Discover 5 Powerful Key Personal Finance Rules that can transform your financial future. Learn smart saving, investing, debt management, and wealth-building strategies. Key Personal Finance Rules, personal finance rules, financial planning tips, money management tips, budgeting strategies, emergency fund importance, debt management strategies, wealth building habits, personal finance for beginners, financial independence, investment planning, savings habits, insurance planning, financial security tips, smart money management.

Update (June 2026): This article has been updated to include current personal finance best practices such as disciplined budgeting, emergency fund planning, debt management, long-term investing, and risk mitigation methods. Internal resources, examples, FAQs, and reference materials have been revised to improve accuracy, user experience, and adherence to EEAT and YMYL content requirements. The counsel is still educational in nature and should be examined in conjunction with individual financial circumstances and, where needed, professional advice.

Introduction

Cash shapes most parts of life – what we buy each day, how big decisions unfold, what happens when work ends. Still, plenty go decade after decade making income while skipping lessons on handling cash well. Because of this, some folks pulling decent pay still find themselves stuck, unable to grow steady worth over time. Here’s something worth noting: managing money well doesn’t mean mastering complex systems. Instead, sticking to straightforward personal finance basics puts you in charge of your finances, eases pressure around cash matters, moves you closer to lasting independence. Even if you’ve barely begun handling money on purpose – or already do but want better results – these guidelines build a sturdier base over time.

Why Following Key Personal Finance Rules Matters

Most times, getting ahead financially has little to do with chance or how much you earn. Sticking to smart money habits year after year makes the real difference. Those who handle cash well tend to know exactly where it goes, when it grows, and what keeps it safe. Most people skip basic money habits, yet sticking to them keeps big errors away. When times get rough – like losing work or facing hospital bills – simple rules become a quiet safety net. Choices start coming from thought, not panic, once you learn what actually works. Wealth grows slower when feelings lead every move.

Built on small choices, good money routines bring calm to daily chaos instead of stress. Reaching big milestones – owning a place, paying for school, retiring well, gaining freedom – feels smoother when finances are handled with care. What truly sticks? Doing the right thing regularly, even when no one notices.

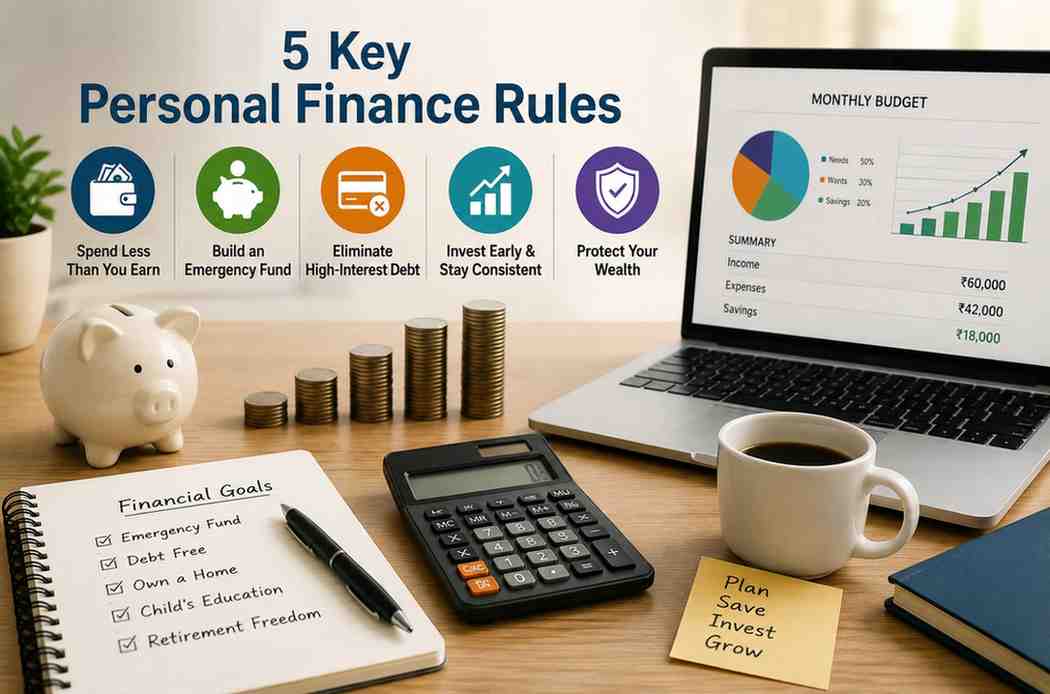

Rule #1: Spend Less Than You Earn

Spending less than you make sits at the core of any workable money strategy. True, that idea seems straightforward – yet lifestyle creep trips up plenty who try. Impulse buys sneak in when attention fades. More pay usually brings bigger bills right behind. Little cash stays free for putting aside once costs catch up. Surprise how much extra shows up when life costs less than income. That leftover money? Tucked away now helps later – when plans shift or trouble hits. Tracking dollars each month reveals spots where cutting back feels painless. Watching habits change once basics stand apart from extras.

