Confused about NPS vs Mutual Fund SIP for Retirement? Discover 7 surprising facts about tax benefits, returns, liquidity, and wealth creation to choose the right retirement strategy. NPS vs Mutual Fund SIP for Retirement, NPS vs SIP, NPS or SIP for retirement, retirement planning India, NPS tax benefits, SIP for retirement, pension planning India, retirement corpus planning, mutual fund SIP benefits, retirement investment options, annuity vs SWP, retirement savings strategy, long term investing India.

Introduction

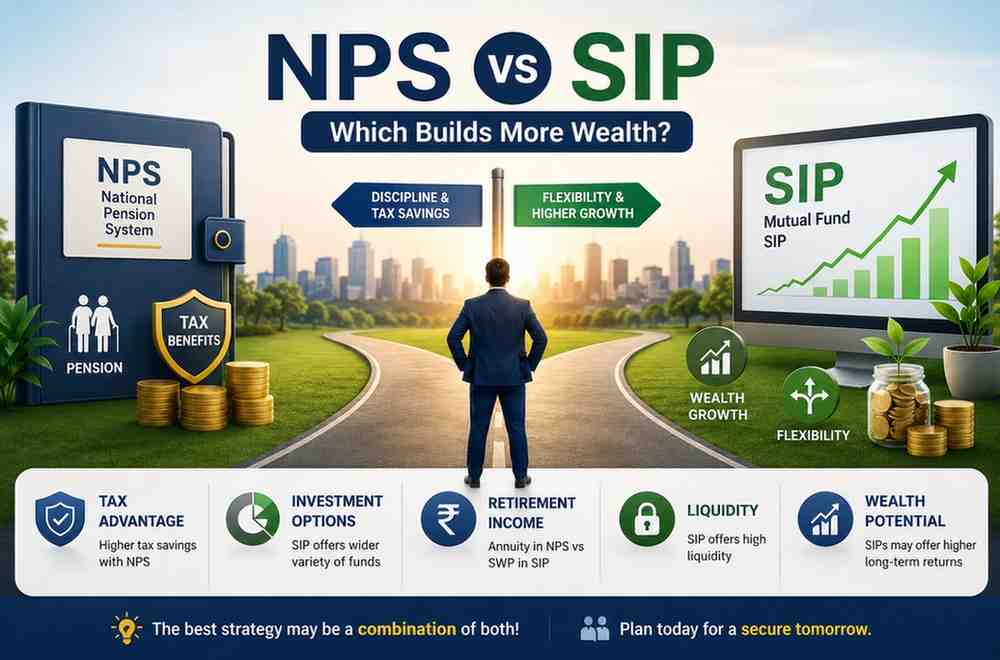

Retirement planning is one of the most important financial objectives, yet many individuals struggle to select the appropriate investment vehicle. Two prominent solutions that frequently come up in talks are the National Pension System (NPS) and Mutual Fund SIPs. Both help to accumulate wealth over time, but they differ greatly in terms of flexibility, tax benefits, liquidity, and retirement income. Some investors prefer NPS due to its tax benefits and retirement-focused structure, but others prefer SIPs for their growth potential and investing flexibility. The challenge is determining which option best corresponds with your financial objectives.

If you’ve already used a retirement corpus calculator to predict your future needs, the next step is to choose the best investing strategy to meet those goals. Understanding how to calculate your retirement corpus can help you make a more informed decision. Let’s look at seven unexpected statistics to assist you decide whether NPS, Mutual Fund SIPs, or a combination of both are the best options for retirement planning.

What Is NPS?

The National Pension System (NPS) is a government-regulated retirement savings system overseen by the Pension Fund Regulatory and Development Authority (PFRDA). Investors can review the latest PFRDA guidelines for NPS subscribers to understand contribution, withdrawal, and account-related rules. It was originally intended for government personnel but is now available to all Indian citizens. NPS is specifically designed to assist participants in building a retirement portfolio through regular payments over time. The money invested in NPS is divided among equity, corporate bonds, government securities, and alternative assets, depending on the investor’s asset allocation.

One of the most appealing aspects of NPS is its tax benefits. Investors can claim deductions under Sections 80CCD(1) and 80CCD(1B), making it one among the most tax-efficient retirement options in India. Unlike many other investment products, NPS is solely focused on retirement. This means that investors cannot withdraw money whenever they want. While a lack of flexibility may appear to be restricting, it also aids in the maintenance of investing discipline throughout one’s working years. Many investors prefer NPS for its organized approach to retirement planning and tax-saving potential. Understanding why NPS is good for retirement can provide additional clarity for long-term investors.

