Compare Target Maturity Funds vs FD in detail. Learn about returns, taxation, liquidity, inflation impact, safety, and risks before choosing the right investment option. target maturity funds vs fd, target maturity fund comparison, fd vs target maturity fund, debt mutual funds vs fixed deposits, target maturity funds explained, fixed income investing India, safer investment options India, bond investing India, low risk investments India, target maturity fund taxation, fixed deposit alternatives.

Introduction

Most people saving money in India now look at Target Maturity Funds instead of just sticking to regular Fixed Deposits. Because prices go up faster, banks change their pay rates often, and tax laws shift without warning, some begin questioning if parking cash only in bank deposits still makes sense over time. Even though TMFs and FDs sit on the safer end of investing when stacked against stocks, their behavior isn’t much alike. Fixed deposits hold steady with predictable gains. Bond market access comes through TMFs, which wiggle a bit in value but might outperform now and then. Before putting away earnings, knowing how each option handles risk, gains, taxes, access to funds, and personal fit matters a lot. Picking poorly might hurt profits while shaking future stability too.

What Are Target Maturity Funds?

Holding bonds until they finish around a set date is what Target Maturity Funds do. Most of these passive debt funds pick government papers, loans backed by states, bonds from public sector units, along with other stable interest-paying assets. Instead of shifting holdings often like active debt funds, their path stays steady – bought once, kept till near the chosen year. A fixed time frame shapes how everything fits together inside them. A bond fund aimed at a 2031 payoff date mostly picks securities that also wrap up around then. When the clock ticks nearer to 2031, swings in rates tend to shake things less. Sticking with it until the finish line means results are somewhat clearer down the road. Retail investors exploring debt mutual funds and bond-based investment categories can also refer to the AMFI India official website for additional investor education resources.

One reason people lean toward TMFs? They bundle many strong bonds into just one buy. Not stuck with only what a bank deposit offers – access spreads across several solid debt options. Choosing these funds often means stepping into the bond world without buying each note by hand. Still, TMFs move with the market. Every day, their value shifts when bond yields or rates change. When drops happen, people rushing out might miss what these funds can do. What seems like a loss at first could turn different later. Investors looking to understand how fixed-income investing is evolving in India may also find The Powerful Future of Bond Investing in India useful while exploring debt-market opportunities.

What Is a Fixed Deposit (FD)?

A set amount sits untouched for months or years when someone chooses a fixed deposit. Banks across India provide this option, popular because numbers add up predictably. Money grows steadily thanks to an agreed-upon interest level locked at start. Knowing the end figure helps map out future spending without guessing. Most folks near retirement pick fixed deposits simply because they sleep better knowing their money won’t drop overnight. Stability over months or years gives a quiet kind of confidence that stocks rarely offer. Instead of watching numbers bounce around, some choose calm – even if it means slower growth. The balance stays put unless touched, which feels safer when life needs fewer surprises. Not everyone chases big wins; peace matters just as much.

Beyond safety, fixed deposits keep things clear. Jumping into bonds or tracking net asset value swings? Not required here. Picking how long to save, then setting money aside – effortless. That ease opens doors for those just starting out. Still, fixed deposits come with downsides many miss. The interest they generate gets taxed based on how much you earn each year. Over years, rising prices eat into actual gains – more so if your tax rate climbs higher. Withdrawals before maturity can bring penalties or shrink interest gains. Given such rules, plenty choose to weigh FDs against different low-risk income options today. Many conservative investors compare bank deposits to long-term savings plans such as PPF. comparison available in PPF vs FD Which Is Safe in 2025? shows how different low-risk investments behave under changing economic conditions.

