Discover 8 surprising reasons why credit score drops despite on-time payment and learn practical ways to improve your CIBIL score safely in India. why credit score drops despite on-time payment, why credit score drops, credit score dropped suddenly, CIBIL score decrease reasons, factors affecting credit score, improve credit score India, credit utilization impact, unsecured loan impact on CIBIL, why CIBIL score decreases, credit score mistakes.

Introduction

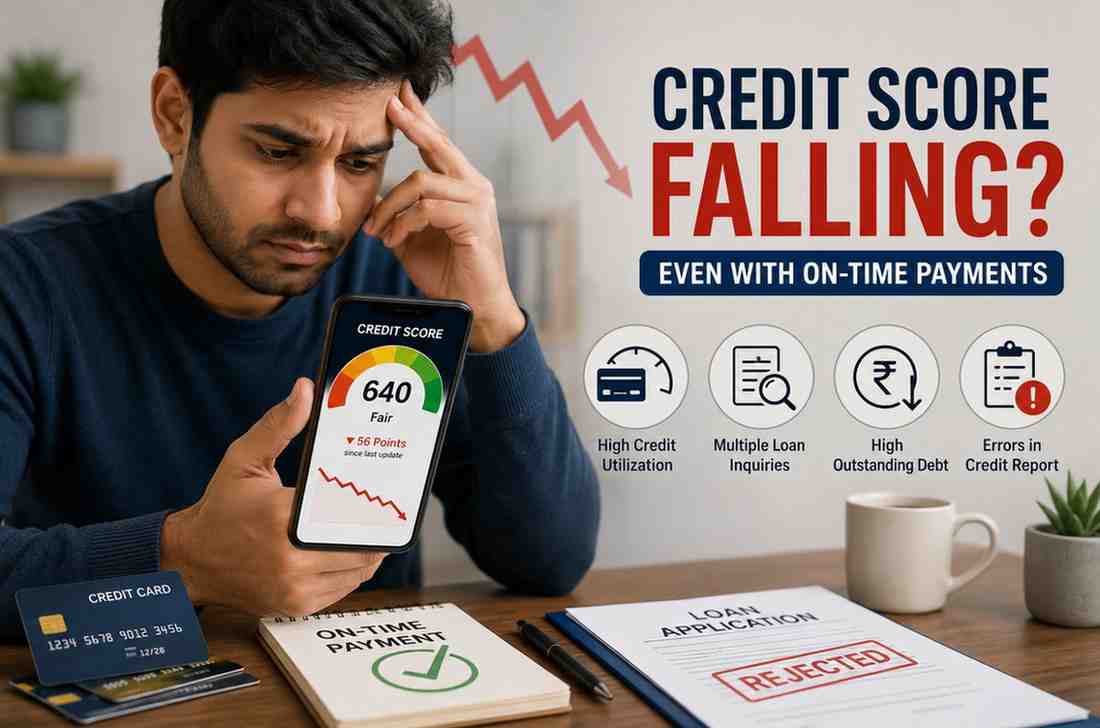

Frustration hits some borrowers when their credit rating drops – despite never missing an EMI or credit card payment. Lately, it happens more often than before since many believe just paying on schedule covers everything needed. Yet behind the scenes, lenders look at a handful of money habits before setting that number. What shows up on your report isn’t built from payments alone. If you are searching for why credit score drops despite on-time payment, the answer often lies in hidden factors such as high credit utilization, excessive loan applications, unsecured borrowing, report errors, or even becoming a loan guarantor. A low credit score can raise loan interest rates, diminish approval chances, and limit financial flexibility during emergencies. According to TransUnion CIBIL, maintaining a healthy score requires balanced borrowing habits, responsible debt management, and disciplined financial behaviour over a long period. Understanding these underlying factors will help you avoid unnecessary credit damage and establish stronger financial reputation in the future.

What Does a Credit Score Actually Measure?