What Is Mutual Fund SIP?

A Systematic Investment Plan (SIP) is a method of investing a set amount of money on a regular basis in mutual funds. Instead of contributing a large flat sum, investors contribute on a monthly, quarterly, or other set schedule. Unlike NPS, SIP is not a standalone investment product. It is basically a strategy of investing in mutual funds, which may include equity funds, debt funds, hybrid funds, index funds, and a variety of other categories. The greatest benefit of SIP investing is flexibility. Investors can begin with small amounts, increase contributions as their income grows, stop investments during financial challenges, or redeem their investments as needed.

SIPs gain greatly from rupee-cost averaging and long-term compounding. Investors who remain diligent over decades frequently see significant wealth accumulation. The impact becomes even more powerful when combined with the power of compounding over a long investment horizon. Because of their flexibility and growth potential, SIPs have become one of the most popular investment strategies among Indian investors seeking financial independence and retirement security.

NPS vs Mutual Fund SIP for Retirement

Retirement sits at the core of NPS, shaping how it works. Because of that, rules guide where money goes plus when it can be touched. Tax perks come along, meant to keep people steady over years. Unlike that path, Mutual Fund SIPs move without such limits. Goals shift person to person – down payment, travel, education – they decide. Money grows steadily but stays reachable whenever life changes course. Most people must turn part of their NPS savings into a steady payout when they retire. That flow of cash helps cover living costs later in life. With SIPs, no rules force you to set up payments that way. Your funds stay flexible. How you use them down the road is entirely your call.

Freedom to pick investments sets them apart. Picking a mutual fund means sorting through hundreds, spread across types and risk levels. Those in NPS face narrower lanes, with less room to shift how money is split. Choices there come with tighter rules. One way to look at it – NPS versus SIP – isn’t clear cut every time. Flexibility and stronger gains matter a lot to certain investors, yet stability and long-term habits draw in others just as much. Clarity begins to appear once you walk through the seven unexpected points ahead.

Fact #1: SIP Offers More Flexibility Than NPS

Starting small means room to grow later. When money gets tight, payments shrink without penalty. Life shifts? Hitting pause works just fine. Even stopping altogether stays allowed if plans change. Moving cash into another fund takes little effort. Pulling out money happens when it suits the saver best.

Only meant for retirement, NPS sticks to tighter rules than most plans. When you pull money out early, it can only happen if specific criteria are met. Unlike mutual funds, getting at your cash isn’t easy. Because of these limits, people stay more focused on saving long term. Less freedom comes with that kind of commitment.

Years go by, life shifts – SIPs let savers adjust without locking them into fixed plans. Still, too many dips into the fund might weaken what a person hopes to have later on.

NPS vs SIP – Flexibility Comparison

NPS

- Restricted withdrawals

- Retirement-oriented framework

- Limited investment options

Mutual Fund SIP

- Easy adjustment of investments

- Freedom to redeem funds.

- A broad range of investment choices

Fact #2: NPS Has a Strong Tax Advantage

Here’s how taxes play a role in why people pick NPS. Putting money into NPS might lower taxable income, thanks to breaks listed in different parts of the Income Tax Act. On top of that, there’s an extra tax reduction allowed under Section 80CCD(1B). Because of this added cut, people saving for later life might pay less tax as they grow their future funds. Investors can verify the latest income tax deductions available under NPS before making retirement planning decisions. Some workers get extra breaks on taxes when employers add money. These perks depend on how the company sets up its plans.

Most mutual fund SIPs won’t cut your taxes – unless they’re in ELSS. That’s why people focused on saving more at tax time tend to lean toward NPS instead. Yet wealth builds over time regardless of tax perks. Choosing investments means weighing growth just as much.

NPS vs SIP – Tax Benefits Comparison

NPS

- Additional tax deduction is available.

- Employer contribution benefits

- Designed to maximize retirement tax efficiency.

Mutual Fund SIP

- Limited tax-saving possibilities.

- ELSS is essential for tax deductions.

- focuses exclusively on wealth creation.

Fact #3: SIPs Often Have Higher Wealth Creation Potential

Most times, building lasting wealth leans toward Mutual Fund SIPs. Picking among many stock-focused options opens doors to stronger gains across extended periods. Equity investments are part of NPS, yet capped allocations often mean less market reach than bold stock-focused funds. These boundaries keep volatility in check – though at the cost of slower wealth build-up over time.

Young folks putting money away for two or three decades might grow far more by leaning into stocks via regular instalments. Sticking to the plan, even when markets shift unpredictably, tends to reward those who wait it out. New investors can also explore SEBI investor education resources to better understand mutual fund investing and risk management.