When life throws money problems their way, those living below their means tend to handle it better. Because they save regularly, chances to grow wealth don’t slip away easily. If you are beginning your financial journey, learning how to invest your first salary becomes much easier when you already have a healthy savings habit. Life still holds room for joy even while managing money. What matters most shows up when choices today support what comes later financially. Begin anywhere else and things get shaky fast. Solid extra income each month makes everything after it possible.

Rule #2: Build and Maintain an Emergency Fund

When life throws surprise bills, money might get tight. Things like hospital visits, losing work, fixing cars, house fixes, or helping relatives add up fast. A stash of saved cash helps absorb the hit when these moments arrive. When life throws surprises, cash set aside keeps stress low. Most folks turn to costly loans without a buffer, digging deeper into trouble. A stash just for tough moments means fewer sleepless nights. Experts often suggest covering basic costs for half a year in something reachable fast. That kind of cushion changes how you handle sudden setbacks.

What matters most in an emergency fund is being able to access money fast – growth takes a back seat. Money sits there ready, not stretched for gains. According to the Reserve Bank of India (RBI), maintaining adequate liquid savings can help households manage unexpected financial disruptions without excessive dependence on borrowing. When things go wrong, having space to breathe matters more than pushing forward fast. Money set aside quietly does its job when surprises hit – turns short stumbles into recoveries instead of spirals.

When life throws surprises, having savings helps think clearly. Those with money set aside rarely feel pushed into quick fixes when pressure builds. Slow progress toward a cushion? Worth every step, since steady preparation shapes solid ground beneath finances.

Rule #3: Eliminate High-Interest Debt Quickly

When handled carefully, owing money might actually help. Yet costly interest charges usually stand in the way of getting ahead. Instead of building wealth, people pay fees just to stay even. Monthly payments on cards or unsecured loans eat up cash that could go elsewhere. Interest doesn’t help when it’s piling up on what you owe. Growth in your savings builds slowly, yet what you owe grows faster than expected. Lenders gain more each month while your progress stalls just as much. Saving enough feels harder because payments eat into funds meant elsewhere.

Paying off costly loans first often helps money problems fade quicker, even when compared to aiming for bigger gains in investments. Many borrowers use strategies such as the Debt Avalanche vs Snowball method to accelerate repayment and stay motivated throughout the process. Free of debt, your wallet breathes easier each month while pressure slips away. With room to move, funds shift naturally into saving, growing, or what matters most. Handling what you owe isn’t only cutting numbers – it’s opening doors that lead to building more down the line.

Rule #4: Start Investing Early and Stay Consistent

Most folks think big cash is needed before jumping into investments. Truth? Starting early beats waiting for a windfall every single time. Patience quietly outperforms lump sums when decades stretch ahead. When you begin sooner, time helps your gains grow gradually. A head start means more rounds of growth stacking up quietly behind the scenes. Even small, consistent investments can grow substantially over decades. This is why understanding the power of compounding is essential for every investor.

Sticking to a routine matters just as much. Jumping in and out based on guesses about where prices are headed usually means losing out. Showing up steadily, putting money aside without fail, softens the blow of wild swings across time. That steady pace builds value slowly, almost without notice. Investor education initiatives by the Securities and Exchange Board of India (SEBI) consistently emphasize disciplined and long-term investing over short-term speculation.

When markets bounce around, people sticking to their plans usually do better than those jumping at every twist. Staying calm matters more than timing moves perfectly. Showing up regularly without drama builds stronger results over time.

Rule #5: Protect Your Wealth Through Insurance

Years pass while growing wealth, yet one surprise moment might weaken everything built. Protection through insurance matters because it guards what you save, shielding it from sudden loss. Paying for doctor visits gets easier when coverage steps in before costs drain your wallet. The Insurance Regulatory and Development Authority of India (IRDAI) advises consumers to review policy coverage, exclusions, and adequacy before purchasing insurance Should medical bills climb, having solid health protection matters more than ever. When the main provider dies too soon, term life steps in to help those left behind. What changes lives isn’t just income – it’s what happens when that stops suddenly.

