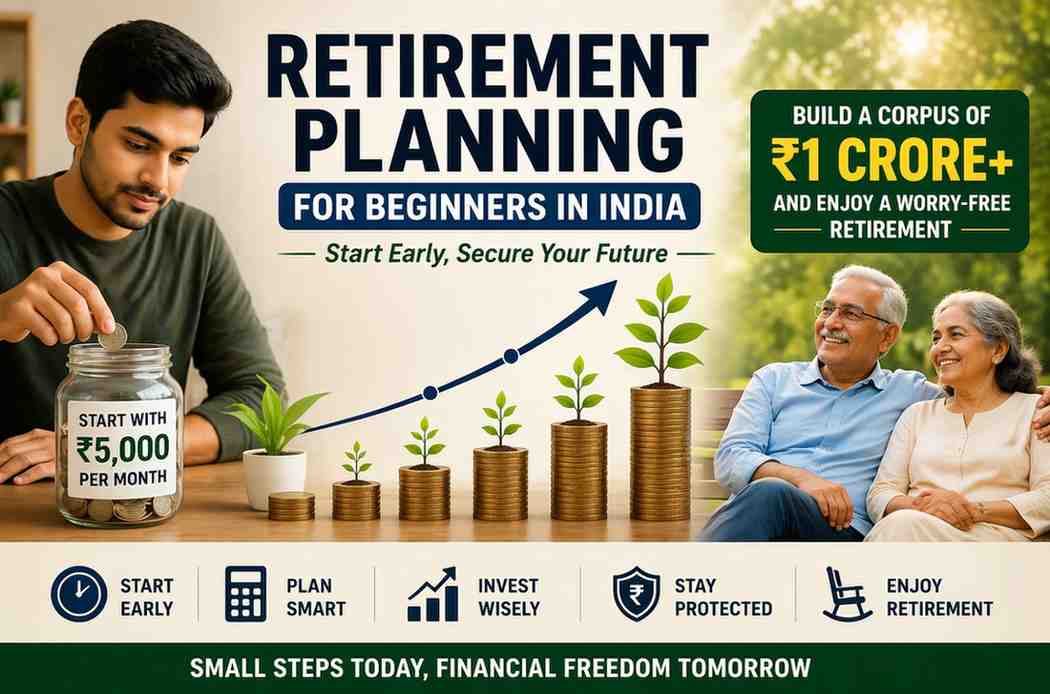

Retirement planning for beginners in India made simple. Learn 9 powerful steps to start with ₹5,000, avoid costly mistakes, and build a secure financial future. retirement planning for beginners in India, how to start retirement planning in India, retirement planning steps India, retirement savings India guide, retirement corpus India.

Introduction

Retirement planning for beginners in India is often ignored because it feels distant, complicated, and unnecessary in the early years of earning.

Later feels safer to many once pay checks rise, yet waiting chips away at what could be theirs down the road. Truth shifts the lens earnings matter less than how soon you step in and keep moving. Five thousand rupees monthly, tucked into smart choices, swells quietly across years. With prices climbing steadily, medical bills piling higher, lives stretching longer, stepping off the work treadmill without savings slips from dream toward danger. To stay updated with financial regulations and safety guidelines, checking information directly on the Reserve Bank of India official website helps you make informed and secure financial decisions. Most folks stumble through life without a clear roadmap, leaning on family or giving up what they love. Not having enough set aside can mean trading independence for help later. Picture staying in charge of your days, your choices, your peace – retirement prep makes that possible. Instead of drowning in jargon, here you get straightforward moves anyone can follow. Step by step, it clears the fog so starting out feels natural, not scary.

