Learn how to calculate advance tax with 7 powerful steps, penalty illustrations, due dates, and real-life examples to avoid costly interest under Sections 234B and 234C. How to Calculate Advance Tax, advance tax calculation example, section 234B interest, section 234C penalty

advance tax due dates, income tax advance tax rules India.

Updated February 2026: This article includes detailed computation of advance tax, practical penalty illustrations under Sections 234B and 234C, behavioural risk analysis, and compliance context relevant for diversified income earners.

Introduction: Why Advance Tax Discipline Matters More Than Ever

Understanding how to calculate advance tax is not merely about meeting statutory obligations; it is about maintaining financial stability throughout the year. Paying taxes ahead of time means splitting the bill into parts, not saving it all for later. When what you owe goes beyond ten thousand rupees minus TDS, this method kicks in. More people now trade stocks, work independently, collect rent, or earn interest – often unaware they’ve crossed the line. Missing this doesn’t bring harsh fines, yet small interest amounts start building up slowly through rules named 234B and 234C. These grow without warning, applied by system logic alone, never adjusted for personal hardship.

Who Must Pay Advance Tax?

Advance tax becomes mandatory when total tax liability exceeds ₹10,000 in a financial year. This typically affects business owners, consultants, freelancers, traders, rental income earners, and investors booking capital gains. Even salaried employees can fall within its scope if they realise gains from shares or mutual funds without properly reviewing their capital gains tax calculation in India. Older adults who don’t run businesses don’t pay this tax, yet nearly everyone else with multiple earnings streams needs close attention to what they owe. What sets off the requirement isn’t where money comes from, but how much is expected overall. Because of that, organized forecasting becomes essential just to stay within rules.

2026 Context: Why Advance Tax Has Become a Broader Risk Area

Lately, people are jumping into retail investing, gig work, and online service gigs like never before. One regular employee might pull money from consulting on weekends, dividends stacking up monthly, quick trades here and there, rent checks rolling in, along with steady bank interest. When so many streams flow together, calculating taxes shifts – no longer a one-time guess but something that moves and changes. Systems tracking these numbers? They’re sharper now. Thanks to tools like AIS and tighter data links between sources, slipping under the radar gets harder each year. Now even those earning average incomes must pay attention – tax rules once meant only for big companies now touch freelancers and consultants alike. Planning every three months shifts from a choice into something necessary.

