Learn how to calculate the right term insurance amount in India using 5 smart methods, real-life examples, expert tips, and common mistakes to avoid for complete financial protection. term insurance amount, ideal term insurance amount, term insurance calculation India, life cover calculation India, insurance for salary India.

Introduction

Most folks see term insurance as smart money planning. Yet only a handful know what coverage level fits their life. Trouble starts not when there’s no policy, but when the sum insured misses the mark. Too little protection leaves loved ones short on funds down the road. Too much means handing over extra cash each month – cash better used somewhere else. In India, this mismatch pops up again and again. Why? Because guesses take the place of clear math.

Truth sits quiet sometimes. Your coverage needs to match how money actually moves – what you earn, what goes out each month, debts hanging around, plans down the road. Skip that picture? Even choices made with care might leave loved ones exposed. For instance, if a large portion of your income goes into EMIs, optimizing them through strategies such as reducing high-interest debt via lower personal loan interest burden can directly impact how much insurance you can realistically afford while maintaining financial balance.

Why Most People Choose the Wrong Term Insurance Amount

Most people choose the wrong term insurance amount because they treat insurance as a one-time formality rather than an ongoing financial decision. Out here, people skip checking their actual money flow, grabbing random figures tossed around by advisors or friends instead. When that happens, personal details like pay size, monthly bills, or family duties get lost – so coverage ends up too thin or way too heavy. Over time, costs keep rising – ignoring this can cause big problems. Money needed now won’t stretch as far later. Picture a home spending ₹40,000 monthly at present, yet needing double that amount years ahead. Without adjusting protection for these shifts, even insured families might struggle. So when plans stay fixed, reality can quickly outpace them.

Money owed sticks around, long after someone passes. Debts like mortgages, auto loans, or personal borrowing stay active. Without enough insurance, loved ones might sell property just to keep up. They could even borrow more, adding pressure. When monthly payments are already tight, that burden grows fast. Staying on track with money habits helps avoid deeper strain later. Additionally, a lot of people overestimate their savings. While building reserves through disciplined approaches like maintaining an financial cushion for emergencies is essential, it cannot replace the immediate protection provided by insurance. Funds grow slowly over months or years – yet protection kicks in right away.

Most people forget how much they count on job-based health plans. When company rules change, protection can vanish overnight – especially after leaving a role. Counting only on that safety net? It feels safe until it isn’t. Gaps appear fast, exposing loved ones when least expected. Only now do some realize how often insurance stays untouched. When you tie the knot, welcome a baby, or earn more, duties shift fast – yet plans stay frozen. Coverage meant for yesterday might leave gaps tomorrow if never reviewed. What felt right before could fall short without a second look.

5 Smart Ways to Calculate the Right Term Insurance Amount

1. Income Replacement Method

The income replacement method is one of the most widely used approaches because it provides a simple way to estimate the term insurance amount. A life plan often means keeping money flowing for loved ones when you are gone. Ten to twenty times what you earn each year might be enough, though it depends on how old you are, who relies on you, and where you stand in your work path. What matters most is matching coverage to real needs over time. If you earn ₹6 lakh every year, aim for insurance between ₹60 lakh and ₹1.2 crore. Those just starting out might want more – say eight to ten times their salary – because they have decades of income ahead. People nearing retirement could go lower, maybe five to six times, since fewer working years remain. When life ends unexpectedly, this cushion keeps loved ones from financial strain.

A person might think replacing lost income is enough, yet that overlooks what they already owe or own. Savings tucked away somewhere could reduce how much protection feels necessary. Picture someone with big investments – coverage needs shrink in those cases. But debt piles up quietly, making a basic calculation fall short when life gets complicated. Money buys less as years go by, which makes inflation worth thinking about. Today’s replacement income might fall short later on. Even with flaws, this approach gives a useful beginning, keeping essential family costs within reach.

2. Expense-Based Calculation

Money habits at home shape the starting point when figuring costs. Rather than measuring what comes in, this way looks at what goes out to keep things running smoothly day to day. A set timeframe helps pin down totals without guessing future earnings. Figure out what you spend every month – things like bills, housing payments, school fees, medical needs, clothing, food. Take that total, times it by twelve for a year’s worth of spending. That yearly amount? Run it through how many years your loved ones might need support from you.

Say your monthly spending is ₹40,000, then each year it adds up to ₹4.8 lakh. When your loved ones need money for two decades, that total jumps to ₹96 lakh. With this approach, life keeps moving smoothly for them, even if you’re not around. So long as numbers hold steady, pressure stays low on finances. A big plus here? The method hits close to actual money demands, skipping guesswork. Real numbers shape it, not estimates pulled from thin air. Still, rising prices matter – what costs now won’t stay fixed down the road. Surprises pop up too: hospital visits, weddings, sudden moves – they all weigh in.

