What happens if you don’t file ITR for 2 years? Know penalties, notices, refund loss & financial risks. Avoid costly mistakes with this guide. what happens if you don’t file itr for 2 years, itr not filed consequences, penalty for not filing itr india, income tax notice india, late itr filing rules, itr after due date, itr penalty section 234f.

Introduction: What Happens If You Don’t File ITR for 2 Years

One time you did not file your income tax return. Still another year went by without a message or alert of any kind. Now it seems like sending that form might be up to you, perhaps even unnecessary. That thought – the idea that silence means permission – starts the trouble. If you are searching what happens if you don’t file ITR for 2 years, it means you are already in a risky zone where consequences may not be visible yet but are silently building. Later on, missing deadlines quietly builds pressure instead of instant consequences. A tiny slip now might grow into fines, official warnings, damaged trust with lenders, and deeper money problems down the road. These ripple effects touch refund claims, borrowing power, and how institutions see your financial behaviour over time.

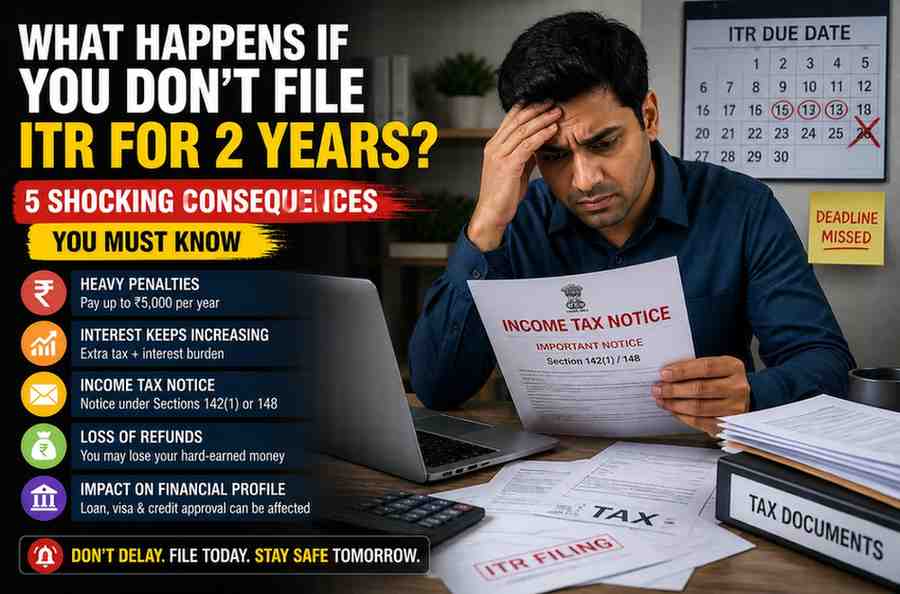

1. Late Filing Penalty Can Hit You Hard

Most folks miss the deadline without thinking twice – then discover the hit comes fast: Section 234F slaps a fee for late returns. At first glance, the number seems tiny; keep ignoring it yearly and it piles into real money. Earn more than ₹5 lakh? That’s five grand each time they tag you. Fall short of that mark, yet still owe something just for turning it in late. Stretch this habit over two filings and suddenly you’re handing out cash for no reason at all. Some think once the fine hits, that’s the end – but actually, it’s just the opener in a longer sequence. Later it gets, worse things turn out. Spotting what built up happens most times once someone jumps into sorting old paperwork. You can reduce such risks by understanding how to avoid income tax penalties in 2025 and staying compliant from the beginning. Missing due dates shows you’re out of step, yet this often opens the door to closer checks. Though silence might follow at first, the record still marks when filings don’t arrive. As missed steps pile up, they form a trail – more serious than any one slip. Handing things in late just once? That’s misstep territory. But skipping two full years? Now it reads like caution tape. So fines aren’t minor costs – they’re echoes pointing toward what could come next.