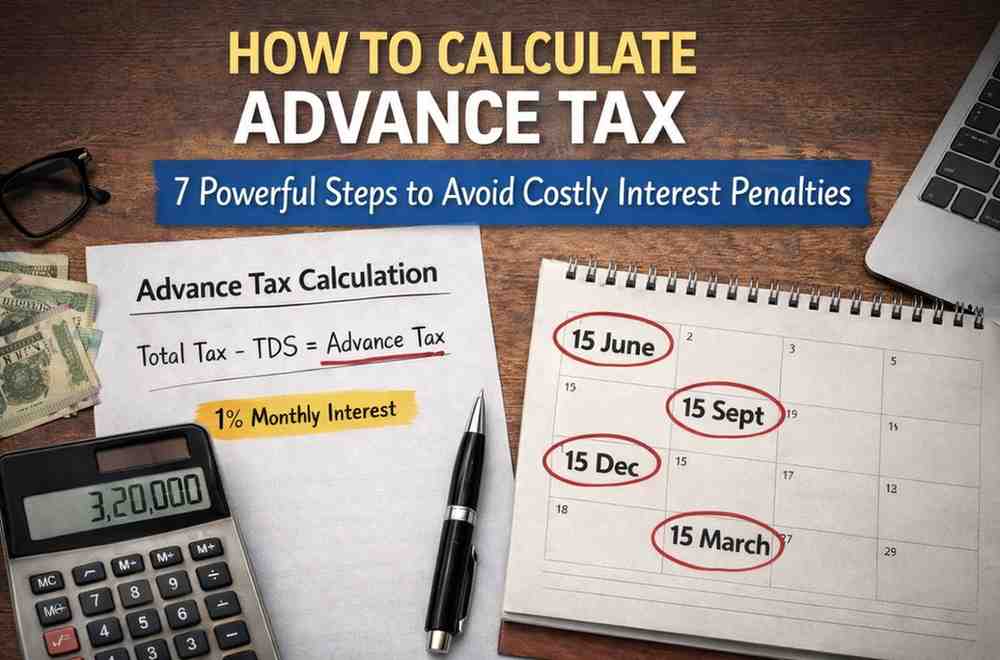

How to Calculate Advance Tax: 7 Powerful Steps Explained in Detail

Step 1: Estimate Total Annual Income

The first step in understanding how to calculate advance tax is to realistically estimate total gross income for the financial year. Pay covers wages, work profits, shop revenue, property payments, asset growth, bank returns – plus whatever else counts. Lots of people overlook the slow build of interest from savings pots, fixed plans, or tiny investment tools, especially when they do not track consolidated returns from various schemes such as post office saving schemes.

Step 2: Deduct Eligible Exemptions and Deductions

Once you figure out total earnings, take away allowed write-offs – things like money put into approved funds under rule 80C, medical plan costs counted in 80D, pension fund deposits, along with breaks such as housing rent allowance or flat reduction. Care matters here since people tend to guess too high on savings they mean to make. Suppose those expected cuts never happen by March; then what gets taxed grows larger, causing gaps in early payments owed. Getting deductions right helps shape a solid number before applying rate levels. Staying careful now avoids bigger errors piling up later.

Step 3: Apply Slab Rates and Add Cess

After figuring out taxable income, use the rate brackets that match your selected system. Where relevant, tack on a surcharge, then throw in an extra 4% for Health and Education Cess. What you’re left with? The full amount of tax owed before credits. Special kinds of earnings – like profits from selling assets – need their own math since taxes there follow separate rules. These portions often slip through cracks, especially when stock prices surge. Overconfidence in projected profits resembles the behavioural tendencies of the risks of chasing high-performing funds, where optimism replaces structured financial planning.

New Tax Regime Slabs

- Up to ₹3,00,000 – Nil

- ₹3,00,001 to ₹6,00,000 – 5%

- ₹6,00,001 to ₹9,00,000 – 10%

- ₹9,00,001 to ₹12,00,000 – 15%

- ₹12,00,001 to ₹15,00,000 – 20%

- Above ₹15,00,000 – 30%

Old Tax Regime Slabs

- Up to ₹2,50,000 – Nil

- ₹2,50,001 to ₹5,00,000 – 5%

- ₹5,00,001 to ₹10,00,000 – 20%

- Above ₹10,00,000 – 30%

Plus:

- 4% Health & Education Cess

- Surcharge where applicable

Step 4: Subtract TDS and TCS Credits

Start by removing taxes taken out before you got paid. Because salary deductions, bank withholdings, plus TCS amounts count toward what you owe. What remains once those are factored in equals how much more tax needs paying now. Workers sometimes think their company’s tax cut covers extra earnings right away. Yet changes made halfway through the year might not reflect immediately. Matching records closely keeps future payments on track without surprise gaps showing up later.

Step 5: Allocate Instalments as per Schedule

Advance tax must be paid in four instalments during the financial year. The statutory schedule requires payment of 15% by 15 June, 45% cumulative by 15 September, 75% cumulative by 15 December, and 100% by 15 March. These percentages apply to total estimated tax liability, not incremental quarterly income. Even if income increases mid-year, the cumulative percentage requirement must be met. Understanding this cumulative structure is crucial to avoiding interest under Section 234C.