When expenses stay predictable, this approach works well. Clear insight into needed funds comes easily, preventing too little or too much coverage. What matters shows up without confusion, simply by following the numbers as they are.

3. Liability + Goals Method

The liability plus goals method is one of the most comprehensive approaches to calculating the ideal term insurance amount. Because life changes, coverage needs to match what you owe now along with where your money plans are headed. Start with writing down every debt you carry – mortgages, personal borrowing, vehicle financing included. Moving ahead, think through what money you’ll need later – college for kids, wedding costs, helping your partner after work ends. At the close, take away anything you already own that holds value: bank balances, market stakes, locked-in deposits.

Say you owe ₹30 lakh, aim to save ₹50 lakh later, yet only have ₹10 lakh set aside – then ₹70 lakh in cover makes sense. That way, loved ones pay off what’s owed while still reaching key plans ahead. What makes this approach work well is how it tackles actual money concerns head on. People juggling big commitments or looking far ahead often find it helps them stay steady. Yet things can go off track without clear plans and realistic guesses about costs down the line.

Understanding how to balance liabilities and assets is also crucial in broader financial planning, which aligns with structured approaches such as allocating money across safety, growth, and liquidity buckets to ensure stability and long-term wealth creation.

4. Human Life Value (HLV) Method

Picture what you bring in over time, shaped by pay now plus how much that might grow. Think ahead – years left at work matter, just like rising costs will shift real value. Money later gets scaled down to today’s terms, since a dollar changes across time. What shows up is a number tied to ongoing contributions, nothing more. Picture this working like a safety net, catching what your loved ones might miss financially when you are gone. Suppose you hit 30, hold steady work, and see pay rise over time – those future earnings add up fast. That total adds weight to how much coverage makes sense. The policy number on paper ought to mirror the income path ahead.

Starting off, professionals often rely on this approach when mapping out money plans – much like how the Life Insurance Corporation of India operates. A clear picture of your actual worth emerges because it digs deep into real numbers instead of guesses. Beyond its tricky setup, this approach ranks among the sharpest tools for pinning down your right term life coverage. People building careers with steady pay bumps ahead tend to get the most from it.

5. Quick Rule of Thumb

Picture this: a shortcut for folks seeking fast answers without math headaches. This way works by taking your yearly pay and stretching it about fifteenfold for coverage size. A person earning ₹8 lakh each year might aim for about ₹1.2 crore in coverage. Simple to follow, yet it still offers a decent safety net when things go off track. Starting here makes sense more often than not.

Still, don’t treat this approach as the last word. Without factoring in debts, what you aim for later, or your current money reality, it falls short. Think of it more like step one – something to begin with before diving into deeper analysis. Still, basic as it may seem, this method keeps you from being left too exposed. Adjustments come after better numbers show up.