2. Interest on Unpaid Tax Keeps Increasing

Should tax be owed without a return filed, the clock begins ticking right away. On top of the base amount, charges pile up each month through rules found in sections 234A, 234B, and 234C. Hidden growth happens behind the scenes – interest builds even when ignored. Over months, what seemed minor swells into something far heavier because of how numbers fold into themselves. Filing late? Some think only the initial sum matters. Truth is, the bill often includes much more than expected. Paying interest might seem like getting punished all over again. Things get trickier if your money comes from wages, freelance work, or investment profits – especially when taxes already took a piece earlier. Understanding how tax liabilities are calculated becomes essential, and you can review how to calculate advance tax step-by-step guide to see how these calculations actually work. Later on comes the real cost when delays turn small duties into bigger problems. Missing the moment to file lets money worries build up slowly behind the scenes. What seems minor today could twist tomorrow’s budget without warning. Step by step, those unpaid amounts start tugging at your monthly balance. Every extra week stretches what you’ll eventually owe. Pushing back deadlines quietly reshapes how much control you keep over personal funds. Facing it early means fewer shocks down the road.

3. Income Tax Notice Can Be Issued Anytime

Receiving a warning from the tax authority is one of the most dire repercussions of failing to file an ITR for two years. The Income Tax Department India uses advanced data tracking systems that monitor your financial activity, including bank transactions, TDS records, high-value purchases, and investment patterns. Most times, money details still get shared even when no return is sent. Should numbers mismatch what’s on record versus official filings, alarms go off in the system. Flags pop up that may trigger scrutiny under rules such as 142(1) or 148, asking for clarification on earnings and payments. A sudden letter like this often brings urgency since answers must come fast – delays aren’t an option. Panic hits some people here – missing documents or unclear transaction history fuels it. Stress deepens if old tax filings pile up untouched. You can understand how these situations escalate by reviewing income tax demand notice explained and the actions required in such cases. Most notices happen because information does not match up. When filings get skipped, mismatch chances go up. A notice already sent means effort, paperwork, even expert help might be needed. Fixing things early beats scrambling after warnings appear. Late corrections take more energy than staying on track from the start.

4. You Lose Refunds Permanently

Most folks miss out on tax refunds more than they think. Should too much tax come off via TDS, filing an ITR on time locks in recovery chances. Miss the window? The system won’t save that cash forever. Eventually, what was yours slips away for good. That leftover amount just vanishes – no second chances. Some people who get paid a salary walk right into this mistake thinking their company took care of it all. Yet filing an ITR isn’t skipped even when TDS gets deducted. The refund simply won’t move unless that form goes in. Across twenty four months, those amounts might surprise you. Letting rebates slip isn’t only losing cash, it shows gaps in how money matters are tracked. Money meant to return might vanish if waiting too long. Sometimes people see the gap only once they choose to submit returns after many years. That delay blocks access forever. Sending in tax forms does more than meet rules – it grabs value owed directly to you. Over time, skipping this step chips away at savings, often unseen until much later.

5. Your Financial Profile Gets Impacted

Skipping ITR for two years straight chips away at how others see your money habits, quietly but surely. Your bank or lender might ask for tax returns when checking if you’re trustworthy with cash – no paperwork means raised eyebrows. Visa offices look at those documents too, searching for signs you can support yourself abroad. Missing files make everything take longer, sometimes ending in flat refusals without clear reasons given. Real income does not matter much if there is nothing on record to back it up. Gaps speak louder than numbers when trust is the real currency being measured. Banks need real paperwork – guesswork won’t cut it. When chasing a mortgage, loan for yourself, or capital to run a company, that rule hits harder than most expect. You can also see how financial discipline impacts long-term stability through personal finance tasks 2025 essential steps which highlights the importance of consistent documentation. Late filings pile up, quietly chipping away at trust. When returns go missing year after year, questions follow – ones that are tough to answer down the line. More than loan rejections, thin records can block border crossings or scare off potential collaborators. Paper trails matter, especially when proving stability counts. Kept neatly, ITRs become quiet proof of consistency, standing ready when needed.