This does not imply that NPS delivers bad results. Rather, SIPs often provide additional chances for investors prepared to tolerate increased market volatility in exchange for possibly better profits.

NPS vs SIP – Wealth Creation Potential

NPS

- Balanced asset allocation.

- Controlled risk exposure

- Ideal for prudent retirement planning.

Mutual Fund SIP

- Higher equity allocation is possible.

- Higher long-term growth potential

- suitable for aggressive investors.

Fact #4: NPS Encourages Better Retirement Discipline

Most people dive into saving for retirement full of energy, yet keeping that pace feels harder as time passes. When markets dip, daily costs rise, or sudden money needs pop up, steady investing tends to slip. Most people struggle to save for later years. A setup built around aging shifts habits quietly. Money stuck away grows because it sits untouched. Hard to reach means rarely touched. Behaviour changes when access slows. Growth happens not by planning but by delay. Patience rides on limits, not willpower.

When it comes to SIP investing, having room to change plans feels helpful – yet too much freedom might backfire. Pulling money out often, hitting pause when markets dip, or hunting quick gains may quietly reshape what retirement looks like. Avoiding common retirement planning mistakes is often more important than selecting the perfect investment product. For investors who seek structure and regularity, NPS can be an effective retirement planning tool.

NPS vs SIP – Retirement Discipline

NPS

- Strong retirement focus.

- Reduced the temptation to withdraw.

- Encourages long-term investment.

Mutual Fund SIP

- Investor-led discipline

- Easy access to funds

- Greater flexibility, but higher behavioral risk.

Fact #5: Retirement Income Works Very Differently

Many investors concentrate on constructing a retirement fund while paying little attention to how that fund will generate income after retirement. This is where NPS and mutual fund SIPs diverge dramatically. Under NPS guidelines, a portion of the retirement fund is typically utilized to purchase an annuity that provides a regular pension-like income. This ensures that pensioners continue to get money during their retirement years.

Mutual Fund SIPs give investors ultimate control over their retirement funds. They can generate income via a Systematic Withdrawal Plan (SWP), withdraw funds as needed, or adjust withdrawals in response to changing expenses. Investors seeking a predictable pension may favour NPS, whilst those seeking flexibility are more likely to pick SIP-based retirement schemes. Understanding the difference between annuity and SWP for retirement can help investors make a better decision.

NPS vs SIP – Retirement Income

NPS

- Regular pension via annuity.

- Structured retirement income.

- Less flexibility.

Mutual Fund SIP

- SWP-based income.

- More control over withdrawals.

- Flexible Retirement Planning

Fact #6: Liquidity Can Be a Game Changer

Most times things do not follow a set path. Health issues, caring for loved ones, or sudden chances might mean needing money from savings earlier than expected. Most mutual fund SIPs let you pull out cash when life demands it. When plans change, getting your money back stays simple – ideal for anyone needing quick access without long waits.

Retirement sits at the core of NPS, shaping its purpose. Even when rules permit taking out some money early, getting hold of those savings often hits roadblocks. Movement within the system leans toward limits rather than freedom. Younger investors often hit big money moments long before retiring. Since access to cash feels easy, staying on track means thinking twice about every pull of the trigger.

NPS vs SIP – Liquidity

NPS

- Limited access to funding.

- Retirement-related restrictions

- Encourages long-term investment.

Mutual Fund SIP

- Easy redemption.

- High liquidity

- Suitable for shifting financial needs.

Fact #7: Using Both Together May Be the Smartest Strategy

Many investors are surprised to learn that retirement planning does not necessarily entail choosing between NPS and SIPs. In fact, combining the two can produce the finest outcomes. NPS can provide tax breaks and retirement discipline, whilst SIPs can provide greater flexibility and wealth development possibilities. Using both products enables investors to capitalize on their individual strengths while reducing their limitations.

For example, an investor may contribute enough to the NPS to optimize tax benefits while also investing in stock SIPs for long-term development. This method can lead to a more balanced and diverse retirement strategy. Many investors seeking financial independence prefer a combination strategy because it offers both stability and growth. Those evaluating their retirement savings goals often find that relying on multiple retirement tools improves overall financial security.

NPS vs SIP – Combined Approach

Benefits of NPS

- Tax savings

- Retirement Discipline

- Structured income.

Benefits of SIP

- Increased growth potential

- Better liquidity.