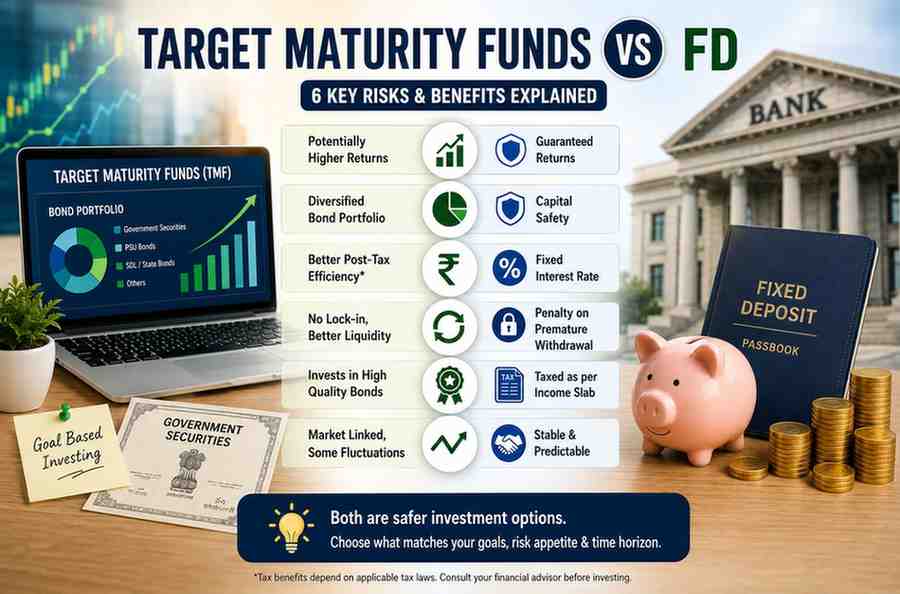

Target Maturity Funds vs FD: 6 Key Risks and Benefits Explained

1. Return Potential and Growth Opportunity

Most people notice the gain chance first when comparing Target Maturity Funds to Fixed Deposits. Locked rates define FD earnings right from day one. Stability shows up here clearly – though markets might surge later, those jumps stay out of reach. Growth stays capped, even when conditions turn favourable down the line. When rates drop following a purchase, bond values might go up – that could lift TMF performance. These funds tend to move alongside shifts in the bond marketplace. Over moderate or extended periods, results may turn out stronger than expected.

Still, bigger gains often bring some ups and downs. Unlike fixed deposits, TMF doesn’t promise set returns. When rates shift badly, these funds might dip for a while – knowing this matters. Value can drop, even if just short term. Interest-rate cycles play a major role in fixed-income investments. Many investors exploring debt opportunities are also evaluating bond-market timing through Best Time to Invest in Bonds India: Why 2025 Is the Ideal Opportunity while planning long-term allocations.

2. Safety and Capital Stability

Most people see fixed deposits as less risky, given the promise of a set pay out at the end. Without day-to-day changes showing on screen, money seems more stable. That steady look helps ease worries over time. Some days, bond values shift due to changing rates – so TMFs reflect those small swings right away. Even steady holdings might jitter briefly on screen when the market breathes wrong.

Government-backed tools make up most of a typical TMF’s holdings, along with state-owned company bonds plus state development loans – these usually carry less danger than weaker corporate borrowing. Still, zero risk does not exist here. Frozen desserts hide downsides too – think shrinking value from rising prices, trouble putting money back to work later. When people fixate on safe gains, they often miss the slow hit to what their cash can buy over years.

3. Taxation Differences

Heavy earners might keep less after taxes with f d s since interest gets added to income. Target maturity fund earnings often face lower cuts in pocket terms. What you actually gain depends on how tax rules apply. Full interest from fixed deposits counts as regular income. That part matters a lot if rates push you into a costlier bracket. When you invest in TMFs, the tax treatment follows whatever rules apply to debt funds during that period. Redemption happens under those same conditions. Rules in place when money moves matter most. Investors wanting official regulatory updates related to mutual funds, disclosures, and taxation frameworks can also check the SEBI official website for updated guidelines.

Even if tax laws around debt funds shifted lately, certain people might see TMFs work better – especially when timing or personal finances play a role. Most people overlook tax effects when investing. Looking just at surface-level gains, yet ignoring what you keep after taxes, paints an inaccurate picture of real financial progress.

4. Liquidity and Flexibility

What sets TMFs apart from FDs? Liquidity plays a big role. Withdraw money early from a fixed deposit, face penalties. Pull out before time ends, what you earn in interest drops. Most of the time, getting money out is easier with TMFs since they skip those usual long-term holds. Trading on exchanges helps some TMF types move faster when sold. Still, that freedom ties to how markets perform. When investors pull out amid weak market moments, what they get back might fall short of what they hoped for.

