Discover 9 hidden facts about Return of Premium Term Insurance, including costs, benefits, drawbacks, returns, and whether it is worth buying compared to a regular term plan. Return of Premium Term Insurance, Return of Premium Term Plan, Return of Premium Insurance, ROP Term Insurance, Return of Premium vs Regular Term Insurance, Is Return of Premium Term Insurance Worth It, Return of Premium Policy Benefits, Return of Premium Policy Drawbacks, Best Term Insurance Plans India, Term Insurance Comparison.

Introduction

Most folks hesitate to get term insurance since handing over money year after year feels pointless when there’s no pay out upon survival. Seeing this worry, insurers came up with Return of Premium Term Insurance – life coverage that gives qualifying payments back once the term ends. At first glance, it appears ideal: safety net meets cash return. Most people think these plans are straightforward, yet that simplicity tends to vanish under closer inspection. The promise of getting cash back sounds good, though it usually means paying more each month and earning less over time, a trade-off few consider early on. Years pass before some realize the return wasn’t worth what was given up along the way.

Most people overlook what happens if they cancel early. A different kind of term plan gives back payments – but only under strict conditions. Think about whether that promise fits how your household manages money over years. Some find comfort in refunds; others see wasted value elsewhere. What looks like safety might tie up cash needed later. Knowing these details changes how seriously you take each option.

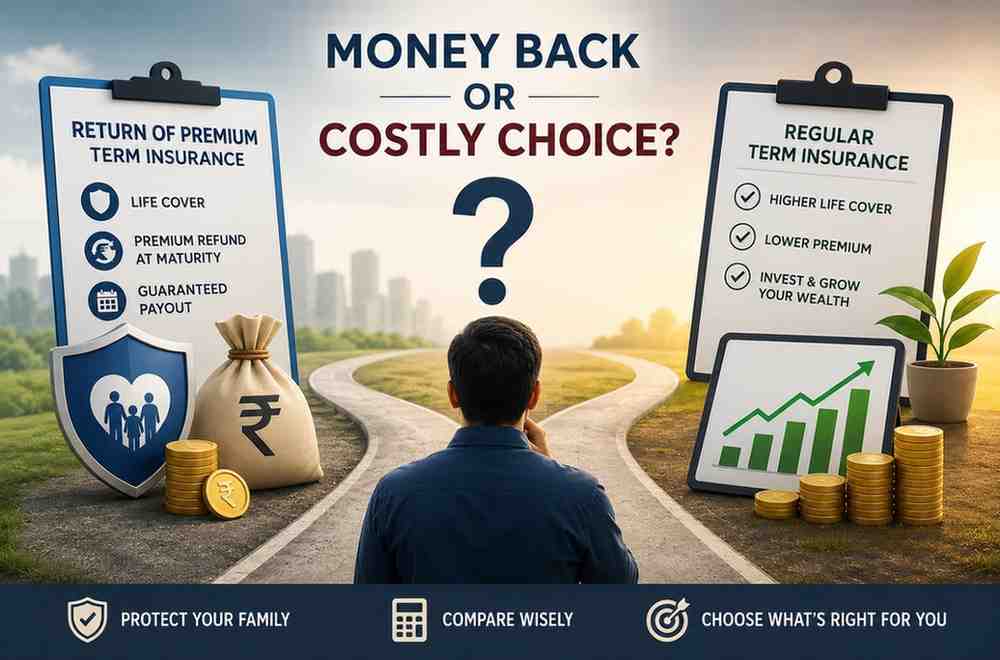

What Is Return of Premium Term Insurance?

Return of Premium Term Insurance, often known as ROP Term Insurance, is a form of life insurance policy that includes both regular term coverage and a maturity bonus. If something happens to you while the coverage runs, your chosen person gets a payout – same as standard plans. Yet should you make it through unharmed, those qualifying payments you made? You get them back.

Most people ignore this unless they hate wasting money on unused coverage. Still, since companies must pay back what’s owed later, costs climb fast compared to basic term options. Readers can verify insurance regulations and consumer protection guidelines through the Insurance Regulatory and Development Authority of India (IRDAI). Even though knowing funds come at the end feels comforting, it is smart to see such plans first as protection – not wealth building.

Hidden Fact #1: You Pay Significantly Higher Premiums

The first surprise most customers face is the expense. Return of Premium Term Insurance is typically priced two to four times higher than a standard term plan with the same coverage level. Because the policyholder might live past the term, refunds are due – that risk pushes the cost up. Premiums go back when survival happens, so pricing adjusts ahead of time. A yearly price for basic term insurance with ₹1 crore protection might run between ₹12,000 and ₹15,000. Yet, choosing one that returns premiums could set you back ₹30,000 to ₹45,000 each year instead. Stretch that gap across three decades, suddenly the extra cost adds up fast.