Getting the kind of protection you need matters a lot. Understanding the appropriate term insurance amount can help ensure your family’s future financial needs are adequately protected. Picture insurance first as protection against what might go wrong, not a way to make money. When things get tough, good policies keep your savings safe while cutting down on stress about costs. Staying steady financially matters just as much as building up more cash over time.

Bonus Rule: Set Clear Financial Goals

Money moves with more sense when you know what it’s meant to do. Picture aiming without a target – saving feels confusing, investing seems random, tracking wins almost impossible. A plan takes shape once dreams get dollar signs attached. What looked like guesswork turns into steps forward. A sudden start could mean saving for emergencies or clearing what you owe. Maybe down the road comes buying a place to live, or covering college costs somehow. Later on, thoughts turn toward stepping back from work, living freely without needing a pay check.

Staying focused on clear targets shapes how money gets used, guiding choices with more consistency. When markets shake or economies wobble, those same aims become anchors – keeping actions steady even when emotions rise. Many investors use goal-based investing strategies to align investments with specific financial objectives. Regularly assessing and revising goals keeps your financial plan relevant as circumstances change. A well-defined goal motivates people and helps them retain consistency throughout time.

Common Mistakes People Make

Some folks earn well yet still face money troubles – often due to repeated missteps. Spotting those slipups sooner rather than later keeps stress low and progress steady.

- Spending More Than They Earn: Many people increase their spending as their income rises, leaving little room for savings or investments. Even with a larger salary, lifestyle inflation might cause long-term financial stress. Spending more than you earn on a regular basis generally leads to debt accumulation and inhibits your ability to develop wealth.

- Ignoring Budgeting and Expense Tracking: Month after month, cash slips away when there’s no plan to follow. Tiny costs that seem harmless – like snacks or subscriptions – creep higher without warning. Watching every dollar spent reveals habits hiding in plain sight. Choices get clearer once numbers stop being guesses.

- Skipping Emergency Savings: Out of nowhere, a hospital visit, sudden unemployment, or a broken furnace might show up. When there’s no savings buffer, folks tend to turn to credit lines or borrowing instead. That move? It piles on stress, slows down debt payoff, and side-tracks what they’re trying to achieve.

- Waiting too long to invest: Most folks put off investing, thinking big cash is required. Yet holding back too long chips away at compound growth, quietly undermining future goals. Better outcomes usually come from beginning sooner, tiny sums included. What matters most shows up over years, not months.

- Carrying High-Interest Debt: Most folks carrying credit card bills plus personal loans pay steep interest. That pile of debt eats into what’s left each month, leaving little room to set money aside. When someone sends just the bare amount due, they often stay stuck paying interest forever. A single misstep here stretches repayment far longer than expected.

- Ignoring Insurance Protection: Money means everything to certain people, yet they ignore what happens when things go wrong. Trouble strikes fast – a sickness, a crash, one sudden loss – and without proper coverage, money vanishes just as quick. Protection keeps hard-earned cash safe, even when life turns harsh out of nowhere.

- Chasing Quick Returns and Market Trends: Hot stocks pull in plenty of investors, especially when social media hypes quick wins. Yet hunting fast money tends to cloud judgment, opening doors to avoidable losses. Staying steady matters more than chasing spikes, with lasting results built on consistency rather than luck.

- Making Emotional Financial Decisions: When fear takes over, choices tend to go sideways. Sometimes people rush into moves when prices climb, carried by excitement instead of logic. A shaky market can push even careful investors toward rash exits. Instead of steady thinking, emotions take the wheel – leading to purchases at peaks and sales at lows. Over time, that pattern chips away at growth without anyone noticing. What feels right in the moment often works against lasting results.

- Not Setting Clear Money Goals: Most folks save without knowing why. When targets like buying a house or planning for later years aren’t set, effort fades fast. Picture what matters – suddenly each choice has weight. Sticking to limits becomes easier once purpose shows up. Goals shape habits more than willpower ever does.

- Failing to Check Finances Often: Life shifts – so should your money choices. Some folks lock in a budget then walk away forever. When pay changes, when kids arrive, when dreams shift – it matters. Checking things every so often reveals what’s missing. Tweaking steps keeps actions tied to today’s reality. Outdated plans drift from real needs.

- Living Off One Pay check: One pay check might not be enough when times get tough. When work dries up or markets shift, budgets often take a hit. Spreading earnings across different sources tends to soften those blows. Having more than just employment helps stabilize what comes in.