Step 6: Revise Estimates When Income Changes

Fresh numbers keep moving past midyear marks. When pay jumps happen – raises, extra checks, property profits, lease shifts – quarterly payments get adjusted later on. Rules allow updates yet ignore past gaps unless fixed by hand. Taxpayers who fail to reassess income sometimes rely on short-term borrowing to manage sudden liability, without fully understanding how credit score works in India, thereby compounding financial stress. Regular reassessment ensures smooth compliance.

Step 7: Monitor 90% Rule to Avoid Section 234B

Beyond quarterly instalments, taxpayers must ensure that at least 90% of total tax liability is paid by 31 March. If less than 90% is paid, interest under Section 234B applies from 1 April until full payment. The official computation rules are detailed by the Income Tax Department on the e-filing portal. This provision is independent of Section 234C. Therefore, even if quarterly instalments were partially compliant, failing to cross the 90% threshold invites additional interest. This final review is essential before financial year closure.

Detailed Penalty Computation Example

Assume the following scenario:

- Total estimated tax liability: ₹3,20,000

- Salary TDS already deducted: ₹1,40,000

- Net advance tax payable: ₹1,80,000

Instalment Requirement (Cumulative)

- By 15 September → 45% of ₹3,20,000 = ₹1,44,000

- Actual tax paid by September → ₹70,000

- Shortfall → ₹74,000

Section 234C Interest

- Interest rate: 1% per month

- Period: 3 months (Sept–Dec)

- Calculation: ₹74,000 × 1% × 3

- Interest payable = ₹2,220

Section 234B Trigger

- Required minimum by 31 March = 90% of ₹3,20,000 = ₹2,88,000

- Suppose total paid by March = ₹2,60,000

- Shortfall = ₹28,000

Section 234B interest applies from 1 April until full payment at 1% per month.

Table of Old Tax Regime and New Tax regime for 2025-26

| Old Tax Regime | New Tax Regime u/s 115BAC | ||||

| Income Tax Slab | Income Tax Rate | *Surcharge | Income Tax Slab | Income Tax Rate | *Surcharge |

| Up to ₹ 2,50,000 | Nil | Nil | Up to ₹ 3,00,000 | Nil | Nil |

| ₹ 2,50,001 – ₹ 5,00,000** | 5% above ₹ 2,50,000 | Nil | ₹ 3,00,001 – ₹ 7,00,000** | 5% above ₹ 3,00,000 | Nil |

| ₹ 5,00,001 – ₹ 10,00,000 | ₹ 12,500 + 20% above ₹ 5,00,000 | Nil | ₹ 7,00,001 – ₹ 10,00,000 | ₹ 20,000 + 10% above ₹ 7,00,000 | Nil |

| ₹ 10,00,001- ₹ 50,00,000 | ₹ 1,12,500 + 30% above ₹ 10,00,000 | Nil | ₹ 10,00,001 – ₹ 12,00,000 | ₹ 50,000 + 15% above ₹ 10,00,000 | Nil |

| ₹ 50,00,001- ₹ 100,00,000 | ₹ 1,12,500 + 30% above ₹ 10,00,000 | 10% | ₹ 12,00,001 – ₹ 15,00,000 | ₹ 80,000 + 20% above ₹ 12,00,000 | Nil |

| ₹ 100,00,001- ₹ 200,00,000 | ₹ 1,12,500 + 30% above ₹ 10,00,000 | 15% | ₹ 15,00,001- ₹ 50,00,000 | ₹ 1,40,000 + 30% above ₹ 15,00,000 | Nil |

| ₹ 200,00,001- ₹ 500,00,000 | ₹ 1,12,500 + 30% above ₹ 10,00,000 | 25% | ₹ 50,00,001- ₹ 100,00,000 | ₹ 1,40,000 + 30% above ₹ 15,00,000 | 10% |

| Above ₹ 500,00,000 | ₹ 1,12,500 + 30% above ₹ 10,00,000 | 37% | ₹ 100,00,001- ₹ 200,00,000 | ₹ 1,40,000 + 30% above ₹ 15,00,000 | 15% |

| Above ₹ ₹ 200,00,001 | ₹ 1,40,000 + 30% above ₹ 15,00,000 | 25% | |||

- Tax rates for Individual (resident or non-resident), 60 years or more but less than 80 years of age anytime during the previous year are as under:

Behavioural Mistakes That Trigger Interest

Most mistakes in advance tax come from habits, not bad math. Since earnings feel unpredictable, people put off calculating what they owe. When profits seem covered by write-offs, planning gets skipped – then shortfalls show up. Waiting until it is time to file means scrambling over missed investment credits. Waiting too long to crunch numbers often backfires by limiting fixes later on. Breaking it into four parts each year stops small issues growing unseen.

Real-Life Case Studies

Freelancer Expansion Case: Starting out, Rohit projected earnings of ₹14 lakh, yet landed overseas customers by summer, pushing total income up to ₹22 lakh. Despite the jump, he held back on updating his advance tax payments, counting on a lump-sum fix come March. Missed targets in April and July built up penalties under Section 234C. Come filing time, extra charges popped up – over ₹5,000 lost, simply because updates every quarter were skipped.

Salaried Investor Case: When markets surged, Anita made five hundred thousand rupees trading shares. Her company took out full income tax straight from pay. Yet when it came time to settle accounts, gaps showed up across two payment deadlines. The profit wasn’t taxed earlier, so penalties piled on without warning. Filing revealed extra dues triggered by those delays. Cash ran tighter than expected once numbers were finalized.

Rental Income Misjudgement: One property belongs to Mr. Verma, another too – he thought a blank month would shrink the tax on rent by just that fraction. Yet hidden rules pushed up what counted as income. Payments due in September dipped below the needed share, so did those in December. Slowly, extra charges built through each quarter, exposing how wrong guesses can backfire.

Mid-Year Bonus Adjustment: That December, Neha got a big performance bonus. Even though her employer split the TDS change over the rest of the year, taxes paid by then still fell short of three-quarters. Because of that gap, interest under Section 234C kicked in. Had she redone the math earlier, the extra charge might never have happened.

Conclusion

Knowing how to calculate advance tax correctly is not merely about avoiding statutory interest; Staying on track financially means keeping steady habits all twelve months. Because pay checks now come from more places – while paperwork links tighter – guessing taxes every three months matters more. A tiny fee here, another there might seem small at first; together, they slowly drain resources. Many taxpayers only realise the impact when facing notices, similar to situations avoiding income tax penalties in 2025. Planning those estimates carefully, updating them when needed, following payment dates keeps cash ready and future goals safe.

FAQs

Q1: Is advance tax compulsory for salaried employees?

When taxes owed go above ₹10,000 after TDS is taken out, salary earners must pay in advance. Often, extra money – like from selling assets, rent, or contract work – leads to this need.

Q2: What happens if I miss one instalment?

Failing to pay a full instalment means extra charges kick in – Section 234C adds 1% monthly interest on what’s missing. When tax returns are filed, even small gaps bring calculated penalties based on how long they lasted.

Q3: Can I revise advance tax later in the year?

Yes, advance tax estimates can be revised in subsequent quarters if income changes. However, earlier shortfalls may still attract interest for the relevant period.

Q4: What is the difference between Section 234B and 234C?

When a quarterly payment falls short within the year, Section 234C comes into play. Payment ending up below 90 percent of the overall tax by March 31 triggers Section 234B, sticking around until everything is settled.

Q5: Does presumptive taxation affect advance tax rules?

Under presumptive taxation schemes, advance tax is typically payable in a single instalment by 15 March. However, liability still arises if total tax exceeds ₹10,000.

Disclaimer

This article is for educational purposes only and does not constitute professional tax advice. Tax laws and interpretations may change. Individual circumstances vary, and readers should consult a qualified tax professional or verify details from official government sources before making decisions.