Understand How DA (Dearness Allowance) is Calculated under the 7th Pay Commission using CPI formula, real examples, pension impact and revision framework. How DA (Dearness Allowance) is Calculated, DA calculation formula, 7th Pay Commission DA formula, AICPI index DA, DA percentage calculation, DA impact on pension, DA revision January July, CPI based DA calculation.

Update (March 2026): This article has been reviewed and updated to reflect the current framework of How DA (Dearness Allowance) is Calculated under the 7th Pay Commission using the latest CPI methodology.

Introduction

Quietly, inflation chips away at how far money can go. Slowly, a paycheck that used to handle bills starts falling short. Because of this shift, workers and retirees in public service gained protection through a measure called Dearness Allowance. Its purpose took root not with fanfare, but necessity. However, while most employees track DA hike announcements closely, very few clearly understand How DA (Dearness Allowance) is Calculated under the 7th Pay Commission framework.

Money loses strength over time without much notice. Bills grow harder to cover even when pay stays the same. So public employees and those who stopped working got help in the form of something named Dearness Allowance. Not born from ceremony, it came because life became heavier. Needed before anyone declared it essential.

The Purpose and Structure of Dearness Allowance

One reason DA sticks around? To fight rising costs. Prices go up, pay buys less – unless something makes up the difference. That gap gets covered because of how DA works. Workers see it added straight onto their base salary. Retirees get a similar boost tied to pension amounts. Over time, this part helps keep spending strength steady. Remember this: DA uses only part of your pay, not the full amount. HRA, transport money, plus certain extra payments do not count toward it. The calculation leaves out these parts by design.

Yearly raises tie to how long someone has worked. Because of price changes, though, DA adjusts without regard to job status. People drawing pensions get these updates too. After all, they no longer move up a ladder at work. Still, rising costs affect them just the same.

The Inflation Backbone: AICPI Explained

Figuring out how dearness allowance works begins with a number called the All India Consumer Price Index for Industrial Workers. Prices shifting month to month for everyday items sit at the core of this measurement. Across cities and factories, what people buy – like meals, rent, clothes, kerosene – gets tracked closely. What shows up in those records shapes adjustments tied to living costs. Even small shifts in fuel prices ripple through the total count. Essentials make up most of the list, quietly guiding the math behind pay supplements.

Month after month, the Labour Bureau – part of the Ministry of Labour and Employment – releases these numbers. Rather than jumping at sudden changes, officials rely on a rolling twelve-month blend of AICPI readings. That steady measure tames wild shifts, keeping pay adjustments stable even when prices briefly jump. By spreading inputs across a full year, brief market ripples lose their power to distort decisions.

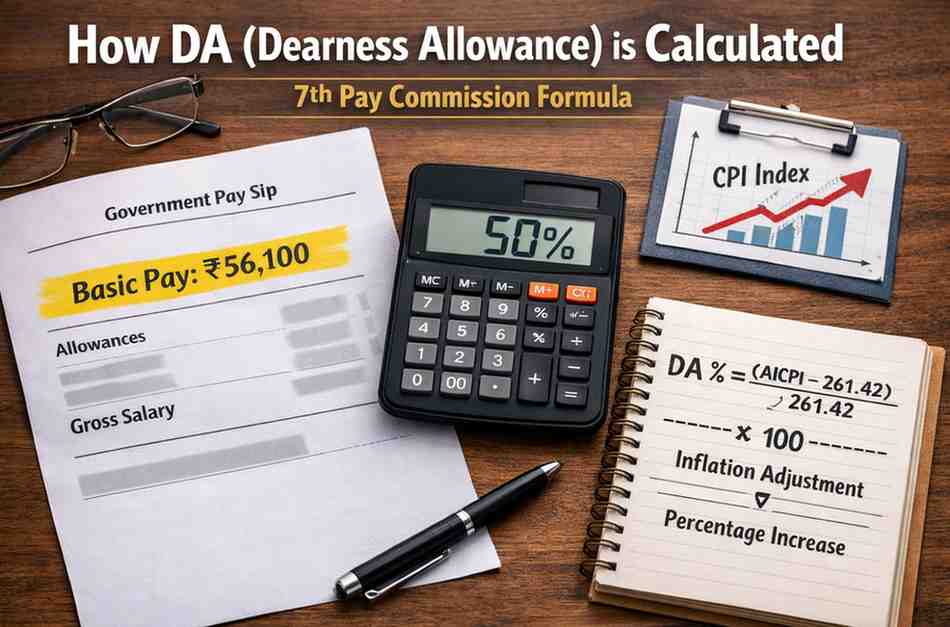

Step-by-Step Breakdown of How DA (Dearness Allowance) is Calculated

Under the 7th Pay Commission, the calculation of Dearness Allowance follows a structured mathematical formula linked to inflation data. The formula is:

DA % = ((12-month average of AICPI – 261.42) ÷ 261.42) × 100

Let us now break this into clearly defined steps.