- Neglecting Retirement Planning: Most people focus on today’s bills instead of saving for old age. Wait too long, then every dollar saved must do more heavy lifting down the road. Begin sooner – time turns small amounts into substantial sums through steady growth, easing strain when working years end.

- Taking Financial Advice from Unverified Sources: Out there, social chatter spreads shaky money claims fast. When guesses pass as facts, choices go sideways – losses pile up quiet and quick. Trusted experts, solid reports – they keep things grounded before moves are made.

- Focusing Only on Returns While Overlooking Risk: Most people pick investments just for big gains. Yet risk tags along with each choice, tied to what someone hopes to achieve and how much uncertainty feels okay. When risk gets overlooked, tough times in markets might wipe out money fast.

- Waiting for the Perfect Time: Most folks wait until things feel just right before they save, invest, buy coverage, or clear what they owe. Yet gains in money matters come less from timing and more from sticking with habits over time. When holding back becomes routine, chances slip away, growth slows down.

Real-Life Examples of Key Personal Finance Rules in Action

Example 1: The Early Investor- Rahul began investing ₹3,000 per month via SIPs at the age of 25. Although the quantity appeared to be tiny at first, he maintained consistency for many years. He built up a sizable financial portfolio by avoiding frequent withdrawals and allowing compounding to occur. His meticulous approach reveals how starting early is frequently more important than investing large amounts later. Time became his greatest financial advantage.

Example 2: The Emergency Fund Saver- Priya saved steadily until she had enough set aside to cover half a year of living costs. Once news came that jobs were being cut, she kept up with bills using only what she’d stored away – no borrowing needed. With money already in place, looking for work happened at a slower pace, skipping rushed decisions. Having space like that eased pressure while keeping bigger plans intact.

Example 3: The Debt-Free Professional- Years went by before Amit noticed what those cards really cost him. Only then did he start tackling the balances with real effort. Cutting back here, shifting payments there – slow progress at first. Two full turns of the calendar passed like that. Once free, he slipped that old payment amount into savings and funds instead. His numbers looked stronger ever since.

Example 4: The Financially Protected Family- After kids came along, Neha and her partner got solid health and life coverage. When an unexpected illness hit, hospital bills piled up fast – yet the policy handled nearly all of it. Money in the bank stayed untouched. Instead of borrowing under pressure, they kept moving forward without debt dragging them down. That safety net made sure dreams didn’t get derailed by crisis.

Conclusion

Most people think money management is hard, yet simplicity often works better. These basic rules build a steady base for security and lasting growth. Live below your income while keeping savings ready for surprises. Pay off high-cost loans before they grow, since delays cost more later. Put aside money regularly even if amounts seem small at first. Coverage matters too – unexpected events hit harder without protection. Goals shape choices when plans feel unclear or motivation fades. True change takes patience, yet steady effort slowly builds real progress. Starting today means reaching that stable, clearer financial path faster. Midnight thoughts become daytime wins when steps add up.

FAQs

Q1: What are the Essential Personal Finance Rules?

Key Personal Finance Rules are essential financial concepts that help people manage their money wisely, eliminate financial risks, and accumulate long-term wealth. These guidelines address budgeting, saving, investing, debt management, insurance, and financial planning.

Q2: Why is having an emergency fund important?

An emergency fund allows you to meet unforeseen expenses like medical emergencies, job loss, or essential repairs without relying on loans or credit cards. It provides financial security and alleviates worry during difficult times.

Q3: What percentage of my income should I save?

The appropriate savings rate varies depending on your financial objectives and responsibilities, but most experts advocate saving at least 20% of your income whenever possible. Higher savings rates can hasten wealth accumulation and provide financial flexibility.

Q4: Should I pay off my debt before investing?

High-interest debt should be prioritized because the interest expense frequently outweighs possible investment gains. Once you’ve paid down your high-interest debt, you can invest more actively for the future.

Q5: Why is insurance so important in personal finances?

Insurance protects your finances from unforeseen catastrophes that would otherwise result in major financial problems. Adequate health and life insurance coverage protects savings and promotes long-term financial stability.

Q6: When should I begin investing?

The optimum time to start investing is as early as possible because compounding works better with time. Even little, regular investments can increase significantly with enough time.

Disclaimer

This article exists to inform and teach. Not meant as guidance on money matters, investing, taxes, coverage, or laws. Each person must weigh their own situation, aims, future needs before deciding what to do next. Markets shift – so too can outcomes of investments, without promise of gain or loss. Before taking big money steps, get advice from someone trained in finance. This writer and the company putting it out won’t cover losses if things go wrong using these ideas.