Learn how to start SIP in mutual funds in India with this detailed beginner guide. Follow powerful steps, avoid costly mistakes, and build long-term wealth smartly. how to start SIP in mutual funds, SIP investment for beginners India, mutual fund SIP guide India, SIP benefits India, how to invest monthly India.

Introduction: Why Most People Struggle to Build Wealth

Money comes in small steps across India, yet hardly anyone thinks about growing it. Pay checks grow at a crawl while daily costs climb without pause, so cash sits stuck behind low-interest walls. Eventually, income just replaces itself – working hard brings no momentum. What truly separates people isn’t pay checks. It’s whether they follow a clear path to build lasting value over time.

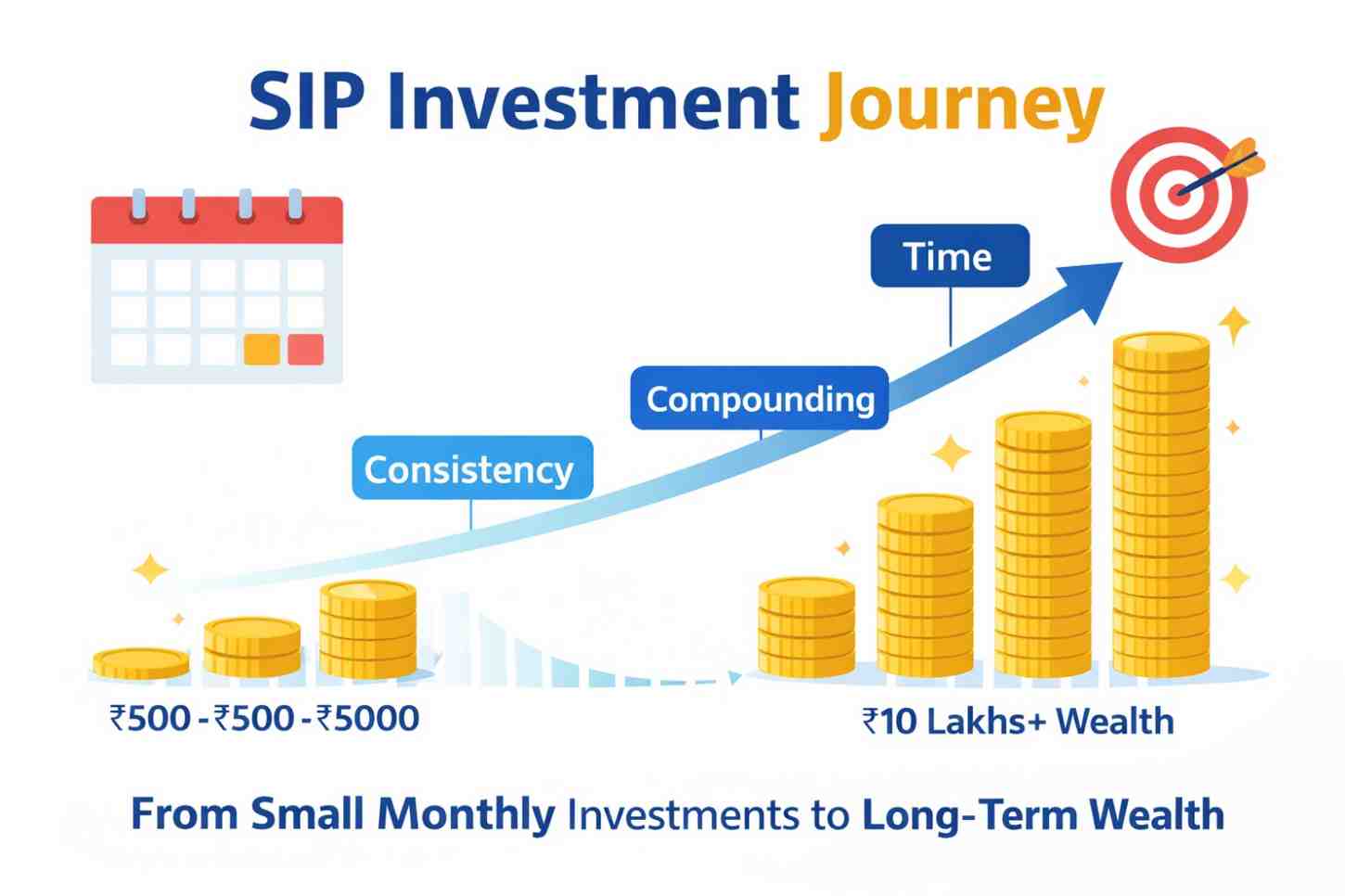

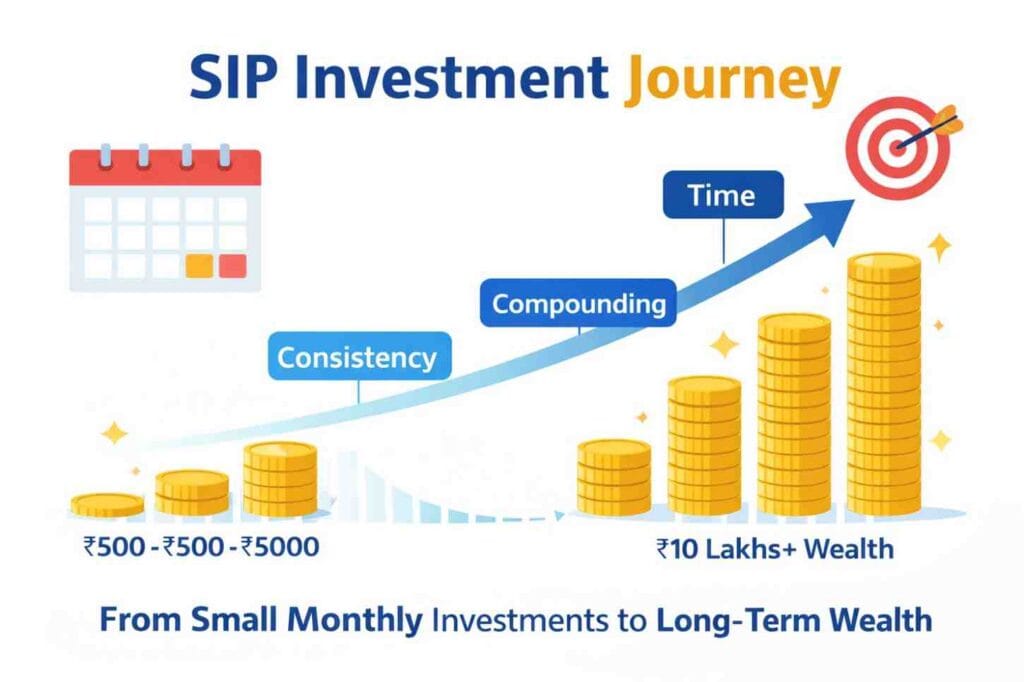

One way to tackle the issue is through a Systematic Investment Plan, which brings structure to how people invest. Rather than waiting for the perfect moment or needing lots of money at once, small regular contributions add up over time because steady habits shape results more than sudden moves. Even small investments, when done regularly, can grow significantly due to the power of compounding, which is the backbone of long-term investing.

This article will guide you step-by-step on how to start SIP in mutual funds in India, with practical clarity, real-life examples, and strategic insights.

What is SIP in Mutual Funds

Every month, money moves automatically into your investment. This setup skips the stress of timing the market. Rather than guessing entry points, you follow a steady rhythm. Emotions fade out when actions repeat on schedule. Decisions shrink down to one choice: starting.

Hesitation melts when you start doing things differently. That single shift handles what trips most newcomers up. Buying mutual fund units at various market points happens when investing via SIP. Because of this timing spread, the average purchase price evens out – rupee cost averaging in action. Market swings matter less down the road, thanks to that steadier base. Long term gains often turn more favourable because of it.

Apart from that, SIP fits right into how you plan your money. For example, if you are also exploring tax-saving investment options in India, you can invest in ELSS funds through SIP and get both tax benefits and market-linked growth.