What Most People Don’t Realize (Important Insight)

Skipping ITR filing isn’t merely late paperwork – this step counts as breaking rules, shaking up how banks see you. Your credit trail takes a hit when returns go missing. Financial reputation wobbles without those filings. Trust built with lenders fades slightly each time nothing arrives. Financial transparency expectations are also aligned with frameworks followed by the Reserve Bank of India in the broader financial ecosystem. Even if you skip filing returns, the system still follows every transaction you make – so your money trail stays visible but unrecorded. That gap? It quietly builds up trouble. Little by little, it opens doors to warnings, fines, or missed chances with finances. Most people wake up to this fact only after a loan gets turned down or tax questions show up out of nowhere. Skipping ITR isn’t merely dodging paperwork – it chips away at your money foundation. Delay stretches problems thin, making fixes harder later. Without regular updates, details slip through cracks since no one tracks them live. That’s when filing turns from rule-following into smart planning by default.

Real-Life Examples

Example 1: Rahul worked a regular job, yet never sent in his income tax return for two full years – figured it wasn’t needed since taxes came out automatically at work. Thinking that covered everything, he carried on without submitting anything. Only when he went to get a house loan did things slow down. The lender wanted proof: tax returns from those past two years. With nothing to show, the request sat frozen, stuck until he could provide what was missing. Later came the revised filings, along with penalty payments, then a stretch of waiting. While time passed, values in real estate climbed – money slipped away because of it.

Example 2: Priya worked alone on projects, earning different amounts each month. Since the money wasn’t steady, she thought taxes didn’t apply to her. Over time, though, numbers in official records did not line up – her bank activity stood out compared to what was reported. A message arrived after twenty-four months, catching her off guard. Finding past receipts took hours; some were lost. Fees piled on top of what she owed, plus added charges that grew daily. Effort stretched beyond just paying – forms, calls, follow-ups filled weeks. Had she filed sooner, most of this would never have happened.

Example 3: Out of nowhere, Amit found too much tax taken from his salary each year. Because he skipped sending income details to the government, nothing came back even if money was owed. Years passed before it hit him – unclaimed cash doesn’t return on its own. Silence cost him funds that might’ve grown through smart choices. His budget felt the gap long after. Then again, delays reshape outcomes more than expected.

Example 4: Starting late on taxes slowed everything down for Neha. Though earning steadily, missing two years of filings left gaps. When officials checked, questions arose about where her money came from. Papers that should have been straightforward turned into hurdles. Instead of packing bags, she scrambled to submit old forms plus fines. Plans already set now hung in uncertainty. Stress built fast when timing fell apart.

Can You File ITR After 2 Years?

Yes, but the procedure gets trickier. ITR-U, which permits rectification of previous filings within a certain time frame, may be required if you need to file an amended return. Waiting too long makes things harder. Taxes might cost more, plus there could be fines. After twenty four months, rules tighten up. Getting paperwork right matters a lot now. Numbers must add up without mistakes. Maybe an expert should step in. Time passes. Choices shrink. Fewer paths stay open. Fixing real errors is what updated filings are for, yet treating them like a routine fix misses the point entirely. That habit of waiting till the last moment? It falls apart under pressure. You can understand the process better through how to file ITR-U online in 2025 which explains the steps involved. While filing beyond the deadline may resolve compliance problems, it also raises costs. Filing on time is usually preferable to relying on remedial measures afterward.

Is It Illegal to Not File ITR?

Skipping ITR isn’t automatically against the rules – unless you were supposed to submit one and didn’t. When earnings go beyond the tax-free threshold or match specific criteria, sending a return turns compulsory. Falling short here might bring fines or official consequences. Staying clear of trouble mostly means following steps set by authorities – not dodging penalties. Still, doing this more than once pushes minor slips toward heavier outcomes. Sometimes making less than the threshold still means sending in a return helps build solid paper trails. When people skip it while also hiding income or lying on forms, that is where penalties start piling up. Knowing what you must do keeps things clear. Sending paperwork each year does more than dodge fines – it shows openness about money matters.