Liquidity needs careful handling when shaping an investment mix that holds steady. A well-structured portfolio depends on how fluid assets stay during setup. Many investors planning emergency allocation strategies also explore 5 Proven Ways to Master How to Balance Liquidity and Returns in Investing while structuring safer financial plans.

5. Inflation Impact

Inflation slowly erodes purchasing power over time. An FD with 6.5% rates may appear appealing, but real wealth building can be limited after accounting for taxes and inflation. TMFs may give substantially superior inflation-adjusted outcomes in some interest-rate situations, as bond-market participation can enhance overall efficiency over time. However, investors should avoid setting false expectations. TMFs are debt-oriented investments that aim for stability and moderate growth rather than aggressive wealth multiplication, as equities do. Long-term investors must determine if their investing plan preserves real buying power or generates simply nominal profits.

6. Predictability vs Market-Linked Volatility

Most families across India stick with fixed deposits because the returns are clear from day one. Knowing the exact amount due at maturity helps people organize their money without worry. That steady outcome beats guesswork every time. Clarity like that? It keeps drawing savers back, again and again. Still, TMFs spread risk while possibly running smoother, yet they bob up and down with the market for stretches. When bond markets wiggle normally, some investors brace hard if dips rattle them. What drives the choice comes down to how investors feel. Stability matters most to certain people, yet some welcome small ups and downs when they expect stronger results and room to adapt.

Who Should Consider Target Maturity Funds?

Target Maturity Funds may be suitable for investors who are fine with mild market fluctuations and seek diversified exposure to fixed-income assets. Investors with medium-to-long investment horizons profit more since staying invested until maturity mitigates the impact of short-term interest rate volatility. TMFs may also appeal to higher-tax-bracket investors looking for potential post-tax benefits above ordinary deposits. Investors who understand debt-market dynamics and can be patient throughout transitory NAV drops are typically better suited to these instruments.

TMFs may also be advantageous for goal-oriented investors planning for future expenses such as children’s education, retirement, or property purchase if the maturity timeframe coincides with their financial objectives. However, TMFs are not appropriate for investors expecting absolute certainty or guaranteed returns. Before investing in any market-linked loan product, ensure that you are emotionally comfortable with minor changes.

Who Should Prefer Fixed Deposits?

Most people who dislike risk lean toward Fixed Deposits – they want peace of mind, clear outcomes, otherwise skip the chase for big gains. Those living off savings, especially older adults relying on steady money each month, find comfort here since what they get back never changes, always straightforward to figure out. Bank deposits often ease worries for those uneasy about market swings. When safeguarding money weighs heavier than chasing gains, fixed deposits tend to fit just fine.

Finding calm matters just as much as returns for some people. A sense of safety comes from knowing exactly what you’ll get, without staring at shifting numbers each morning. True, but taxes eat into gains over time. Relying only on fixed deposits might miss the mark when it comes to protecting money’s real value. What feels safe today could lose ground later.

Common Mistakes Investors Make

- Assume TMFs are completely risk-free: Many investors believe that Target Maturity Funds operate in the same way as Fixed Deposits do. In actuality, TMFs are market-linked debt securities with NAVs that change in response to interest rate fluctuations.

- Ignoring post-tax returns: Investors frequently compare simply headline returns, neglecting taxes. This can lead to erroneous expectations for long-term wealth accumulation.

- Selecting Products Without Matching Goals: Investing in long-term TMFs for short-term financial reasons can result in excessive liquidity pressure and transient volatility concerns.

- Panic Selling during Volatility: Some investors abandon TMFs amid temporary market downturns induced by higher bond yields. Emotional decisions made during periods of instability may have a negative impact on long-term outcomes.

- Ignoring Inflation’s Impact: Many investors rely solely on promised profits, without considering whether the investment will genuinely preserve purchasing power after taxes and inflation.

Are Target Maturity Funds Better Than FDs?