Surprisingly few think about how much they actually pay each year when chasing a big pay out later. Paying hundreds of thousands extra often ends up funding a return that barely moves the needle on real wealth. Before choosing any policy, determining the appropriate term insurance amount should take priority over focusing on the refund feature.

Hidden Fact #2: The Refund May Be Lower Than Expected

Surprisingly, people often think each rupee paid returns fully. Yet reality tends to differ sharply. Base premiums usually come back under most Return of Premium Term plans. Taxes or extra charges? Left out entirely.

Most times, taxes handed over while paying premiums won’t come back later. When you add extra coverage – like for accidents, serious sickness, or losing your ability to work – the money spent on those parts might vanish when it’s time to collect. So what lands in your hands at the end? Often less than every dollar you ever put in. The full ride of payments doesn’t guarantee equal returns.

Most people feel let down when they get less than expected. That happens because they miss what the contract actually says about refunds. Reading every part closely helps avoid surprises later. Over time, tiny points in the wording add up fast.

Hidden Fact #3: Inflation Can Reduce the Real Value of Your Refund

Years down the line, getting one big payment might seem nice at first glance. Still, rising prices quietly eat away what that money can buy. What feels like a solid number now could feel much smaller decades later. The future value often hides how weak it truly is. Thirty years pass. You’ve paid ten lakh rupees in premiums, every last bit of it. At the end, that same sum comes back to you. Numbers stay unchanged, yet value shrinks – quietly eroded by inflation year after year. Today’s solid return might barely touch tomorrow’s bills. A pay out feeling substantial now often fades into insufficiency later.

That’s the reason money specialists usually look at earnings once inflation has been factored in. The same principle can be observed when examining the inflation impact on ₹1 crore, where inflation gradually erodes wealth despite the nominal amount remaining unchanged. Ignoring inflation may cause buyers to overestimate the true value of the maturity advantage. Industry reports and insurance statistics published by the Insurance Information Bureau of India (IIB) help consumers understand long-term insurance trends and policyholder behaviour.

Hidden Fact #4: The Effective Returns Are Often Modest

Surprisingly few realize they’re treating Return of Premium Term Insurance like a savings plan. Even though getting money back at the end feels rewarding, what you gain rarely matches what was hoped. Money isn’t handed out freely by the insurer. Rather, once the expense of maintaining coverage over time is subtracted, qualifying premiums get sent back. Figuring out the internal rate of return usually leads experts to a number much smaller than gains seen in extended investment periods.

Just because of this doesn’t mean the product fails – instead, a key compromise shows up. Buyers looking for wealth generation may discover better options elsewhere. Understanding the power of compounding demonstrates why many financial planners prefer purchasing a regular term plan and investing the premium difference separately. Separating insurance and investment decisions can provide more flexibility and potentially better long-term outcomes.

Hidden Fact #5: You May End Up Underinsured

Should anything happen to you, insurance helps keep your family safe money-wise. Yet expensive premiums from Return of Premium Term plans usually push people toward smaller policies. A single income could buy twenty million rupees in coverage using standard term insurance, yet just ten million with a return-of-premium plan. When savings are locked into repayment features, the safety net shrinks by half.

Surprisingly few households notice this balance until they dig into the fine print of plans. Getting money returned might sound good – yet solid protection matters more above all. Receiving cash later never justifies risking being underinsured when trouble hits. Understanding why insurance is a smart financial decision reinforces the idea that insurance should first focus on protection rather than returns. Regardless of the maturity advantage, a policy that leaves your family underinsured may fail to serve its primary objective.

Hidden Fact #6: Missing Premium Payments Can Hurt More Than You Think

Most conversations about selling insurance skip right past what happens when someone stops paying. Because these return-of-premium plans cost much more, sticking with one for decades isn’t always realistic. Years go by, life shifts, budgets tighten – suddenly keeping up feels like walking uphill.

One moment your income stops, next you’re skipping a payment. Miss too many, the safety net vanishes – coverage gone, future payout lost. Getting it back? Often means forms piling up, fees appearing, maybe even a doctor’s visit. Wait past the deadline, everything resets like nothing happened.

Most people fixate on refunds when buying insurance, yet rarely think about long-term costs piling up year after year. Facing tough times down the road could make steady payments hard – check if your budget can handle that strain before signing anything.