Lending trust isn’t just about paying back – it shows up as a number. India sees these figures run from 300 to 900, where past 750 tends to open doors quicker, bringing lower charges on borrowed money. What shapes that digit? Missed payments weigh in, so does how much you owe right now, how close you are to maxing out limits, how long accounts have been active, fresh applications, even the mix of debts held. Sometimes, despite flawless returns on time, numbers dip – something shifted behind the scenes tipped the scale. When someone asks for cash, property financing, company funding, or high-end plastic, institutions check this mark before saying yes. Most of the time, a high mark means your finances are steady. When the number dips, banks see it as harder to pay back. Because institutions watch this digit closely when you borrow, keeping it solid opens doors later on down the road.

Why Credit Score Drops Despite On-Time Payment

Here are the most common hidden causes that can lower your credit score, even if you make your payments on time.

1. High Credit Utilization Ratio

High credit usage often quietly drags down scores more than people realize. This number shows how much of your allowed borrowing space is filled at any time. Imagine having a ₹1 lakh card limit while routinely charging over ₹75,000 each month. Paying off everything by the deadline does not erase concern entirely. From a lender’s perspective, that pattern hints at relying too heavily on debt. One way to stay safe? Keep your credit use under 30%. Some folks on fixed incomes hurt their ratings without realizing it – chasing cashback leads them to swipe too often. When several cards run close to max at once, trouble starts building quietly. Those stuck paying just the bare minimum tend to fall into this trap more easily, especially if perks drive how they spend. Borrowers trying to improve their financial profile often build healthier borrowing habits after understanding practical methods from how to build credit without credit cards in 2025. Lower utilization typically indicates higher financial discipline and less repayment stress for lenders.

2. Multiple Loan Applications in Short Time

Lenders might think you’re desperate if too many requests show up close together. Each time someone applies for a loan, it often leaves a mark on their credit file. Getting quotes from different banks seems smart but comes at a cost some overlook. That trail of checks adds up, even if bills get paid right on schedule. Needing funds isn’t the issue – how you go about seeking them matters more than expected. One issue shows up if people sign up for several credit cards just to get cash rewards or access lounges at airports. When applications pile up close together, it looks like someone is desperate for credit. Borrowers usually avoid unnecessary rejections once they understand the minimum CIBIL score required for loan approval. Responsible borrowing and limiting applications help to sustain long-term score stability.

3. Errors in Your Credit Report

Surprisingly often, errors show up on credit reports without people noticing. Incorrect late payments might appear, alongside repeated loan entries or wrong balance numbers – sometimes entire accounts aren’t yours at all. Even if you pay every bill on time, those glitches could drag your score down overnight. People usually spot trouble only once a denial arrives or their number drops out of nowhere. When lenders take too long to report closures, paid-off debts still linger as open obligations for weeks, even months. Borrowing under a fake name might leave hidden marks on your record unless caught fast. Watching things closely matters since small mistakes, when missed, slowly wreck your standing over time. Many users detect hidden reporting issues while regularly checking their reports through free credit score monitoring methods in India. Consumers can also verify their records directly through TransUnion CIBIL and Experian India to identify inaccurate entries before they create major borrowing problems.

4. Closing Old Credit Cards

Surprisingly, tossing out an old credit card might do more harm than good. That long-standing account? It quietly boosts how lenders see your history. Shutting it down can drag down the average age of your accounts fast. Losing that line of credit tightens your overall borrowing space too. When you shut a card but keep spending like before, the system sees higher usage right away. That spike in use tends to drag scores down across many models. Old accounts show steady habits – something lenders notice when they check reliability. Shutting several at once? That move often leads to sharper declines. Keeping those long time cards active, even with tiny charges, usually helps more than ending them fast. Financial behaviour linked to credit cards also becomes riskier when borrowers continue believing misconceptions associated with common credit card myths in 2025. Responsible long-term account management typically improves overall creditworthiness.