- Increased investment flexibility

NPS vs Mutual Fund SIP for Retirement: Quick Comparison

| Feature | NPS | Mutual Fund SIP |

|---|---|---|

| Primary Objective | Retirement Planning | Wealth Creation |

| Tax Benefits | High | Limited |

| Flexibility | Low | High |

| Liquidity | Restricted | High |

| Investment Choices | Limited | Extensive |

| Equity Exposure | Restricted | Flexible |

| Retirement Discipline | Strong | Depends on Investor |

| Annuity Requirement | Generally Required | Not Required |

| Wealth Creation Potential | Moderate to High | High |

| Suitable For | Tax Savers | Growth-Oriented Investors |

Which One Can Build More Wealth?

Most times, when building wealth matters most, Mutual Fund SIPs tend to lead – thanks to broader choices plus room for heavier stock investments. Stretched across decades, say two or three, these equity-focused plans often grow at a notable pace. Still, building wealth isn’t something to consider alone. Thanks to tax perks, NPS lets more money grow inside it, keeping early pulls at bay. These features often make a real difference when people reach retirement.

How things turn out hinges on how you handle investing. Those who stick to a routine could grow big savings using SIPs, whereas people often pulling money out may find NPS fits better. Sometimes, mixing the two paths leads to the sturdiest future when stepping away from work.

Real-Life Examples

Example 1: Rahul, Age 30, Salaried Employee

At sixty, Rahul hopes to stop working – he’s building that chance now. Each year, his NPS payments are sized just right to grab the extra tax break from Section 80CCD(1B). Alongside that move, equity mutual funds get steady cash through SIPs. Growth over time gets a boost because of this split path. Taxes shrink today; tomorrow’s savings grow bigger as a result. Relying only on one tool never happens here. Strengths from both sides – NPS discipline and SIP flexibility – do the work together.

Example 2: Neha, Age 35, Self-Employed Professional

Sometimes Neha adjusts how much she saves, depending on what her business earns each month. Her work means money comes in unevenly, so fixed plans feel too tight. Mutual fund SIPs let her move smoothly between busy spells and quiet ones. Even if NPS cuts taxes now, being stuck with long-term rules feels limiting later. What matters most is staying free to shift gears when life changes – SIPs allow that without fuss.

Example 3: Amit, Age 45, Conservative Investor

Worried by wild market swings, Amit leans on structure. His backbone? The NPS – forcing steady deposits while blocking early grabs at funds. Into that frame slips a modest SIP, feeding upside reach. Calm follows routine. Less twitching when prices jump. Staying put feels easier now. Growth ticks along, but peace matters more.

Conclusion

Retirement planning sparks talk about NPS or Mutual Fund SIP – no single winner suits everyone. When it comes to savings, tax perks stand out with NPS, along with steady habits and planned payouts later. On another note, choosing SIPs opens doors to easier access, adaptability through market shifts, plus room for growth over time. Growth hunters might pick SIPs. Tax savers aiming at retirement could go for NPS instead. Yet using both together tends to balance things best. Starting sooner sets the pace. Staying consistent matters just as much. Eyes locked on distant money targets make all the difference.

FAQs

Q1: Is NPS better than mutual fund SIPs for retirement?

For those focused on saving taxes and sticking to a retirement plan, NPS might fit better. When it comes to adapting over time and building wealth gradually, SIPs often work well. What suits you best hinges on personal aims and how much market change you can handle comfortably.

Q2: Can I invest in NPS and SIP at the same time?

Yes, many investors utilize both products together. NPS contributes to tax savings and retirement planning, whilst SIPs offer flexibility and additional wealth generation options.

Q3: Which provides higher returns: NPS or SIP?

Mutual Fund SIPs invested in equity-oriented funds often offer a higher return potential due to increased equity exposure. However, returns are subject to market conditions and investment duration.

Q4: Can I withdraw money from the NPS before I retire?

Partial withdrawals are permitted under certain conditions, although NPS is primarily intended for retirement savings. Withdrawal flexibility is significantly lower than that of mutual funds.

Q5: What is the main advantage of SIPs for retirement planning?

The main advantage is flexibility. Investors can select their preferred funds, change their contributions, and access their investments at any time.

Q5: Should young investors select NPS or SIP?

Young investors with extended investment horizons frequently profit from SIPs due to their growth potential. However, using NPS for tax benefits can result in a more balanced retirement strategy.

Disclaimer

This article serves education only, never standing in for expert money, tax, or investing direction. Market shifts shape gains, bringing changes that unfold without fixed pattern. Your personal aims, comfort with uncertainty, and timeline guide smart choices about where to put funds. For tailored insight, talking with a certified finance professional makes sense.