Hidden Fact #7: Rider Premiums May Not Be Refunded

Some choose extra layers on their policy – like help if sick, hurt, wiped out financially, or unable to work. When life shifts hard, these extras might keep a household steady. Here’s a twist most overlook: the fine print might leave out rider costs when giving back money at the end. Even if the main part of your payment comes back, those added charges for extras? They’re sometimes kept by the company. Not every dollar you handed over gets returned.

Most times, the pay out at maturity ends up smaller than hoped, especially when extra features got added through long years on the plan. Knowing how that works ahead of time avoids let-down later plus makes it easier to see which policies truly line up.

Hidden Fact #8: The Money-Back Feature Can Create a False Sense of Value

Surprisingly, how we think affects every dollar choice. Many folks feel better when they get cash back instead of watching payments vanish. Seeing this pattern, insurers frame Return of Premium Term Insurance as an answer for those uneasy about losing it all. Getting your money back years later might seem like a win, yet it doesn’t always reflect strong growth. Some people walk away happy just seeing a payout at the end, although once inflation and missed chances are factored in, the real gain could be small.

This mindset can prevent objective evaluation of alternative strategies. Similar behavioural mistakes often appear among investors who make emotional decisions instead of rational ones, which is why understanding common mistakes investors make with insurance can be valuable before selecting any policy. Maturity benefits should not be confused with wealth creation.

Hidden Fact #9: Return of Premium Plans Are Suitable Only for Certain People

Because Return of Premium Term Insurance gives something more than a standard term plan, many customers believe it is inherently better. In actuality, personal circumstances and financial goals are the only factors that determine eligibility. For some people, certainty is the most important thing. They want predictable results, detest market-linked investments, and are more at ease with a guaranteed maturity reward. An ROP policy can offer these buyers both financial discipline and psychological fulfillment.

However, a regular term plan paired with long-term investments may yield superior results for those who feel comfortable investing individually. More flexibility is made possible by the decreased premium, which frequently leads to more overall wealth generation. The most important lesson is that no insurance package is flawless for everyone. Your objectives, risk tolerance, investing style, and family protection needs all play a role in selecting the best policy.

Return of Premium vs Regular Term Insurance

| Feature | Return of Premium Term Insurance | Regular Term Insurance |

|---|---|---|

| Death Benefit | Available | Available |

| Maturity Benefit | Premium refund if policyholder survives | No maturity benefit |

| Premium Cost | Much Higher | Lower |

| Coverage Affordability | Lower coverage for same budget | Higher coverage for same budget |

| Investment Flexibility | Limited | High |

| Inflation Protection | Weak | Depends on separate investments |

| Long-Term Returns | Usually modest | Potentially higher through independent investing |

| Suitable For | Conservative buyers | Cost-conscious buyers seeking maximum protection |

| Main Objective | Protection + Premium Refund | Pure Protection |

| Financial Planner Preference | Moderate | Generally Preferred |

Life cover comes with either policy, yet what you gain financially might surprise. For each rupee paid, standard term plans often stretch further in protection. Those drawn to getting money back when time runs out lean toward Return of Premium options. Where you stand hinges on how you weigh money goals, comfort with risk, and where you aim years ahead.

Advantages of Return of Premium Term Insurance

- Premium Refund at Maturity: Should you make it through the policy period, a portion of what you paid comes back. That peace of mind matters to plenty who dislike losing every dollar to coverage.

- Protecting Loved Ones Financially: Besides offering a pay out upon death, an ROP plan secures your loved one’s future should life take a sudden turn. Protection stays in place throughout the coverage period, just like standard term insurance does.

- Predictable Outcome: When it comes to pay out timing, one thing stays fixed instead of shifting with the market. That steady outcome draws people who like knowing what’s coming rather than gambling on bigger unknown gains.

- Encourages Long-Term Discipline: Most people stick with their payments when they know money comes back later. That steady flow of cash keeps coverage active for years. Only then does the full benefit show up.

- Suitable for Risk Averse Individuals: When risk feels uncomfortable, ROP plans tend to ease the worry. Knowing money comes back helps calm nerves when markets jump or drop.

Disadvantages of Return of Premium Term Insurance

- Significantly Higher Premiums: Cost stands out first. That price tag climbs way higher compared to a standard term policy with identical protection.

- Lower Effective Returns: Even when premiums get returned, gains built up over many years tend to be fairly small next to what different long-term investments can offer.

- Inflation Erodes Value: What looks good now might feel smaller later because rising prices eat into what you can actually buy when the money arrives.

- Less Coverage Same Spending: With steeper costs, many pick lighter plans – this could mean less protection for loved ones down the road.

- Reduced Financial Flexibility: Money set aside for coverage grows, leaving less room to grow wealth through saving or putting funds to work. What stays in policies cannot build future value elsewhere.