Why SIP Works So Well

Most folks struggle with knowing when to jump in. SIP sidesteps that mess entirely. By making moves automatic, it skips guesswork. Over time, those steady steps add up quietly. Timing worries fade out. Success grows through rhythm, not luck. Every time you put money in regularly, you end up riding along with peaks and dips without needing to watch closely. When prices drop, each dollar buys extra shares, yet when things climb, those earlier purchases start gaining worth. Over months, this push and pull smooths into steady progress.

Here’s why SIP sticks – it shapes habits quietly. Effort fades into background because the system runs on its own. Money moves without waiting for a reminder. Skipping feels harder when the process hums along by itself. Truth is, time makes SIP effective. As months stack up, growth builds on itself quietly. That’s how modest sums grow meaningfully across a decade or two. Lengthy commitment turns tiny inputs into something substantial. Mutual funds are regulated investment instruments, and you can verify details on the <a AMFI India website.

How SIP Actually Functions in Real Life

Once it is running, SIP works without needing much attention. Picking a mutual fund comes first – match it to what you want and how much risk feels right. Next up, lock in how much money to put in plus when it should happen. Come that day each month, the sum moves straight out of your bank without needing to lift a finger.

Fresh each morning, the fund splits pieces into your name using that day’s cost. On it goes through every month, come rain or shine. Later on, picking up shares bit by bit means each batch costs a little differently – smoothing out what you pay overall. Because of that shift, stepping in slowly cuts down risk more than going all in at once while keeping you active in trading steadily. If you want to understand how different assets compare in this process, exploring gold vs other investment options can help you see why mutual funds are preferred for long-term growth.

7 Powerful Steps to Start SIP in Mutual Funds in India

Step 1: Define Your Financial Goal Clearly Before You Invest

Starting SIP without knowing your reason? That changes everything that follows. It isn’t paperwork – it shapes each move you take. No target means drifting, quitting early, reacting when stress hits. Picture your money moving toward something real. That shape comes from naming a clear target for your SIP. Without that, choices about time or risk feel loose, ungrounded. Picking funds gets easier when you know what they’re meant to do. Retirement isn’t rushed; it grows slowly, quietly. A new phone next year? That needs steadier hands, less motion. Each aim pulls the plan in its own direction.

With a target in sight, swings in the market matter less since attention moves past quick gains toward what lies ahead. Because of this, steady effort grows stronger – key when following a SIP plan over time. Most new investors rush past this part, diving straight into buying assets – only to face chaos down the line. Yet pausing matters; ask what you truly want: growing riches, a safety net, or preparing for years ahead. Clarity shapes everything, even when it feels slow at first. Without clear intent, every choice wobbles.

Step 2: Choose the Right Mutual Fund Based on Strategy, Not Trends

Selecting a mutual fund matters more than most realize when starting an SIP, and understanding how to choose the right mutual fund in India can help you make better decisions, though people usually get it wrong. Instead of checking suitability, lots jump in because a fund did well lately or everyone talks about it. Most of the time, matching your investment to your personal plan matters more than chasing high returns. Pick something that lines up with what you want, how long you can wait, also how much uncertainty feels okay. New investors often do fine with straightforward picks – say, big company funds or market indexes – since these track reliable businesses while skipping wild swings.

Complicated portfolios tend to backfire. Piling up fund after fund might feel safe, yet outcomes get muddy fast. Pick just a single solid option – sometimes even two – and stick close at first. Clarity shows up where simplicity lives. Start steady, not fast. Pick what lasts, rather than what shines now. Choose a fund that’s been around, one with fewer surprises. It matters less how big the gain is this year. What counts is showing up every year without shock or collapse. Staying put beats jumping around. A fit choice today may still make sense five years from now.

Step 3: Complete Your KYC Smoothly and Start Without Delay

Starting out with investments means doing KYC first – it’s required. Yet calling it a hurdle misses the point. These days, going digital makes the whole thing fast. Most people finish it online without stepping into an office. The steps line up smoothly if you have your documents ready. Start off by gathering essentials – a PAN card sits next to your Aadhaar, both paired with active bank info. After sending them in, verification kicks in quietly behind the scenes. Only then does KYC light up, clearing the path for mutual fund moves. Freedom to invest shows up once everything checks out.