Real-Life Examples

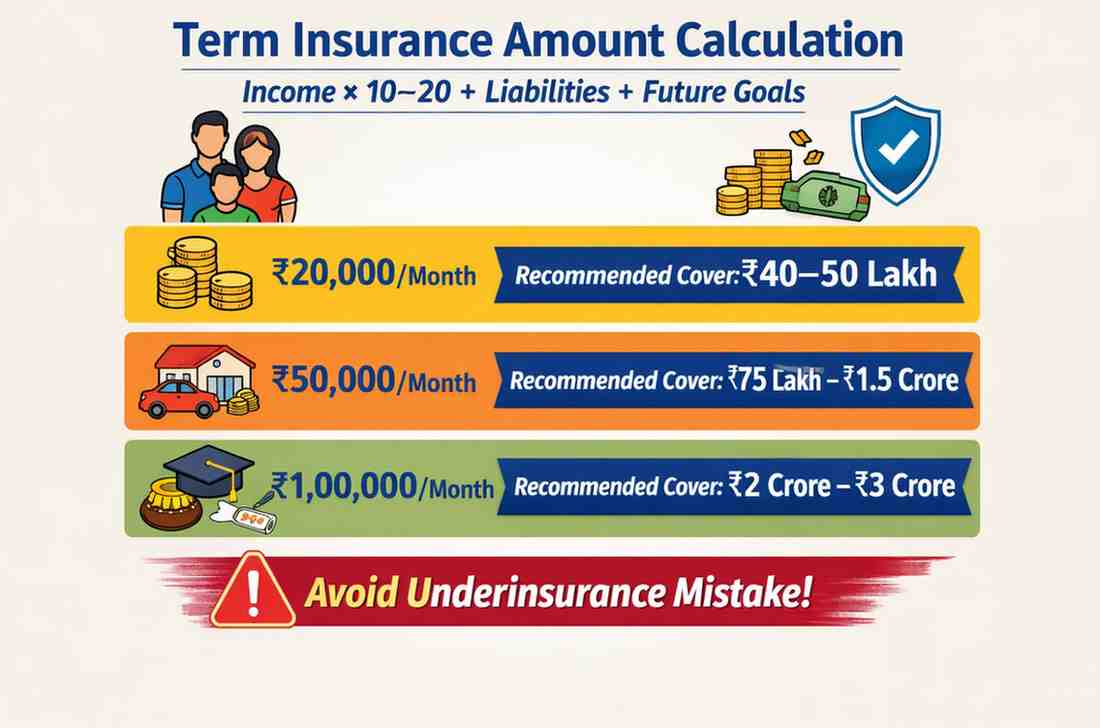

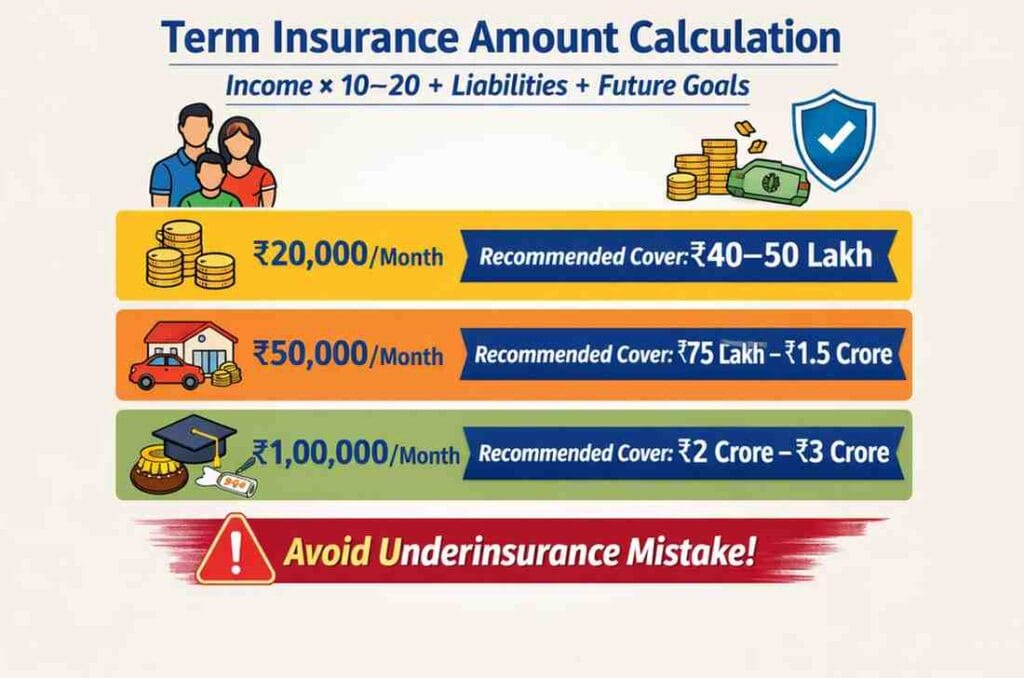

₹20,000 Monthly Income: Making ₹20,000 a month usually means tight money choices and heavy reliance on each pay check. Still, bills like rent, groceries, power, and daily essentials take up most of that amount. Because of this, picking minimal insurance might leave loved ones struggling sooner than expected. A person spending ₹15,000 each month will need ₹1.8 lakh every year. Stretch that across two decades, it climbs to ₹36 lakh total. Once you factor in rising prices and unforeseen needs, aim closer to ₹40–50 lakh for coverage. That cushion helps loved ones stay steady when regular costs pile up. Stability matters most after someone is gone.

₹50,000 Monthly Income: A salary of ₹50,000 each month often comes with bigger duties – supporting a household, paying for kids’ schooling, handling loan repayments. Spending every month might sit anywhere from ₹30,000 up to ₹40,000. A ₹20 lakh loan combined with future goals of ₹25 lakh adds up to ₹45 lakh in needed funds. When factoring in rising costs and lost earnings, coverage from ₹75 lakh to ₹1.5 crore makes sense. That kind of buffer handles today’s debts along with tomorrow’s needs. What matters is staying covered beyond just the present.

₹1,00,000 Monthly Income: A person making ₹1 lakh each month often lives more comfortably yet faces bigger money responsibilities. Because of their income, they might carry home loans alongside school fees and savings plans. When they spend ₹70,000 every month, that’s ₹8.4 lakh each year. Stretch that across two decades and it climbs to ₹1.68 crore. Toss in debts along with what they plan to achieve later, then protection through a term policy fits best between ₹2 crore and ₹3 crore. With that kind of safety net, money worries fade into the background.