Step 1: Collect the Latest 12 Months of AICPI Data

Starting off, find the latest 12-month stretch of AICPI figures – that’s the All India Consumer Price Index for Industrial Workers. Put out each month by the Labour Bureau, this info forms the base.

A different way begins how the numbers are figured each year. Rather than pick one month’s inflation value, twelve months get folded together into a rolling total. Spikes in grocery or gas prices lose their sharp edge when smoothed like this. By spreading changes across time, pay adjustments stay steady through sudden jumps.

Step 2: Calculate the 12-Month Average CPI

Picture those twelve monthly CPI numbers gathered up. Their mean comes together at 392.00 when averaged.

This figure captures how prices have shifted during twelve months straight. What you see comes from steady increases tied to everyday items people rely on.

Yearly averages smooth things out, so changes in DA follow lasting price shifts instead of brief spikes.

Step 3: Subtract the Base Index (261.42)

One way to look at it: 261.42 marks where things started under the 7th Pay Commission. That figure became the reference point for prices when changes took effect.

Start by taking the 12-month average of the CPI. From that number, remove the starting index value. What remains shows how much prices have risen overall. This method tracks total inflation steadily over time.

Example:

392.00 – 261.42 = 130.58

This difference shows how much the price index has risen compared to the base year.

Step 4: Divide by the Base Index

The difference obtained in Step 3 must be standardised. This is done by dividing it by the base index (261.42).

130.58 ÷ 261.42 = 0.4995

This step converts the inflation difference into a proportional figure relative to the base index. Without this step, the increase would not be expressed as a percentage.

Step 5: Convert the Value into Percentage

The proportional figure is multiplied by 100 to convert it into percentage form.

0.4995 × 100 = 49.95%

The final value is rounded according to official rules. In this example, the DA rate would be notified as 50%.

Step 6: Apply the DA Percentage to Basic Pay

Once the percentage is officially announced, it is applied to Basic Pay (for employees) or Basic Pension (for retirees).

If Basic Pay = ₹56,100 and DA = 50%:

56,100 × 50% = ₹28,050

What you get here forms part of your monthly pay labelled DA. Once that rate is set, things move smoothly, yet the method ties the number directly to real-world price changes. It stays grounded in actual figures

Why DA Is Revised Twice a Year

Every January and July brings updates to DA, keeping pace without chaos. Too many changes – say, every month – and things get messy fast on payrolls. Yet waiting a full year risks letting inflation eat into earnings slowly. Stability matters, but so does staying current.

Half a year gives enough time to collect CPI numbers, yet keeps inflation updates moving without long waits. Starting in January, changes rely on data gathered since the prior July through June, whereas those in July pull from January to December instead. When delays happen in announcing adjustments, payments still go back to when they should have started.

A clear method keeps DA changes from being too sudden or arriving late.

What Happens When DA Crosses 50%?

Halfway past fifty means something – not just in name but in effect. Before, when pay panels decided, hitting that mark usually pulled DA into Base Pay like clockwork. Now things differ; the 7th CPC does not lock it in by default. Only a clear signal from authorities can make it happen this time around.

Even so, going past 50% might stir shifts in money flows. As DA hits specific marks, HRA bands tend to shift higher. Once those points are reached, updates often follow. Transport pay could see tweaks at similar junctures. When DA climbs, NPS inputs grow too – tied as they are to Basic Pay along with DA. These boosts happen without extra steps.

So when DA goes up, it doesn’t blend straight into base pay but still shakes things up elsewhere in the paycheck.

Impact on Pensioners

Older adults rely on DA because it fights rising prices. Without pay hikes from job growth, these updates matter a lot. Living costs creep up – DA helps keep pace. Promotions stop after retirement, yet expenses grow; that is where this support steps in.

A retiree getting ₹30,000 as base pay sees their DA hit ₹15,000 when it’s set at half that amount – total income then lands at forty-five thousand rupees. When that same DA climbs four points higher, up to 54 percent, the pay-out shifts upward – to ₹46,200. Stretching across years without work, tiny bumps like these reshape budget margins more than expected. Medical costs rising over time make those slight gains matter far beyond surface numbers. For retirees, consistent income adjustment becomes essential when managing long-term longevity risk in India.

Real-Life Examples

Example 1: Mid-Career Officer

That extra four percent made Anita pause. Her pay stub now showed a hike – fifty per cent dearness allowance instead of forty-six. A jump of two thousand one hundred twenty-four rupees each month didn’t feel life-changing at first glance. But multiplied across twelve months? More than twenty-five thousand saved before she even noticed. She chose to funnel that sum into steady investment plans. Comfort crept up slowly – no splurges, just silent growth year after year. Small shifts, repeated, began reshaping what security meant by the fifth cycle. Numbers stacked without fanfare.