What really slows things down isn’t the steps involved, yet the pause that comes from waiting. Some put off KYC believing there’s always tomorrow – this wait quietly pushes back when they start investing too. Because SIP grows best over years, losing even a handful of months matters more than most expect. Time slips fast; starting late means missing what early effort builds. Picture KYC like setting up a tool just once – then using it again and again to put money into investments. Finish it early, then begin shaping what comes next with your finances without delay.

Step 4: Select a Reliable and Simple Investment Platform

Smooth investing often depends on which platform you pick. Since the wrong one adds clutter instead of clarity. Picking a tool that trims the noise helps more than loading extra buttons no one needs. You should always invest through trusted platforms and follow SEBI official guidelines for safety. Cluttered screens slow decisions down. Simplicity keeps things moving without hiccups along the way. Pick a service where you can invest straight into mutual funds, because those options usually charge less than standard ones. A tiny gap in costs might not seem like much now, but it adds up over years. That extra money staying in your pocket makes the direct route better if you are planning ahead.

Starting out feels simpler when things just work. A clear layout, straightforward monitoring, then hassle-free trades help keep nerves calm along the way. Apps such as Groww or Zerodha shape their tools around new users, so stepping in becomes natural right away. Safety matters just as much as clear information. When putting money into something, go only where rules are followed strictly. Places you can count on keep your funds protected while letting you reach them whenever needed.

Step 5: Decide Your SIP Amount Based on Comfort and Consistency

Starting small? That’s something SIP makes possible. Picking how much though – it needs a bit of thinking. Go with a sum that fits so investing each time feels natural, even when bills pile up. Jumping in too fast often leads new folks to set big numbers at first – then scale back when money gets tight. Instead, beginning small lets you build steady momentum without stress weighing down each step forward. Grow the number slowly, tied closely to how much comes in each month, nothing forced or rushed ahead.

Starting slow beats stopping early. A tiny monthly investment, if kept going year after year, grows quietly but deep because of how numbers multiply over time. What counts most is showing up each month, not chasing fast wins. Sticking with it slowly builds strength without flash or noise. When your pay check goes up, think about boosting your SIP too. Called a step-up SIP, this move helps money multiply faster by matching rising earnings. Growth happens steadily, yet keeps spending comfortable. As income climbs, so does investment power – without pressure on budgets.

Step 6: Automate Your SIP to Build Discipline Effortlessly

What makes SIP stand out? Automation wipes out guesswork tied to people. Once set up, money moves without waiting on memory or monthly choices. Every month, money moves from your account to your SIP on its own. Because it runs like clockwork, timing never slips – no matter how busy you are. Missing a payment fades into irrelevance when the system handles it silently.

Picking the correct day matters just as much. Go for one shortly after payday hits your account – makes saving jump ahead of spending. That way, money moves into investments before anything else gets paid. Doing it like this turns priority into practice without needing willpower each time. Slowly, money moves on its own, shaping choices without daily decisions. Without hassle, progress continues – no push needed, just motion carrying forward.

Step 7: Stay Invested and Focus on Long-Term Growth

SIPs kick off easily enough. Sticking with them, though – that’s what trips people up. Numbers dip. Markets wobble. That kind of moment shakes new investors. Doubt creeps in. Then they pull back. Consistency slips. Progress halts. Staying put through ups and downs often brings better results than chasing quick shifts. Years matter more than months when it comes to how SIPs unfold. With time, gains build on gains – slow at first, then faster – as markets bounce back and move forward. Lengthy stretches in the game open doors that brief runs simply cannot.

Every now and then, take a look at how your investments are doing – yet steer clear of tweaking things nonstop when markets shift briefly. Staying steady matters more than reacting every time something new pops up. Sometimes it’s not about flawless choices, yet showing up again matters more. Through time, keeping money in play turns regular investing into something stronger than expected.