Why Retirement Planning Feels Confusing (But Shouldn’t Be)

Starting at the wrong place makes retirement planning seem messy. With so many choices – EPF, NPS, mutual funds, PPF, annuities – it’s easy to think you need a finance degree just to begin. Too much detail slows decisions down; pauses grow into waiting, then years pass. The mind often picks today’s wants – new gadgets, trips, monthly payments – over tomorrow’s safety. Even when distant, retirement shapes your future more than most moves you make. Take words like compounding, asset allocation, or inflation – they might seem tangled at first. Yet after a closer look, their meaning clears up fast. Simple ideas hide behind confusing labels. Once you get them, they make sense quickly. For example, understanding the power of compounding in wealth creation can completely shift how you approach investing. Some people still count on old ideas – like help from relatives or government payouts – that might fall short later. With folks living longer, leaving work could mean twenty years or more without income. That stretch demands personal preparation, not just hope. Reality check: setting up for retirement does not need confusion. Clear goals matter most, along with steady habits and an organized path forward. Slice it into small actions, then handling it feels less heavy, even normal. Anyone can do it when the pieces make sense.

What Happens If You Don’t Start Early

Later moves on retirement prep ripple further than most guess. Missing early momentum strips away growth power over decades. Begin down the path slowly, funds miss stretch years where numbers multiply quietly. A smaller sum set aside earlier might beat heavier payments started past middle age. Picture this: twenty-five brings small deposits that outpace forty-year starts needing much steeper money pushes. Time alone creates this gap. People who begin later wrestle money troubles, fewer choices day to day, yet rely more on others when older. Medical bills weigh heavy, particularly in India as prices climb fast each year. Worry follows shaky finances, dragging down health over time. That tension sticks around longer than expected. Understanding risks like longevity risk in India where retirement may last over 30 years without salary highlights why early planning is critical. Later beginnings cut down on options, forcing people toward riskier moves just to catch up. Because they begin sooner, some enjoy room to adjust, fewer surprises, a calmer outlook. It takes less energy to act now than pay what waiting demands later.

Step 1: Define Your Retirement Goal Clearly

The first step in retirement planning for beginners in India is defining your retirement goal with clarity and realism. Most people start saving without knowing why they save. Yet, picture this: retirement means freedom to live as you wish – minus money worries. Think hard on when you’d leave work behind. Then, what kind of days follow? Quiet routines may call some, while others dream of long trips or diving into passions. A few even see helping loved ones as part of their future rhythm. Figuring out how much money you need each month when retired matters – think rent, meals, doctor visits, fun stuff too. Over years, prices rise, so today’s costs won’t match tomorrow’s reality. Skip factoring that in, and numbers fall short, causing stress down the road. Having a solid idea of what retirement looks like gives direction, shaping where you put your money now. Sticking to that picture keeps choices steady, even when distractions pop up. Should you know exactly what you aim for, money choices naturally fit where life is headed. With that kind of vision, second-guessing fades – sure footing grows under each step forward.

Step 2: Calculate Your Retirement Corpus

After setting a clear goal, figure out how much money you will need to cover life in retirement. Because costs rise over time, what you spend each month now won’t stay the same. Since lifespan varies, planning must account for how long retirement might last. When estimates fall short, trouble often follows down the road. A structured approach like understanding how to calculate retirement corpus in India helps you set a realistic financial target. Most people forget medical bills when they think ahead. Yet surprise events often cost more than expected. Comfort later depends on choices made now – choices that go beyond just survival stuff. Picture waking up knowing each dollar has a job. Uncertainty shrinks once numbers get real. A shaky guess still beats staring into empty space. Direction appears even if details stay fuzzy. What matters? Seeing patterns before money vanishes. Referring to official financial literacy resources and calculators available on the Reserve Bank of India financial education section can further improve your planning accuracy. Additionally, it enables you to modify your plan according to your income and financial objectives. You won’t experience financial strain in retirement if you have a well-calculated corpus.

Step 3: Start Early Even with ₹5,000

Starting early is one of the most powerful advantages in retirement planning for beginners in India. Most folks think big money’s needed right away, yet just five thousand rupees monthly might grow into something solid years ahead. Sticking with it matters more than timing, since steady deposits let gains multiply quietly over months and decades. Hesitating until things feel ideal? That hesitation chips away at what could’ve been yours. Tiny steps early on shape habits without pressure, slowly opening doors to larger amounts when ready. Later on, once paychecks get bigger, putting more into investments feels easier. Because of that, stress stays low and sticking with it becomes natural. Those who begin early gain room to adjust, even trying bolder moves if they see a chance. Little amounts add up differently when years are on their side. Jumping in quickly, before doubts pile up, turns out to matter most.