5. Becoming a Loan Guarantor

It might surprise you how risky it is to back a friend or family member’s loan. When someone else borrows money under your promise, lenders start seeing that debt as yours too – at least on paper. Missed payments by them can drag down your credit standing, no matter how careful you’ve been. Even changes like rescheduling instalments count against you when banks assess new applications. Defaulting? That hits hard. Your record could take damage, despite spotless habits of your own. Later on, when they try getting a loan themselves, that is when guarantors usually notice something went wrong. A missed payment by another person might quietly influence mortgage decisions, shape how much one can borrow personally, or limit options down the road. What happens after depends less on intention and more on history recorded elsewhere. Financial exposure increases significantly when borrowers ignore the risks associated with major CIBIL guarantor liabilities. Being a guarantor should always include rigorous financial consideration rather than emotional decision-making.

6. Delayed Reporting by Lenders

After making a payment, your number might dip if companies wait too long to send info to rating agencies. Though you finish paying fast, past balances sometimes still show up due to slow updates. Credit accounts, pay-later tools, and online loan apps often run into this delay. People think settling debt lifts scores right away – reality works slower. Agencies get data once per month, so any lag in lender reports can drag down numbers briefly. Even with fresh payments cleared, last month’s higher balance could be what appears now. When reports do not match up, mix-ups happen in loan decisions since lenders view only what is now on file. Sometimes lag time between banks and credit agencies leads to temporary errors showing up. Users heavily dependent on flexible repayment products often face additional risk through services like Buy Now Pay Later financing, where repayment tracking and reporting cycles may vary across providers.

7. Too Many Unsecured Loans

Borrowing without security might hurt your rating, even if you always pay on time. Things like personal loans, credit cards, BNPL plans, or EMI purchases count as unsecured – they have nothing backing them up. Lenders tend to favor a mix of debt types instead of leaning only on those no-collateral options. If these kinds of debts pile up, banks could start seeing trouble ahead should money get tight suddenly. Some people end up with multiple unsecured loans without even realizing it, yet they keep paying on time. Even so, their total debt can look shaky under closer inspection. Lenders tend to trust borrowers more when there is a balance between secured and unsecured credit. Trouble starts creeping in when someone takes out new personal loans just to handle old ones – payments stay consistent, but stress builds slowly beneath the surface.

8. Sudden Increase in Outstanding Debt

Out of nowhere, more unpaid balances might drag down your rating fast. Usually follows getting a fresh loan, buying big-ticket items on finance, stacking several monthly payments, or pulling close to your spending limits all at once. On time payments do not always offset the impact when amounts owed spike quickly. Lenders see heavier commitments as tougher to manage, even without missed due dates. How much you owe compared to how you borrow weighs heavily in automated assessments. When debts pile up fast, lenders might see someone as more at risk. Big events like weddings or health crises often spark those spikes – so do trips, new electronics, or living larger than before. Even if bills get paid on time, scores can drop when total borrowing shoots upward. Stability tends to come easier when loans grow slowly, handled step by step.

Real-Life Examples

Example 1: Cashback Card Usage Reduced Rahul’s Score

From Delhi, Rahul drew a salary and leaned on his rewards-heavy credit card for most transactions – groceries, petrol, work costs, even trips. Held a two-lakh rupee ceiling on borrowing, yet often spent above one point six lakhs each month. Despite clearing every single charge by the deadline, steadily lost around forty-five points off his rating across half a year. No delays in payment showed up, still the damage came from stretching that limit too far. What pulled him down wasn’t late bills but how much of the allowance he kept using. Slowly his score began rising after Rahul kept card spending under a third of each limit, shifting charges between different accounts. Trouble like this sneaks up on busy workers chasing rewards without realizing the cost.

Example 2: Excessive Loan Comparisons Hurt Neha’s Profile

Neha sought for personal loans from numerous banks and fintech companies within two weeks because she wanted the lowest feasible interest rate. Each lender thoroughly reviewed her report. Despite accepting only one loan and paying all EMIs on time, her score decreased since frequent queries indicated aggressive borrowing habits. When she later filed for a car loan, the bank deemed her recent credit history hazardous. After avoiding new applications for several months, her score steadily stabilized. This scenario is extremely prevalent among borrowers who compare loans aggressively online.