Real-Life Example of SIP Growth

Imagine a working professional who makes ₹30,000 a month and chooses to use SIP to invest ₹3,000 each month.

- Right away, it seems tiny – almost too little to matter

- Some time passes – about two or three years – and then the numbers begin shifting in a noticeable way

- Falls in the market mean extra units get picked up when costs drop

- Over time, compounding starts accelerating returns

- A decade passes. Money put aside slowly becomes much more. Time changes small sums in surprising ways

- It hits the investor – sticking with it beat trying to nail the perfect moment every single time

- A tiny routine at first grows into something steady beneath your money choices

This example highlights how SIP works silently in the background and builds wealth over time.

Common SIP Mistakes

Many investors fail because they disrupt the process rather than because SIP is ineffective.

- Stopping SIP during market crashes: This is the most common mistake. Market dips are actually opportunities to accumulate more units at lower prices.

- Chasing high-return funds blindly: Selecting funds based only on recent performance often leads to poor long-term results.

- Lack of clear financial goals: Without a goal, investors lose direction and withdraw prematurely.

- Investing in too many funds: Over-diversification creates confusion and reduces effectiveness.

- Expecting quick returns: SIP is a long-term strategy. Short-term expectations lead to disappointment.

Avoiding these mistakes is more important than finding the perfect investment.

Practical Insights to Improve SIP Performance

To maximize the benefits of SIP, focus on strengthening your strategy:

- Increase SIP Amount Each Year

- Stay invested for at least 5–10 years

- Keep your portfolio simple (2–3 funds max)

- SIP Aligned to Long Term Financial Goals

- Avoid frequent changes based on market noise

- Combine SIP with budgeting and saving habits

Over time, these minor adjustments can greatly improve your outcomes.

Conclusion

What makes SIP different isn’t clever tricks. Starting small works because it fits regular life. Staying steady matters more than big moves at once. Growth happens quietly when effort doesn’t stop. Simplicity turns into strength over years. Waiting patiently shapes results most. Planning well removes guesswork later. Perfect moments never arrive – beginning does. Large sums aren’t required to begin building. Begin now. Stick with it. Slowly, doing this every day turns into a choice that shapes your money future more than most others.

FAQs

Q1: What is the minimum amount needed in India to begin SIP?

Depending on the mutual fund you select, you can begin a SIP with as little as ₹500 each month. Because of this, SIP is very accessible to novices, students, and even people with low incomes. Starting early is more important than starting large since compounding allows even a small sum to grow tremendously when invested regularly over time.

Q2: For novices, is SIP preferable than lump sum investments?

Because SIP lowers the danger of investing at the wrong time, it is typically a better choice for novices. You can take advantage of rupee cost averaging and steer clear of market timing errors by making recurring investments. While SIP works well even if you have little information or expertise, lump sum investing necessitates a deeper understanding of the market.

Q3: Can I increase my SIP amount later?

Yes, depending on your financial circumstances, you can raise your SIP amount at any moment. This is referred to as a “step-up SIP,” in which you progressively raise your investment as your income increases. Regularly raising your SIP can greatly increase your long-term earnings without placing an unexpected strain on your finances.

Q4: What occurs if I fail to make a SIP payment?

Your investment is not automatically canceled if you fail to make a SIP payment. That installment is simply skipped by the SIP, and subsequent installments proceed according to plan. For better long-term outcomes, it’s crucial to maintain consistency because missing payments on a regular basis might undermine your investment discipline.

Q5: How long need I keep using SIP in order to achieve positive returns?

SIP is a long-term investment plan, and in order to see significant returns, you should ideally stick with it for at least five to ten years. The impact of compounding increases with the length of time you invest. Patience and persistence are essential for optimizing SIP benefits because short-term investments could not yield the anticipated profits.

Disclaimer

This article shares knowledge just to inform, never to guide money choices. Since mutual funds face shifts in markets, gains aren’t promised. Talking with an approved finance expert helps when planning where to put funds. Goals around money and comfort with uncertainty need checking first.