Step 4: Choose the Right Investment Options

Start smart when picking investments for your future. For salaried individuals, tracking provident fund contributions regularly is important, and you can verify your savings through the EPFO member portal for PF balance and account details. Across India, people lean on tools such as EPF, NPS, mutual funds, or PPF to mix it up wisely. Stability comes through EPF – perfect if you earn a salary. Growth tied to markets shows up in NPS, along with breaks on taxes. Before investing, reviewing scheme structure and benefits on the PFRDA official website for National Pension System details can help you make better long-term decisions. Keeping track of contributions through this step-by-step EPF balance checking guide ensures transparency and awareness of your savings. Equity funds work best when you plan ahead, whereas PPF keeps money secure with steady gains. Instead of putting everything in one place, spreading it out lowers danger and lifts results. What fits your wallet ties back to how much risk feels right, how old you are, how far off your targets stand. Mixing things just enough brings steadiness along with room to climb. Check in now and then, tweak what needs it so nothing drifts too far from where it should be.

Step 5: Understand Compounding and Time

Money grows faster when gains build on top of past gains. Staying in the game long term makes each dollar work harder. Over years, growth stacks up without extra effort. Waiting just a few months might cost thousands later. Time turns quiet progress into big results. Most folks overlook how quiet progress beats quick wins when saving for later years. Patience turns small steps into big results because gains build on top of gains over months that stretch into decades. Money grows best when left alone, doing its thing without interference. Starting sooner means each dollar gets extra seasons to multiply itself quietly behind the scenes. Slow, steady choices today shape what tomorrows feel like much more than sudden moves ever could.

Step 6: Increase Investments Gradually

Little by little, putting more into investments when earnings rise keeps pace with rising prices and personal targets. Each year, adding just a bit extra stacks up noticeably down the road. It works because pressure on daily spending stays low. Over months, raising investment slowly grows future savings while keeping life much the same. When life changes, so should your money moves. Staying on track means matching today’s choices with tomorrow’s goals. As earnings go up, shifting more into investments pays off faster. Small boosts add up, thanks to steady gains building on themselves. Flexing your strategy keeps progress strong.

Step 7: Plan for Retirement Income

Most folks save without thinking ahead to when they stop working. Yet pulling income later matters just as much as stashing cash now. Some fixate on building balances but pay little mind to what comes next. Using savings wisely becomes key once regular pay checks end. A structured approach like using SWP for retirement planning helps convert your investments into a steady income stream. Most people find their money stretches further when they plan ahead. Because income needs are mapped out early, surprises happen less often. Independence stays intact, simply by thinking ahead today. Funds move steadily over time, avoiding sudden drops later. Without this move, comfort in later years could fade fast.

Step 8: Avoid Common Mistakes

Stopping missteps matters just as much as picking winning trades. Late beginnings trip people up, so does forgetting how prices climb over time – savings alone rarely keep pace. Pulling money out too soon? That breaks the momentum needed for steady gains. Recognizing common retirement errors that could wreck your future helps you avoid costly decisions. Emotional investing, lack of diversification, and poor financial discipline can also affect outcomes. A stronger and more robust plan can be created by learning from these errors. Error prevention saves worry, money, and time.

Step 9: Take Action Immediately

Beginners in India often freeze at the start – doing something matters more than knowing everything. Action beats endless preparation every time. A big salary? Not required. High confidence? Skip it. Even tiny steps push things forward. Without movement, plans stay empty. First moves count strongest. Later you start, smaller your gains grow. Doing something now shapes habits, strengthens resolve – both needed down the road. Staying steady beats occasional bursts of effort. Begin at once, let time multiply what you build. Move forward, turn ideas into outcomes, protect what comes next.

Where Most People Go Wrong

Some people mess up when they choose quick pleasures ahead of lasting money safety. When spending rises with pay, less cash flows into future growth. Relying just on a savings account misses gains because it often trails rising prices. Not knowing how money works can steer choices off course, leaving openings untouched. Most people lose money when fear drives choices, like dumping stocks fast or copying hot fads. Sticking to old habits without checking progress slowly breaks down success chances. Skipping variety in investments opens the door to bigger losses while shaking confidence. Clear eyes on common errors make saving smarter over time.