The target maturity funds vs. fd debate has no clear winner because the two types of investments have different uses. An investor’s objectives, tax bracket, liquidity requirements, investment horizon, and level of emotional comfort with market-linked swings all influence the best choice.

Investors looking for diversity, some flexibility, and possibly greater efficiency over longer periods of time may find Target Maturity Funds more appealing. Bond-market involvement through TMFs may be advantageous for investors who are at ease with transient NAV volatility.

In contrast, investors who value certainty and predictable maturity values continue to find fixed deposits to be extremely desirable. FDs continue to be preferred by many retirees and conservative savers due to their ease of planning and ability to lower financial concern.

Combining the two items can be the best course of action for many investors. While medium-term allocations can be diversified into TMFs for a better balance between stability and efficiency, emergency funds and short-term saves may stay in FDs.

Suitability should take precedence over trends when making investment decisions. Without understanding risk, chasing marginally higher returns might lead to unneeded financial stress down the road.

Real-Life Examples

Example 1: Retired Investor Seeking Stability- After serving in the government for 35 years, Mr. Verma retired and sought total assurance over his retirement funds. He placed the majority of his retirement corpus in fixed deposits because his monthly household costs were mostly dependent on a steady pay check. Although he was aware that inflation might eventually lower real returns, he was more concerned with emotional comfort and steady income flow than with optimizing profits. Because he was uneasy with even brief market swings, FDs were a better fit for his personality and financial objectives.

Example 2: Salaried Professional in Higher Tax Bracket- After taking inflation into account, 34-year-old IT professional Rohit noticed that post-tax FD returns were losing appeal. He investigated Target Maturity Funds, mostly investing in government-backed assets, because his financial objectives were still six to eight years away. Because he felt comfortable staying invested for the long run, he was willing to accept modest NAV volatility. He sought to increase overall portfolio efficiency while keeping comparatively lower risk than stocks by diversifying outside conventional FDs.

Conclusion

Although they serve different client needs, target maturity funds and fixed deposits both have significant roles in financial planning. While TMFs offer diversity and moderately flexible bond-market exposure, FDs offer certainty, simplicity, and emotional comfort. Taxation, liquidity requirements, investment horizon, inflation impact, and risk tolerance are some of the criteria that determine which option is best. Investors should refrain from choosing products solely on the basis of short-term market trends or headline results. Relying solely on one investment category is frequently not as effective as a balanced plan that combines stability and diversification. Investors can make better long-term financial decisions by carefully weighing the advantages and dangers.

FAQs

Q1: Compared to standard debt mutual funds, are Target Maturity Funds safer?

In contrast to lesser-rated debt funds, many TMFs primarily invest in PSU bonds and government-backed securities, which often lessen credit risk. They are not entirely risk-free, though, because they still contain interest-rate-related volatility.

Q2: Is it possible for Target Maturity Funds to provide negative returns?

Indeed, when bond yields climb significantly, TMFs may momentarily produce negative returns. Lower redemption values may be experienced by investors who withdraw during adverse times.

Q3: Are returns on FD guaranteed?

FD returns are typically predetermined at the time of investment and don’t change until the investment matures. Post-tax and inflation-adjusted returns, however, can be very different from what was anticipated.

Q4: What is the best investment for retirees?

Fixed deposits are preferred by many retirees due to their predictable yields and constant maturity value, which lessen financial stress. TMFs may still be used selectively for diversification by certain retirees, nevertheless.

Q5: Can I take money out of TMFs at any time?

The majority of TMFs permit redemption before to maturity; however, the value of the redemption is contingent upon current market circumstances and NAV movement at the time of withdrawal.

Q6: Why are TMFs growing in popularity in India?

In search of greater long-term efficiency, investors are increasingly looking at diversified fixed-income possibilities outside of standard bank deposits, which is why TMFs are growing in popularity.

Disclaimer

This material should not be interpreted as investment advice; it is merely meant to be instructive and informative. Depending on your financial circumstances, investment products such as Fixed Deposits and Target Maturity Funds have varying degrees of risk, taxes, and suitability. Before considering an investment, investors should assess their objectives, risk tolerance, and get advice from a certified financial advisor. Tax laws and financial regulations are subject to change.