Example 2: Retired School Principal

After working many years, Mr. Verma began receiving ₹42,000 each month as basic pension. Because prices kept going up, changes in dearness allowance made it easier to handle medical bills and power costs. Once dearness allowance went beyond half the base amount, his total payment jumped quite high. Still, prices kept rising a bit, yet buying strength stayed mostly steady. Had there been no DA updates, his actual earnings would’ve dropped noticeably.

Example 3: Young Government Recruit

Fresh off joining the public sector, Rahul saw each new dearness allowance not as extra cash but a cue to act. When the amount ticked up, his response stayed consistent – shift that rise straight into future-focused savings. Rather than let it blend into daily expenses, he treated the boost like fuel for bigger goals. Every uptick became part of a quiet habit, building value without fanfare. Many employees channel incremental DA into structured allocation using a three-bucket portfolio strategy.

Over time, Rahul realised that periodic DA increases, though small individually, created compounding momentum when invested consistently.

Tax Implications of DA

Tax on Dearness Allowance works just like any other salary income under the law. Some workers think it might be taxed differently because it adjusts for rising prices. Yet the truth is, it gets added straight into their usual pay for tax purposes. What feels like extra due to inflation still counts fully as earnings.

With a rise in DA, yearly earnings go up by the same amount. That could shift some workers nearer to the edge of a bigger tax slab. Or it might shrink the space left before hitting rebate limits. For those sticking to the earlier tax system, benefits tied to pay components can change too.

An increase in DA may also require recalculating tax projections for the financial year. Higher DA can change taxable income slabs, especially when computing advance tax liability.

People who earn extra money – maybe from rent, interest, or selling assets – need to pay close attention here. When dearness allowance goes up, it can push overall income higher without warning. That surprise boost might mean taxes get miscalculated. Falling short on tax payments triggers charges, specifically under rules 234B and 234C. Missing those marks costs more in the long run.

Got pension? That dearness allowance tagged onto it counts as taxable income. Even if part of your pension gets a tax break when taken early, the DA portion still falls under salary earnings for taxes. Not everything tied to retirement pay escapes the tax net.

Therefore, whenever a DA hike is announced, employees should:

Recalculate projected annual income

Review TDS deductions

Adjust advance tax payments if applicable

Update financial planning allocations

Getting taxes right means inflation adjustments won’t lead to trouble with tax rules by accident.

Conclusion

Understanding How DA (Dearness Allowance) is Calculated eliminates uncertainty around salary revisions. What keeps DA tied to rising prices lies in the 7th Pay Commission’s setup – clear, open, built to be counted on. Following CPI shifts and sticking to set rules lets staff and retirees guess adjustments without waiting for updates. More than just a pay bump, this allowance acts like armor against inflation within public sector wages. Understanding its mechanics opens doors to smarter budgeting, clearer tax guesses, future income views shaped by reality.

FAQs

Q1: Is DA calculated on gross salary?

Here’s how it works – DA uses just the Basic Pay if you’re still working, or Basic Pension once retired. Things like HRA or transport money? Left out completely. Special benefits also don’t make the cut. The number crunching sticks only to that central part of your earnings. Whatever rate applies, it gets slapped onto this one piece alone.

Q2: Why is 261.42 used in the DA formula?

The base Consumer Price Index used during the 7th Pay Commission is shown in figure 261.42. It serves as the standard by which cumulative inflation is evaluated. The DA % is calculated using inflation growth, which is reflected in any increase over this index.

Q3: Is Dearness Allowance fully taxable?

According to the Income Tax Act, DA is completely taxable as a component of salary income. In order to determine total taxable income, it is added to gross salary. Along with their pension, pensioners also pay taxes on the DA they receive.

Q4: Does DA automatically merge with Basic Pay after crossing 50%?

Automatic merger is not assured under the 7th Pay Commission. The government must formally announce any decision to combine DA with Basic Pay. While there won’t be an automatic merger, over 50% may result in additional allowance modifications.

Q5: How can employees estimate upcoming DA hikes before official announcement?

One way workers stay informed is checking the Labour Bureau’s monthly AICPI updates. After gathering those numbers, a rolling average across twelve months gets calculated. Using that result, the 7th CPC method helps shape an expected DA figure. Small differences might pop up in informal guesses, yet the core calculation never shifts.

Disclaimer

This piece serves education and awareness goals alone. Though attempts were made to keep details correct, DA rates and rules can shift via state announcements. Check current numbers using authorized releases prior to handling money matters. Updates come often, so relying solely on this text isn’t wise. Guidance here does not count as financial, legal, or tax counsel.