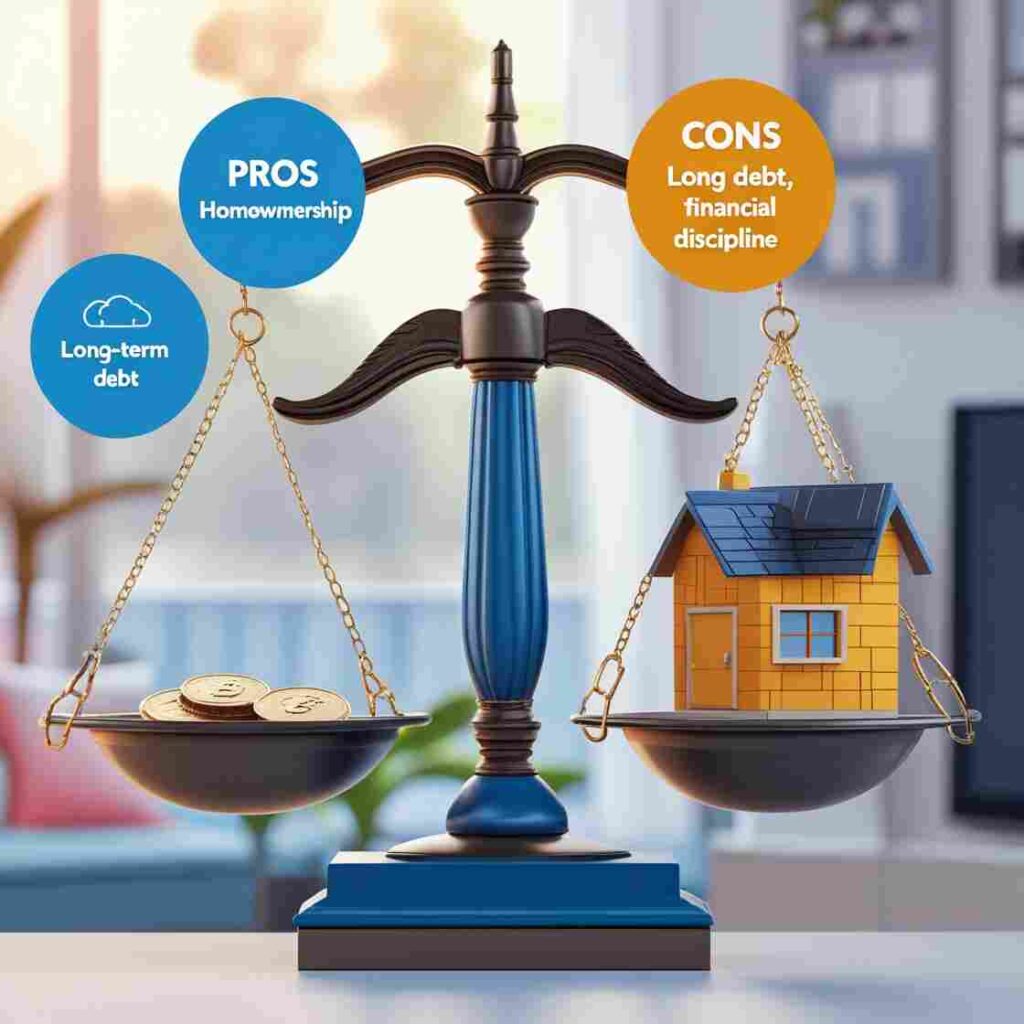

5. Balance the Pros and Cons of a Home Loan

A comprehensive home loan decision guide must weigh benefits against drawbacks. Here’s a clear breakdown:

Pros

- Asset Creation: Invest in real estate that might increase in value over time.

- Tax Savings: Your tax burden is lessened by principle and interest deductions.

- Stability: Having a home provides security and removes rent increases.

- Prepayment Options: To reduce interest expenses, the majority of lenders permit prepayments without penalties.

Cons

- Long-Term Debt: A commitment spanning 15 to 30 years may seem excessive.

- Financial Strain: EMIs may make it harder to save money for other objectives.

- Market Risks: Low returns could result from bad site selections.

- Impact on Credit: Your credit score may suffer if you miss payments.

Key Takeaway: This home loan decision guide shows that home loans offer wealth-building potential but require careful risk management.

6. Renting vs. Buying: What’s Right for You?

This home loan choice guide includes the rent-or-buy conundrum as a major element. If you’re not sure if you want to live in one place for the long run, renting gives you flexibility. Funds are released, but no equity is created. Purchasing gives you stability and an asset, but it also binds you to a place and a loan.

A home loan frequently beats renting if you can pay the EMIs and want to remain in the city for seven or more years. To compare costs, use a rent vs. buy calculator. You can better match your selection with your life objectives by using this home loan decision guide.

Key Takeaway: A home loan decision guide advises renting for people who value flexibility and purchasing for long-term residents.

7. Navigate 2025 Market Conditions

This house loan decision guide takes into account the particular market conditions of 2025. While floating-rate loans can profit from future rate reductions, rising interest rates might favour fixed-rate loans to lock in expenses. Use resources such as the Economic Times or the Reserve Bank of India to stay updated. This home loan choice guide highlights the wisdom of timing your loan according to market movements.

Key Takeaway: To select the best loan type and timing, a home loan choice guide recommends keeping an eye on 2025 trends.

Conclusion: Your Home Loan Decision Guide to Financial Success

With the help of this house loan decision guide, you may approach homeownership with confidence and clarity. You can choose wisely by examining seven important aspects: financial advantages, long-term commitment, financial preparedness, property location, advantages and disadvantages, renting versus purchasing, and market conditions in 2025. Although a home loan requires discipline and careful planning, it provides stability, tax savings, and possibilities to create wealth. Make sure your choice is in line with your objectives by using this home loan decision guide to evaluate your finances and investigate properties. Let this book serve as your reliable companion in 2025 for a more prudent and secure financial future.

FAQs

Q1: Can I save money by paying off my house loan early?

According to this home loan decision guide, the majority of lenders do permit penalty-free prepayments for floating-rate loans, which lower interest and shorten loan terms.

Q2: How is my credit score impacted by a home loan?

According to this house loan decision advice, a home loan may initially lower your score because to enquiries and debt, but on-time EMI payments raise it.

Q3: Is a home loan preferable than renting?

While buying increases equity, renting allows for flexibility. Long-term residents with stable finances are advised to purchase a home by this home loan decision guide.

Q4: What should I look for at the location of a property?

As suggested by this house loan decision guide, pay attention to resale potential, infrastructure, and connectivity.

Q5: Do home loans qualify for tax deductions?

According to this home loan choice guidance, you may deduct up to ₹1.5 lakh on principal (Section 80C) and ₹2 lakh on interest (Section 24b) per year.

Disclaimer

Financial advice is not provided by this home loan decision guide; it is merely meant to be informative. Before choosing a house loan, speak with a lender or qualified financial expert to assess your unique situation. There are dangers associated with real estate loans and investments, and market conditions can change. Consult a tax expert to confirm tax benefits.

Also Read:

- How to Invest in Real Estate in India 2025

- Second Home Investment Tips: 5 Critical Factors to Know Before Buying

- 7 Essential Insights on What Does Home Insurance Cover to Protect Your Home

- Should you take a home loan? What to weigh before deciding

- Understanding Home Loans in India: A Complete Guide

- Step-by-step home loan process in India: A complete guide