Should You Buy Return of Premium Term Insurance?

Your priorities and financial habits will determine the answer. A normal term plan is typically a better option if your main goal is to get the best life insurance coverage at the most affordable price. You can buy greater coverage and use the savings for other investments thanks to the lower cost. This strategy frequently yields better financial outcomes in the long run.

But not everyone feels at ease making investments. Some people cherish guaranteed results, detest market instability, and prefer predictability. Return of Premium Term Insurance can provide these individuals with security and comfort. The certainty that the funds were not fully utilized for insurance expenses comes from receiving premiums back at maturity.

Examine policy characteristics thoroughly before making a choice. Understanding the key ratios for choosing insurance policy options can help evaluate plans objectively. At the same time, buyers should understand the common causes of term insurance claim rejection because claim settlement quality matters far more than maturity benefits.

In the end, conservative people who value certainty could find Return of Premium Term Insurance to be appropriate. Buyers seeking a deeper understanding of insurance principles and risk management can also explore educational resources available through the National Insurance Academy (NIA). A regular term plan might be more beneficial for buyers who want to maximize coverage and build long-term wealth.

Real-Life Examples

- The Conservative Government Worker: Government worker Rajesh needed coverage yet hated losing money if he lived past the plan’s duration. Because the promise of repayment fit how carefully he handled cash, he picked a Term Plan that gives premiums back. Even though gains weren’t large, knowing every rupee would return made him feel secure. Comfort came first – beating out bigger profits any day.

- The Young Investor: Aman worked as a software engineer. At age thirty, he looked at two types of life insurance – one was standard, the other promised returns if he outlived it. Instead of choosing the return-of-premium option, he went with lower-cost coverage. The money saved didn’t sit idle. He put those funds into different kinds of assets. Years passed. That pile of invested cash expanded more than expected. In the end, what he built beat the pay out the ROP plan would have given. Sticking to his method opened up room to grow wealth steadily. Flexibility came naturally when choices weren’t tied to rigid policies.

- The Underinsured Family Provider: One day Suresh looked at his tight money situation and picked an insurance plan with a return feature just so something would come back later. That choice came at a cost though – the price tag ate up most of what he could spend. So after thinking hard about who relied on him, he made another move entirely. Protection grew much larger when he shifted to basic term coverage instead. His people stood stronger because of it.

- The Risk-Averse Retiree: Most days, Meena leaned toward what was sure, staying clear of anything tied to market swings. A Return of Premium Term Insurance fit right into how she liked handling money – quiet and cautious. True, the gains weren’t big. Still, knowing every rupee would return when time ended brought peace more than profit ever could.

Conclusion

Most people worry about spending years on insurance only to get zero return. That peace of mind sounds good – yet costs more each month, loses value over time, offers weak growth, and locks you in tighter. Some cautious folks might accept those trade-offs for guaranteed outcomes. Still, anyone focused on strong coverage or building lasting assets ought to weigh other paths first. True fit matters far more than flashy claims – it’s what supports your household’s real plans ahead.

FAQs

Q1: Is it worthwhile to get Return of Premium Term Insurance?

For cautious consumers who like certain results, it may be beneficial. Regular term insurance, however, is frequently preferred by people looking for maximum coverage.

Q2: Does Return of Premium Term Insurance yield profits?

Not in the conventional sense. The policy should be primarily considered an insurance product since it primarily refunds qualified premiums.

Q3: Why do ROP premiums cost more than those of standard term plans?

Because it guarantees to reimburse eligible premiums if the policyholder lives out the policy period, the insurer raises the price.

Q4: Does the refund include rider premiums?

Not all the time. Rider premiums might not be covered by the maturity benefit, and many insurers simply reimburse the base premium.

Q5: Can the maturity amount be impacted by inflation?

Indeed. Over time, inflation lowers purchasing power, which might drastically reduce the refund’s actual worth decades later.

Q6: Which is preferable, regular term insurance or return of premiums?

Your objectives will determine which solution is best. While ROP policies give a maturity benefit, regular term plans often offer greater coverage.

Q7: Are youthful investors a good fit for Return of Premium Term Insurance?

A regular term plan and independent investment strategy may frequently be more advantageous for young investors who are at ease making separate investments.

Disclaimer

Learning comes first here. Over time, coverage details shift – each provider sets different terms for premiums, perks, or rules tied to taxes. Look closely at the paperwork if something feels unclear. Guidance from someone trained in money matters could help spot what fits best. Official websites of regulators hold current facts worth checking. What applies today might not stay true tomorrow.