Common Mistakes That Can Cost Your Family Big

Picking too small a term insurance amount trips up plenty of people. Fixating on cheap rates rather than solid protection turns out poorly later. Sure, payments feel lighter at first – yet trouble often shows years down the road. One big error? Overlooking inflation. When prices climb, what seemed like solid protection might shrink fast – suddenly not enough when needed most. Life shifts matter just as much: a new job, a child, or even moving homes changes everything about how much support is truly necessary. Sticking with old numbers means gaps grow without notice.

A surprise waits when policies blend coverage with market promises – returns dip, safety thins. Protection matters most in life plans, nothing else. Separate moves work better: one path for guarding income, another for growing wealth on its own terms. A big error? Not mapping out money moves early. When spending isn’t tracked, plus goals aren’t set, keeping up with needed protection gets shaky. Learning how to manage monthly income effectively can help create room for better insurance planning.

Expert Tips to Choose the Ideal Term Insurance Amount

It takes considerable consideration and frequent evaluation to determine the appropriate term insurance amount. Understanding your financial status, including your income, expenses, liabilities, and future objectives, should always be your first step. It’s critical to assess your coverage on a regular basis. Revaluating your insurance needs should be prompted by life changes like marriage, having children, or earning more money. This guarantees the continued relevance of your coverage. Aligning your insurance with your overall financial plan is also crucial. Combining protection with disciplined investing helps create long-term financial stability. Insights from strong financial habits can help you build a balanced approach.

Picking a solid insurance provider matters, plus getting familiar with what the policy actually says helps too. Rules set by the Insurance Regulatory and Development Authority of India keep things open and guard buyers. Head over to the Insurance Information Bureau of India site if you want clear details straight from the source.

Expanded Term Insurance Calculation Table

| Monthly Income | Base Coverage | With Liabilities | With Inflation Buffer |

|---|---|---|---|

| ₹20,000 | ₹30 lakh | ₹40 lakh | ₹50 lakh |

| ₹50,000 | ₹75 lakh | ₹1 crore | ₹1.5 crore |

| ₹1,00,000 | ₹1.5 crore | ₹2 crore | ₹3 crore |

This table reveals changes in term insurance amounts once actual life conditions come into play. A rough guess falls short, so accurate math becomes essential for solid money safety.

Conclusion

Choosing the right term insurance amount is one of the most important financial decisions you will make. Your family’s future stability hinges on how well plans are set before anything changes. Yet many guess instead of measuring needs with clear numbers, creating risk down the road. When inflation enters the picture alongside debts, a clearer figure emerges through step by step thinking. As life shifts – so should protection levels, quietly adjusting behind the scenes. A single smart choice can guard your money while quieting worries too. What matters most? It’s not simply owning coverage – it’s picking a sum strong enough to shield those who depend on you.

FAQs

Q1: What is the recommended term insurance premium in India?

Your income, expenses, liabilities, and long-term financial objectives all influence the optimal term insurance premium. 10–20 times your yearly salary is a good starting point, but a more precise figure should account for debt, future expenses, and the impact of inflation.

Q2: Is term insurance worth ₹1 crore sufficient?

A sum like ₹1 crore could work if your spending is light and debts are few, yet might fall short for city households where daily life costs more. Think through what you truly need rather than follow common benchmarks without question.

Q3: How frequently should my term insurance be reviewed?

Every two to three years, or anytime a significant life event like marriage, delivery, or a pay raise occurs, you should check your term insurance. Frequent evaluations guarantee that your coverage remains in line with your present financial obligations.

Q4: Can I subsequently raise the amount of my term insurance?

Yes, if your income and responsibilities increase, you can buy more term insurance plans to expand your coverage. This method gives you flexibility and lets you modify your protection over time without having to cancel your current coverage.

Q5: Does the amount of term insurance change with inflation?

Indeed, over time, inflation drastically lowers the value of money, so your present coverage could not be enough in the future. To ensure long-term financial security, it is crucial to factor in an inflation buffer when determining your insurance requirements.

Q6: Do investing plans and insurance go hand in hand?

Because investments and insurance have different functions, it is usually preferable to keep them apart. Investments are made for long-term financial growth and asset generation, whereas term insurance covers only pure risk.

Q7: Can I rely solely on term insurance offered by my employer?

It is dangerous to rely solely on employer-provided insurance because it is typically restricted and might not last if you move jobs. Regardless of your family’s work status, having a separate term insurance policy guarantees consistent and sufficient protection.

Disclaimer

This piece shares information, nothing more, never meant as financial guidance. Needs differ, shaped by personal money matters along with aims each person holds. Speaking with a certified expert makes sense prior to choices being made. Scenarios shown serve clarity, yet fit isn’t guaranteed across every situation. Check straight with the insurance provider what rules apply. Since standards can shift over time, turn to authorized documents for current details.