REAL LIFE EXAMPLES

Example 1: Early Starter Advantage

One day, a person aged twenty five begins putting away five thousand rupees monthly into mutual funds. Each new year, they lift that sum by ten percent without fail. Thirty years pass like seasons turning one after another. Slow gains gather quietly beneath steady effort. Numbers grow not because of luck but through repetition. More than salary size, it is duration that shapes outcome. Returns stay ordinary yet results surprise many. Money multiplies when left undisturbed over decades. Patience becomes the quiet engine behind large numbers. This person feels lighter money stress since saving happens slowly over many years. Because they begin sooner, room to adjust grows, fewer big dangers show up, trust in handling cash deepens along the way.

Example 2: Late Starter Pressure

A person working full time waits until age thirty five before thinking about life after work. Because of monthly bills and loan payments piling up, saving feels impossible back then. Only later does it become clear that setting aside fifteen thousand to twenty thousand rupees every month is necessary. That kind of amount pressures the budget now, leaving less for everyday needs. Cutting back on spending today becomes unavoidable. To make up for lost time, riskier choices in investing might be needed instead of safer ones. Without enough time, gains shrink fast, turning progress into a grind. That case proves waiting only piles on work and tension.

Example 3: Mid-Life Catch-Up Strategy

One day, a person at age forty notices their savings won’t cover retirement. Because of that, they start putting money into stock-based mutual funds along with the NPS without waiting any longer. Even though earlier moves would have helped more, sticking to regular investments makes a difference over time. Cutting back on nonessential spending adds up slowly but steadily. To give themselves extra room, they choose to work past the usual retirement point. What happens next proves progress is possible when effort stays steady, no matter how late it begins.

Example 4: Wrong Approach (Savings Only)

A person in their 30s would rather save money in a bank account than make investments. Their savings gradually increase over time, but inflation lowers the actual value of money. They discover after 20 years that their savings are insufficient to cover future costs. Wealth creation is constrained by a lack of investment exposure. This illustration shows that retirement planning requires more than just saving. To overcome inflation and reach financial objectives, investing is essential.

Final Thoughts

Retirement planning for beginners in India is not about complexity but about discipline, consistency, and clarity. Later on, starting now opens doors nothing else can match. Tiny moves today, tied to years ahead, grow into something strong. What matters most? Doing something right now instead of holding back until everything feels ready. Step-by-step choices, made wisely over time, shape how free you feel with money down the road. Each little thing done at present weaves tighter safety nets for days yet to come.

Conclusion

Later on, how you live depends heavily on choices made today about money. Begin now, no matter the sum put aside – it adds up when done regularly over time. A clear plan shapes better outcomes than hoping things work out fine. Picking suitable options matters just as much as skipping errors others repeat often. Staying steady through changes makes all the difference down the road. One foot in front of the other, that is how distance shrinks toward money peace. Missed chances live in yesterday – right now holds what comes next.

FAQs

Q1: How much should beginners invest for retirement in India?

Any amount that a beginner can regularly invest, even ₹5,000 a month, can be their starting point. Growing contributions over time contributes to the development of a substantial retirement corpus.

Q2: In India, what is the greatest option for retirement planning?

A balanced strategy is offered by combining PPF, mutual funds, NPS, and EPF. Your risk tolerance and financial objectives will determine the best mix.

Q3: At 30 or 40, is it too late to begin planning for retirement?

Although it’s never too late, getting started early yields greater outcomes. To succeed, late starters require larger investments and meticulous planning.

Q4: What effect does inflation have on retirement planning?

Over time, inflation lowers money’s purchasing power, raising future costs. Ignoring inflation can result in retirement funds that are insufficient.

Q5: Can I use modest investments to retire early?

Yes, but it calls for self-control, steady investing, and gradually increasing contributions. Early retirement is possible if you start early.

Disclaimer

This piece shares information, not guidance about money choices. Each person must decide using their own aims, comfort with risk, their earnings too. What happens in markets can shift, influencing outcomes over time. Speaking with a qualified expert helps shape better steps ahead. History shows what happened before cannot promise what comes next.