How to Fix This Situation Immediately

Step 1: Review Your Income Details

Looking back at where your money came from over twenty-four months sets the stage – paychecks, client work, even returns from funds tucked away somewhere. Form 26AS or AIS shows if tax was taken out already, so take a close look there next. That step makes it clear: did you owe tax? Was something missed earlier? Fixing gaps comes after knowing that.

Step 2: File Pending Returns

Later filings might need ITR-U instead of standard options. Every number on the form must match what’s already documented somewhere else. Getting it right now means fewer letters later asking questions. Accuracy today blocks confusion tomorrow.

Step 3: Pay Penalties and Interest

Determine the interest and late filing fees that apply under the applicable sections. Paying bills on time maintains your compliance record spotless and stops additional accumulation.

Step 4: Respond to Any Notice Quickly

If you have been notified, reply with the appropriate paperwork within the allotted time. Responses that are delayed may intensify the problem and result in more stringent measures.

Common Mistakes People Make

Mistake 1: Assuming No Notice Means No Problem- Many people believe they are safe if they haven’t gotten a notice. In actuality, the system continuously monitors financial data, and problems can subsequently arise.

Mistake 2: Ignoring TDS Deductions- ITR filing is not replaced by tax deducted at source. Refunds cannot be requested without filing, and records are left unfinished.

Mistake 3: Delaying After Missing One Year- disregarding one year generally results in disregarding the next. This results in a backlog that is more difficult to clear later on and carries heavier fines.

Mistake 4: Not Checking AIS or Form 26AS- When financial data is not verified, there are discrepancies that may result in tax department notices.

Mistake 5: Underestimating Financial Impact- Penalties are often thought of as little, but when interest, lost refunds, and compliance problems are taken into account, the financial cost is increased.

Final Verdict

Skipping tax returns for two years isn’t simply falling behind – each month adds unseen costs. A forgotten due date turns into fines, extra charges pile up, money owed back slips away. Authorities may send warnings without warning. Over time, borrowing gets tougher. So does travel approval. Records start looking shaky. Fixing things late means more paperwork, higher stakes. Dealing with it sooner feels lighter on every level. Policy direction and enforcement continue to evolve under guidance from the Central Board of Direct Taxes which oversees direct tax regulations. Not only is timely ITR filing compliant, but it also protects your finances.

Conclusion

Skipping ITR for two years might look fine at first, yet trouble grows behind the scenes, touching many parts of money matters. Fines pile up, interest adds on, warnings arrive, refunds vanish – these show clearly, whereas hidden problems like damaged trust and rule-breaking risks creep in slowly. Time stretches the gap, turning things harder, pricier to fix. Handing in ITR does more than meet rules; it acts like armour for earnings, reputation, what lies ahead. Right now matters most when handling money paperwork – slipping up leads to messes piling fast. Missed a deadline? Jump on it without delay; fixing things early cuts losses and brings order back quick.

FAQs

Q1: What happens if you don’t file ITR for 2 years?

Penalties, interest on unpaid taxes, and potential notices are all conceivable. Your financial credibility may also be impacted. The whole cost burden is increased by delays.

Q2: Can I file ITR after 2 years?

You can use the updated return options when filing, yes. But there will be extra taxes and fines. Compared to timely submission, it is more complicated.

Q3: Will I undoubtedly receive a notice for failing to file my ITR?

Mismatches in financial data may result in alerts later, though not usually right away. Over time, the risk rises.

Q4: Is filing an ITR required each year?

Your circumstances and income will determine this. For appropriate financial paperwork and compliance, filing is advised.

Q5: What happens if my income is less than the taxable threshold?

Maintaining financial records is aided by filing, even if it may not be legally necessary. Verification and lending both benefit from it.

Q6: If I file later, will I be exempt from penalties?

No, late filings typically result in penalties and interest. Early filing reduces the overall expense.

Disclaimer

Just so you know, this article shares general info and isn’t meant as financial or legal guidance. Rules around taxes can shift – what applies today might not tomorrow. People have different circumstances, so outcomes aren’t guaranteed. It’s wise to check current regulations through trusted channels or talk with someone licensed in tax matters. Decisions made using these words are on each reader, not the writer.