Example 3: Guarantor Responsibility Created Unexpected Trouble

At first, things seemed fine when Amit promised to back his cousin’s business loan – truth is, he didn’t grasp what it truly meant. Payments stayed on track early on; then again, profits dipped and instalments began slipping. Even though he never took out any money himself, his credit rating still dropped since the debt carried his name. Later, while applying for a house loan, lenders flagged the existing obligation, which cut down how much they’d offer. It often takes personal setbacks like these before someone sees how heavy such promises can become over time.

How to Improve Your Credit Score Again

- Keep credit utilization below 30%: Lower usage indicates regulated borrowing and financial prudence. Reducing reliance on credit cards often boosts lender trust over time.

- Avoid Frequent Loan Applications: Applying just when necessary eliminates harsh queries and keeps your profile from being financially stressed or credit-hungry.

- Check credit reports regularly: Monitoring reports allows you to detect hidden problems, fraudulent accounts, and delayed lender updates before they cause long-term damage.

- Maintain older credit accounts: Older accounts increase your average credit age and show lenders and bureaus that you have made consistent payments over time.

- Diversify Credit Carefully: Balanced secured and unsecured borrowing appears to be safer than relying just on unsecured personal loans or credit cards.

Common Credit Score Myths People Still Believe

- Checking My Own Score Reduces It: Self-checking through approved portals is typically treated as a mild inquiry and does not impact your credit score.

- Closing Credit Cards Always Improves Score: Closing old cards may reduce credit age and boost use ratios, which can have a negative influence on scoring models.

- Only Missed Payments Affect Scores: In addition to repayment history, credit use, hard inquiries, debt burden, and loan mix all have a substantial impact on ratings.

- Minimum Due Payments Are Enough: Minimum dues escape penalties momentarily, but excessive balances and interest charges continue to increase financial strain.

Conclusion

Understanding why credit score drops despite on-time payment is important because repayment discipline alone does not guarantee a healthy financial profile. What shapes a credit score? Things like how much of your limit you use, frequent loan checks, total debt load, reliance on cards, plus correct data flow behind the scenes. Paying EMIs on time doesn’t always save your rating – some still lose ground without realizing it. Too many swipes or chasing multiple loans chips away slowly, almost unnoticed. Watching activity month by month, borrowing in moderation, handling credit with care – it shields your number from silent drops. Solid standing opens doors when big moments come: buying something major, facing sudden costs. That kind of readiness lives beyond just approval chances.

FAQs

Q1: Why does my credit score drop even after I pay my EMIs on time?

High utilization, multiple hard inquiries, escalating debt levels, unsecured borrowing, or credit report inaccuracies can all lower your credit score. Credit bureaus assess entire financial behavior, not just repayment history.

Q2: Can checking my own credit score harm it?

No, self-checking through authorized channels is typically regarded as a light inquiry and has no negative impact on your score. Only hard inquiries initiated by the lender normally have a temporary impact on the credit score.

Q3: What is considered a safe credit utilization ratio?

Most experts advise keeping utilization below 30% of your total credit limit. Lower utilization usually indicates greater financial discipline and reduced repayment risk.

Q4: Does closing old credit cards lower your credit score?

Yes, it can happen because older cards increase average credit age and keep available credit limits higher. Closing them may boost the utilization ratio automatically.

Q5: How long does it take to improve a bad credit score?

Recovery may take many months, depending on repayment consistency, debt reduction, and error correction in reports. Responsible long-term borrowing behavior is critical for progress.

Q6: Can becoming a guarantor impact my CIBIL score?

Yes, if the borrower fails to make repayments on time, your own credit score may suffer as a result, because guaranteed loans are tied to your financial history.

Disclaimer

This piece serves education and information needs. It does not stand as financial, legal, or lending direction. Lenders and bureaus might score credit differently – each uses its own rules and ways of judging risk. Before doing anything, check your loan details, choices, and report data directly with trusted sources. Facts here aim to stay correct; even so, laws and money rules shift now and then. For personal help, reach out to someone trained in finance matters.